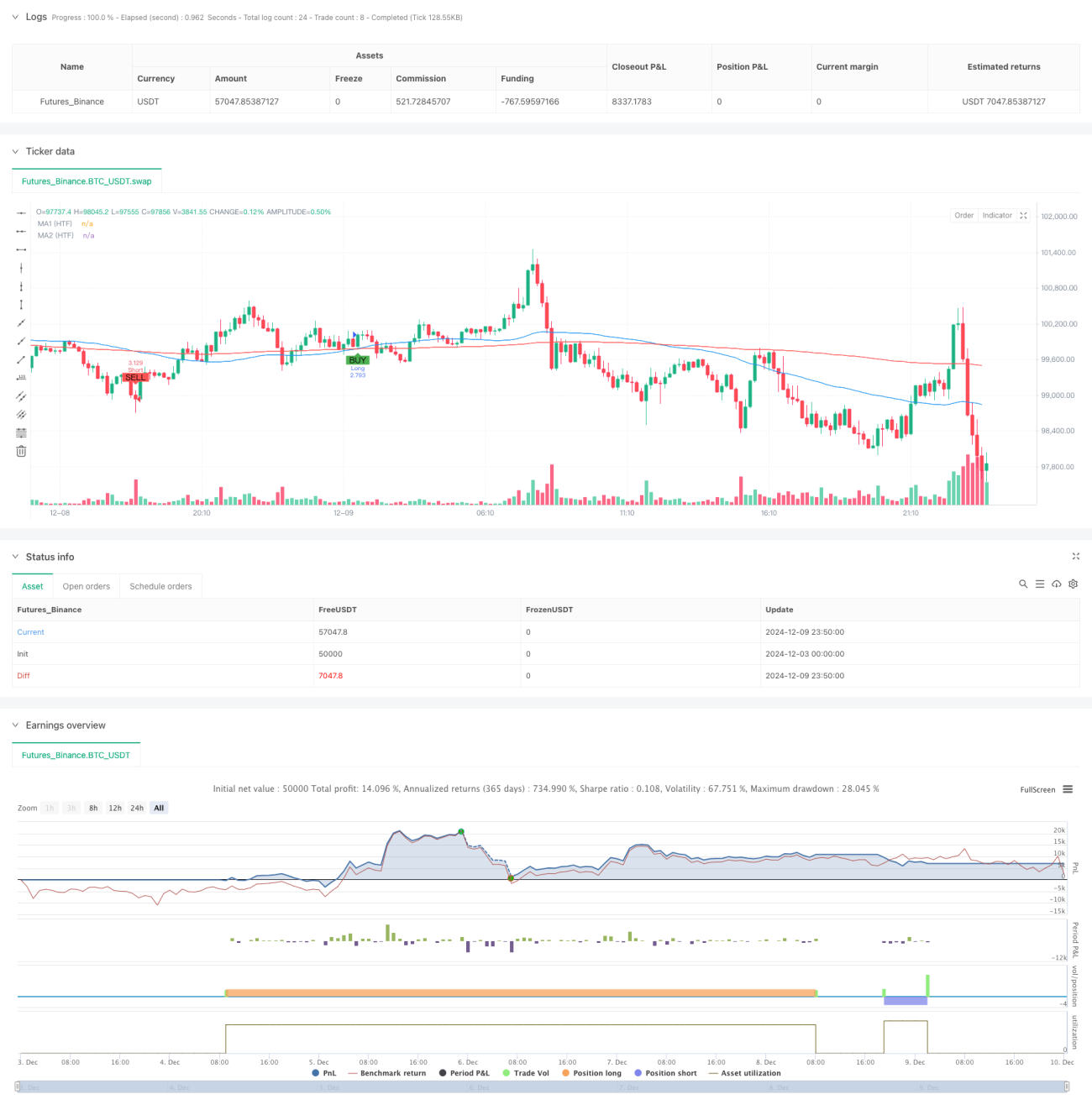

Tổng quan

Chiến lược này là một hệ thống giao dịch thông minh dựa trên nhiều đường trung bình động và cường độ xu hướng. Nó đo lường cường độ xu hướng thị trường bằng cách phân tích mức độ lệch giữa giá và các đường trung bình động có chu kỳ khác nhau, kết hợp với chỉ báo biến động ATR để quản lý vị thế và kiểm soát rủi ro. Chiến lược có tính tùy chỉnh cao, có thể linh hoạt điều chỉnh tham số theo các điều kiện thị trường và nhu cầu giao dịch khác nhau.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các khía cạnh sau:

- Sử dụng hai đường trung bình động có chu kỳ khác nhau (nhanh và chậm) để nhận diện hướng xu hướng và tín hiệu giao cắt

- Định lượng cường độ xu hướng thông qua tính toán độ lệch giữa giá và đường trung bình động (tính bằng điểm)

- Kết hợp các mẫu hình nến (nhấn chìm, búa, sao băng, doji, v.v.) làm tín hiệu xác nhận phụ trợ

- Sử dụng chỉ báo ATR để tính toán động mức dừng lỗ và mục tiêu lợi nhuận

- Áp dụng phương pháp chốt lời một phần và trailing stop để quản lý lệnh

Ưu điểm của chiến lược

- Hệ thống có khả năng thích ứng cao, có thể điều chỉnh tham số để phù hợp với các môi trường thị trường khác nhau

- Định lượng cường độ xu hướng thông qua độ lệch, tránh giao dịch thường xuyên khi xu hướng yếu

- Kết hợp nhiều chỉ báo kỹ thuật và xác nhận mẫu hình, tăng độ tin cậy của tín hiệu giao dịch

- Áp dụng phương pháp dừng lỗ động dựa trên ATR, kiểm soát rủi ro hợp lý

- Hỗ trợ hai phương thức quản lý vốn: lãi kép và vị thế cố định

- Có chức năng chốt lời một phần và trailing stop, bảo vệ lợi nhuận hiệu quả

Rủi ro của chiến lược

- Trong thị trường đi ngang có thể phát sinh nhiều tín hiệu giả, nên thêm bộ lọc chỉ báo dao động

- Sự kết hợp nhiều chỉ báo có thể dẫn đến bỏ lỡ một số cơ hội giao dịch

- Tối ưu hóa tham số quá mức có thể dẫn đến rủi ro overfitting

- Trong thị trường có thanh khoản thấp, giao dịch khối lượng lớn có thể đối mặt rủi ro trượt giá

- Cần thiết lập tỷ lệ dừng lỗ hợp lý, tránh thua lỗ quá lớn trong một lần

Hướng tối ưu hóa chiến lược

- Có thể thêm chỉ báo khối lượng làm chỉ báo phụ trợ xác nhận xu hướng

- Xem xét đưa chỉ báo biến động thị trường để điều chỉnh động tần suất giao dịch

- Lọc tín hiệu dựa trên tính nhất quán xu hướng của các khung thời gian khác nhau

- Bổ sung thêm nhiều lựa chọn phương thức dừng lỗ, như dừng lỗ theo thời gian

- Phát triển cơ chế tối ưu hóa tham số tự động, nâng cao khả năng thích ứng của chiến lược

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch toàn diện bằng cách kết hợp đường trung bình động, định lượng cường độ xu hướng, mẫu hình nến và quản lý rủi ro động. Nó vừa duy trì sự đơn giản trong logic chiến lược, vừa nâng cao độ tin cậy của giao dịch thông qua cơ chế xác nhận nhiều lớp. Tính tùy chỉnh cao của chiến lược cho phép nó thích ứng với các phong cách giao dịch và điều kiện thị trường khác nhau, nhưng khi sử dụng cần chú ý đến tối ưu hóa tham số và kiểm soát rủi ro.

- 1