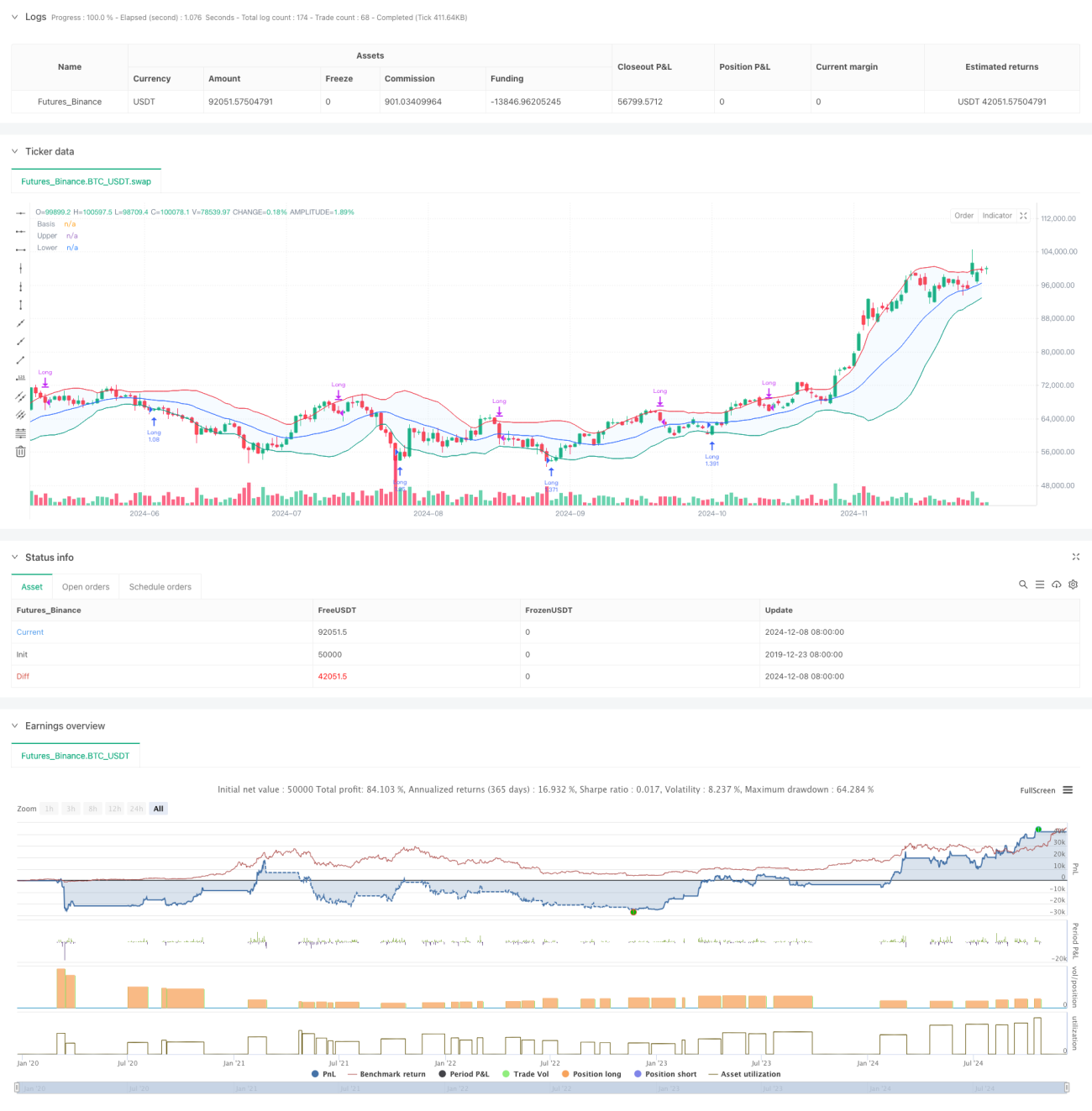

Tổng quan

Chiến lược này là một hệ thống giao dịch thông minh dựa trên chỉ báo Bollinger Bands và ATR, kết hợp cơ chế chốt lời và cắt lỗ đa lớp. Chiến lược chủ yếu sử dụng tín hiệu đảo chiều gần dải dưới của Bollinger Bands để vào lệnh mua, và quản lý rủi ro bằng phương pháp trailing stop động. Hệ thống được thiết kế với mục tiêu lợi nhuận 20% và mức cắt lỗ 12%, đồng thời kết hợp chỉ báo ATR để thực hiện trailing stop động, có thể bảo vệ lợi nhuận trong khi vẫn cho phép xu hướng phát triển đủ không gian.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm các phần chính sau:

- Điều kiện vào lệnh: Yêu cầu nến đỏ chạm dải dưới của Bollinger Bands, sau đó xuất hiện nến xanh; mô hình này thường báo hiệu khả năng đảo chiều.

- Lựa chọn đường trung bình động: Hỗ trợ nhiều loại đường trung bình động (SMA, EMA, SMMA, WMA, VWMA), mặc định sử dụng SMA 20 chu kỳ.

- Thông số Bollinger Bands: Sử dụng độ lệch chuẩn 1,5 lần làm bề rộng dải; thiết lập này thận trọng hơn so với độ lệch chuẩn 2 lần truyền thống.

- Cơ chế chốt lời: Đặt mục tiêu lợi nhuận ban đầu là 20%.

- Cơ chế cắt lỗ: Thiết lập mức cắt lỗ cố định 12% để bảo vệ vốn.

- Trailing stop động:

- Kích hoạt trailing stop dựa trên ATR sau khi giá đạt mức lợi nhuận mục tiêu.

- Kích hoạt trailing stop động dựa trên ATR sau khi giá chạm dải trên của Bollinger Bands.

- Sử dụng hệ số nhân ATR để điều chỉnh khoảng cách trailing stop động.

Ưu điểm của chiến lược

- Kiểm soát rủi ro đa cấp:

- Mức cắt lỗ cố định bảo vệ vốn gốc.

- Trailing stop động khóa lợi nhuận.

- Trailing stop động do chạm dải trên Bollinger Bands cung cấp bảo vệ bổ sung.

- Lựa chọn đường trung bình động linh hoạt giúp chiến lược thích ứng với các môi trường thị trường khác nhau.

- Trailing stop động kết hợp chỉ báo ATR có thể tự động điều chỉnh theo biến động thị trường, tránh thoát lệnh quá sớm.

- Tín hiệu vào lệnh kết hợp giữa mô hình giá và chỉ báo kỹ thuật, nâng cao độ tin cậy của tín hiệu.

- Hỗ trợ quản lý vị thế và thiết lập chi phí giao dịch, phù hợp hơn với môi trường giao dịch thực tế.

Rủi ro của chiến lược

- Thị trường biến động nhanh có thể dẫn đến giao dịch thường xuyên, tăng chi phí giao dịch.

- Mức cắt lỗ cố định 12% có thể quá nhỏ đối với một số thị trường có biến động cao.

- Tín hiệu từ Bollinger Bands trong thị trường xu hướng có thể tạo ra tín hiệu giả.

- Trailing stop dựa trên ATR trong điều kiện biến động mạnh có thể dẫn đến drawdown lớn.

Biện pháp giảm thiểu:

- Khuyến nghị sử dụng trên khung thời gian lớn hơn (30 phút - 1 giờ).

- Có thể điều chỉnh tỷ lệ cắt lỗ dựa trên đặc điểm cụ thể của sản phẩm.

- Cân nhắc thêm bộ lọc xu hướng để giảm tín hiệu giả.

- Điều chỉnh động hệ số nhân ATR để thích ứng với các môi trường thị trường khác nhau.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa vào lệnh:

- Thêm cơ chế xác nhận khối lượng giao dịch.

- Thêm chỉ báo cường độ xu hướng để lọc tín hiệu.

- Cân nhắc thêm chỉ báo động lượng hỗ trợ phán đoán.

-

Tối ưu hóa cắt lỗ:

- Thay đổi cắt lỗ cố định thành cắt lỗ động dựa trên ATR.

- Phát triển thuật toán cắt lỗ thích ứng.

- Điều chỉnh động khoảng cách cắt lỗ theo biến động.

-

Tối ưu hóa đường trung bình động:

- Kiểm tra các tổ hợp chu kỳ khác nhau.

- Nghiên cứu phương pháp chu kỳ thích ứng.

- Cân nhắc sử dụng hành vi giá thay thế đường trung bình động.

-

Tối ưu hóa quản lý vị thế:

- Phát triển hệ thống quản lý vị thế dựa trên biến động.

- Thực hiện cơ chế vào lệnh và giảm vị thế theo từng phần.

- Thêm kiểm soát rủi ro danh mục.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch đa lớp thông qua chỉ báo Bollinger Bands và ATR, áp dụng phương pháp quản lý động trong việc vào lệnh, cắt lỗ và chốt lời. Ưu điểm của chiến lược nằm ở hệ thống kiểm soát rủi ro hoàn thiện và khả năng thích ứng với biến động thị trường. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược còn nhiều dư địa cải thiện. Đặc biệt phù hợp sử dụng trên các khung thời gian lớn hơn; đối với nhà đầu tư nắm giữ tài sản chất lượng tốt, chiến lược có thể giúp tối ưu hóa thời điểm xây dựng và giảm vị thế.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Demo GPT - Bollinger Bands Strategy with Tightened Trailing Stops", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_value=0.1, slippage=3)

// Input settings- 1