Tổng quan

Đây là chiến lược giao dịch đa tầng tích hợp tính toán Dải biên độ thực trung bình thích ứng (ATR) và phát hiện xu hướng dựa trên động lượng. Đặc điểm nổi bật nhất của chiến lược này nằm ở cơ chế chốt lời 7 bước độc đáo, kết hợp 4 mức thoát dựa trên ATR và 3 mức phần trăm cố định. Phương pháp hỗn hợp này cho phép nhà giao dịch điều chỉnh linh hoạt theo biến động thị trường, đồng thời thu lợi nhuận một cách có hệ thống trên cả thị trường tăng và giảm. Chiến lược cung cấp một giải pháp giao dịch toàn diện thông qua sự kết hợp giữa tính toán ATR động, phát hiện sức mạnh xu hướng và cơ chế chốt lời đa dạng.

Nguyên lý chiến lược

Cốt lõi của chiến lược hoạt động thông qua các thành phần chính sau:

- Tính toán Dải biên độ thực tăng cường: Đo lường biến động thị trường bằng cách xem xét các biến động giá đáng kể nhất.

- Tích hợp yếu tố động lượng: Điều chỉnh ATR dựa trên biến động giá gần đây, giúp nó thích ứng hơn.

- Tính toán ATR thích ứng: Điều chỉnh ATR truyền thống theo yếu tố động lượng, làm cho nó nhạy hơn trong các giai đoạn biến động.

- Định lượng sức mạnh xu hướng: Đánh giá sức mạnh của xu hướng thông qua thuật toán phức tạp.

- Cơ chế chốt lời 7 bước: Bao gồm bốn mức thoát dựa trên ATR và ba mức phần trăm cố định.

Ưu điểm của chiến lược

- Khả năng thích ứng cao: Thích ứng với các điều kiện thị trường khác nhau thông qua tính toán ATR động.

- Quản lý rủi ro hoàn thiện: Cơ chế chốt lời đa tầng cung cấp khả năng kiểm soát rủi ro có hệ thống.

- Tính linh hoạt cao: Có thể hoạt động hiệu quả như nhau trên cả thị trường tăng và giảm.

- Tham số có thể điều chỉnh: Cung cấp nhiều tham số có thể điều chỉnh để phù hợp với các phong cách giao dịch khác nhau.

- Thực thi có hệ thống: Quy tắc vào và ra rõ ràng giảm thiểu giao dịch cảm tính.

Rủi ro của chiến lược

- Nhạy cảm với tham số: Cài đặt tham số không phù hợp có thể dẫn đến giao dịch quá mức hoặc bỏ lỡ cơ hội.

- Phụ thuộc vào điều kiện thị trường: Có thể hoạt động kém trong thị trường biến động mạnh hoặc đi ngang.

- Rủi ro về độ phức tạp: Cơ chế chốt lời đa tầng có thể làm tăng độ khó thực thi.

- Ảnh hưởng của trượt giá: Nhiều điểm chốt lời có thể bị ảnh hưởng đáng kể bởi trượt giá.

- Yêu cầu quản lý vốn: Cần đủ vốn để thực hiện chiến lược chốt lời đa tầng.

Hướng tối ưu hóa chiến lược

- Điều chỉnh tham số động: Tự động điều chỉnh tham số theo điều kiện thị trường.

- Lọc môi trường thị trường: Thêm cơ chế nhận diện môi trường thị trường.

- Tăng cường quản lý rủi ro: Giới thiệu cơ chế dừng lỗ động.

- Tối ưu hóa thực thi: Đơn giản hóa cơ chế chốt lời để giảm ảnh hưởng của trượt giá.

- Hoàn thiện khung backtest: Thêm nhiều yếu tố giao dịch thực tế.

Tổng kết

Chiến lược này cung cấp cho nhà giao dịch một hệ thống giao dịch toàn diện thông qua việc kết hợp ATR thích ứng và cơ chế chốt lời đa tầng. Ưu điểm của nó nằm ở khả năng thích ứng với các điều kiện thị trường khác nhau, đồng thời quản lý rủi ro thông qua phương pháp có hệ thống. Mặc dù tồn tại một số rủi ro tiềm ẩn, nhưng với sự tối ưu hóa và quản lý rủi ro thích hợp, chiến lược này có thể trở thành một công cụ giao dịch hiệu quả. Cơ chế chốt lời đa tầng sáng tạo của nó đặc biệt phù hợp với những nhà giao dịch muốn tối đa hóa lợi nhuận trong khi vẫn duy trì kiểm soát rủi ro.

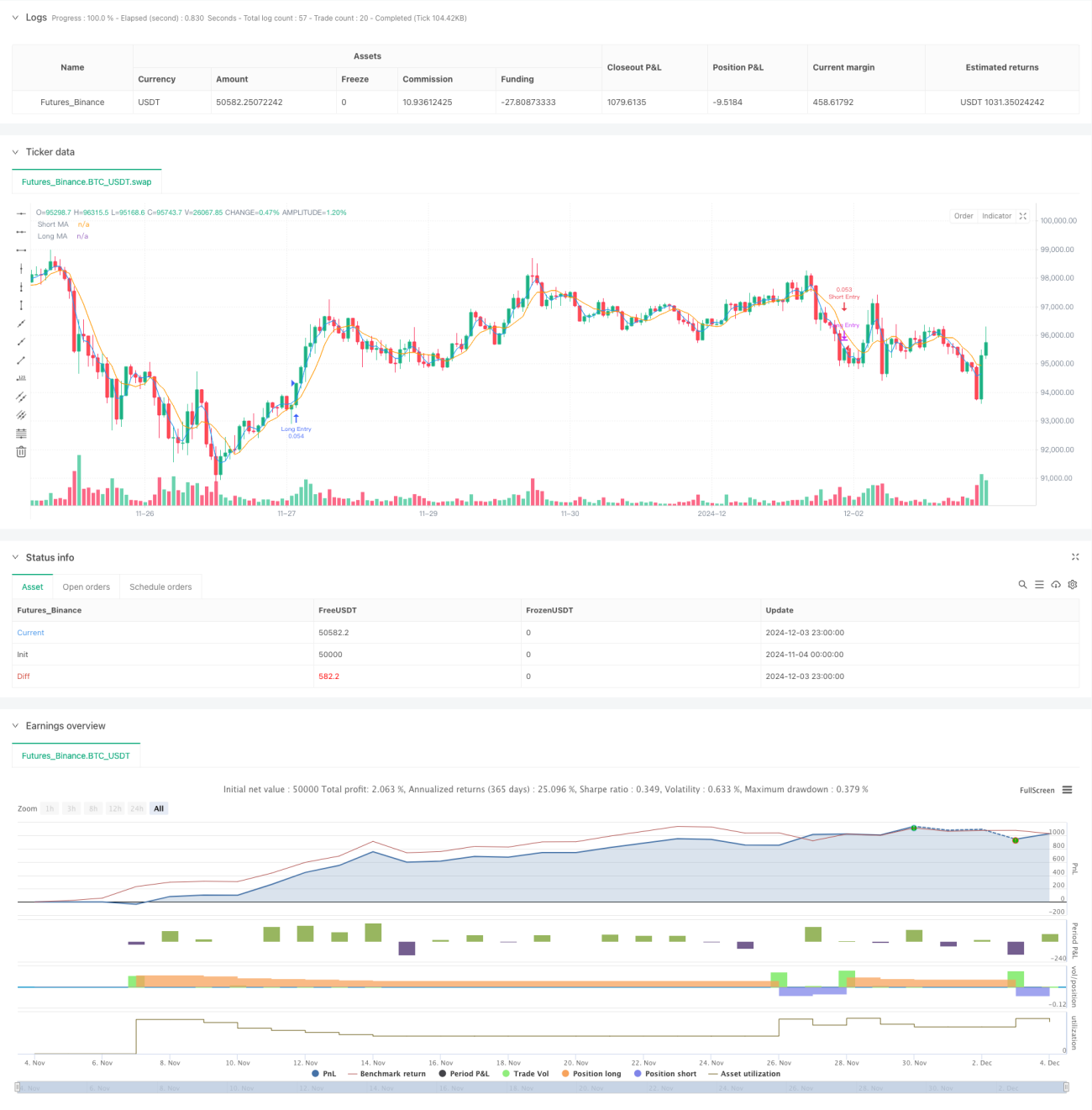

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The SuperATR 7-Step Profit Strategy is a multi-layered trading strategy that combines adaptive ATR and momentum-based trend detection - 1