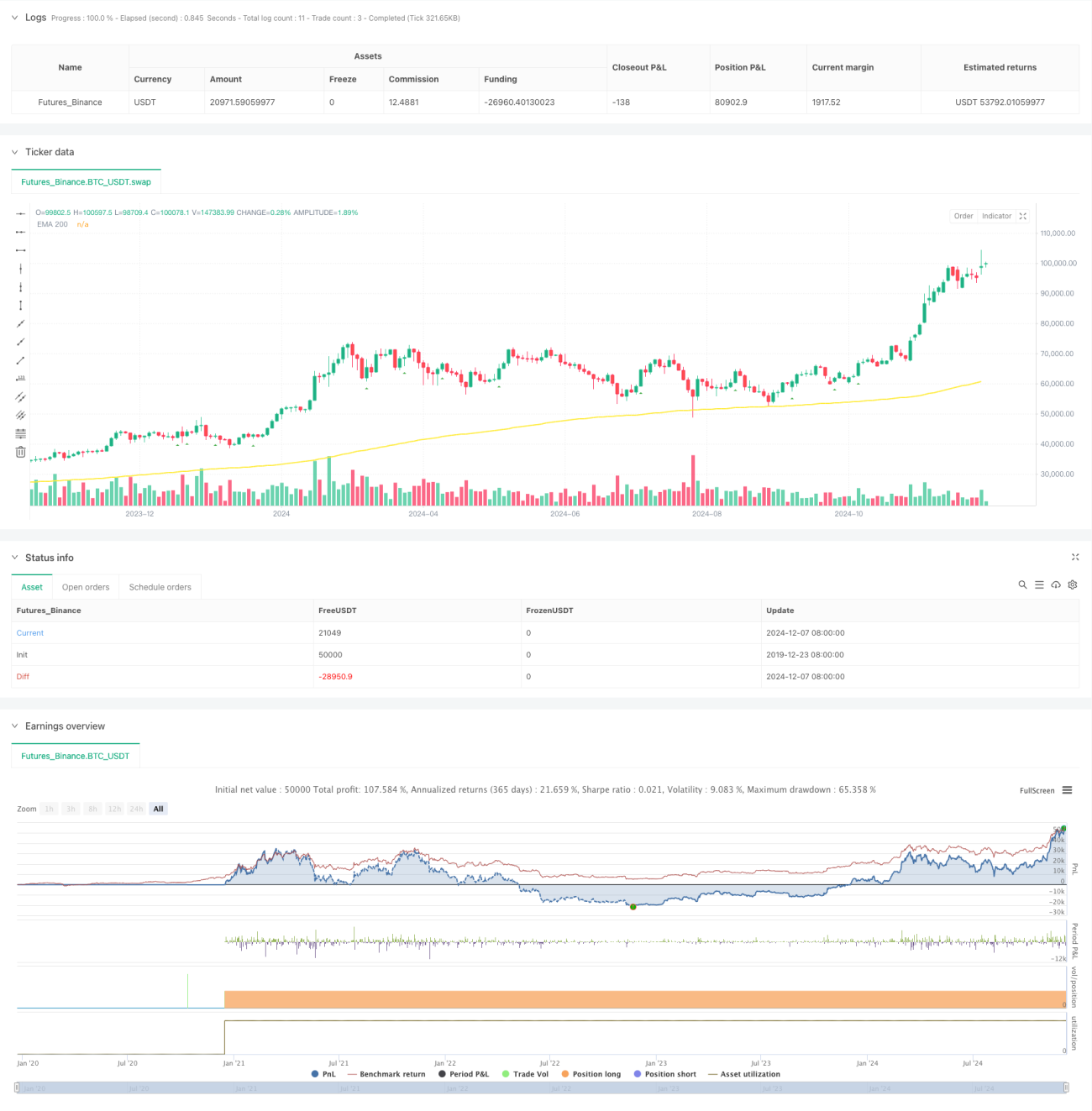

Chiến lược giao dịch xu hướng động lượng với đường trung bình động hàm mũ nâng cao

Tổng quan

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên đường trung bình động hàm mũ (EMA) và chỉ báo động lượng. Nó kết hợp tín hiệu đột phá động lượng với bộ lọc xu hướng EMA để giao dịch khi thị trường có xu hướng rõ ràng. Chiến lược bao gồm mô-đun quản lý rủi ro hoàn chỉnh, bộ lọc thời gian giao dịch linh hoạt và các chức năng phân tích thống kê chi tiết nhằm nâng cao tính ổn định và độ tin cậy của chiến lược.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Nhận diện tín hiệu động lượng: Tính toán giá trị động lượng trong khung thời gian do người dùng tùy chỉnh. Khi động lượng vượt qua ngưỡng tăng, phát tín hiệu mua (long); khi vượt qua ngưỡng giảm, phát tín hiệu bán (short).

- Bộ lọc xu hướng EMA: Sử dụng EMA kỳ 200 làm cơ sở xác định xu hướng. Giá trên EMA cho phép mua, giá dưới EMA cho phép bán.

- Bộ lọc thời gian: Có thể thiết lập khung giờ giao dịch cụ thể và hỗ trợ điều chỉnh múi giờ GMT, giúp chiến lược thích ứng tốt hơn với thời gian giao dịch của các thị trường khác nhau.

- Kiểm soát rủi ro: Hỗ trợ cài đặt dừng lỗ và chốt lời dựa trên ATR hoặc tỷ lệ phần trăm cố định, đồng thời giới hạn số lần giao dịch tối đa mỗi ngày.

Ưu điểm của chiến lược

- Khả năng bám xu hướng mạnh: Nhờ sự xác nhận kép từ EMA và động lượng, có thể nắm bắt hiệu quả các đợt xu hướng chính.

- Quản lý rủi ro hoàn chỉnh: Cung cấp nhiều phương án dừng lỗ, có thể sử dụng dừng lỗ động theo ATR hoặc dừng lỗ theo tỷ lệ phần trăm cố định.

- Phân tích thống kê toàn diện: Theo dõi thời gian thực nhiều chỉ số hiệu suất, bao gồm tỷ lệ thắng lệnh mua/bán, tỷ lệ lợi nhuận/rủi ro, v.v.

- Tham số linh hoạt có thể điều chỉnh: Các tham số chính đều có thể được tối ưu hóa và điều chỉnh theo đặc điểm của từng thị trường.

Rủi ro của chiến lược

-

Rủi ro thị trường đi ngang: Trong thị trường dao động ngang, có thể phát sinh nhiều tín hiệu đột phá giả.

Giải pháp đề xuất: Thêm bộ lọc dao động hoặc tăng ngưỡng đột phá. -

Rủi ro trượt giá: Trong giai đoạn biến động mạnh, có thể đối mặt với trượt giá lớn.

Giải pháp đề xuất: Thiết lập phạm vi dừng lỗ hợp lý, tránh giao dịch trong khung giờ biến động cao. -

Rủi ro giao dịch quá mức: Tín hiệu quá thường xuyên có thể dẫn đến giao dịch quá mức.

Giải pháp đề xuất: Thiết lập hợp lý giới hạn số lần giao dịch tối đa mỗi ngày.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số động: Có thể tự động điều chỉnh ngưỡng động lượng và chu kỳ EMA dựa trên mức độ biến động của thị trường.

- Phân tích đa khung thời gian: Thêm xác nhận xu hướng từ nhiều khung thời gian, nâng cao độ tin cậy của tín hiệu.

- Nhận diện môi trường thị trường: Bổ sung mô-đun phân tích biến động, áp dụng các thiết lập tham số khác nhau trong các môi trường thị trường khác nhau.

- Phân cấp cường độ tín hiệu: Phân loại cường độ tín hiệu đột phá, điều chỉnh quy mô vị thế linh hoạt dựa trên cường độ tín hiệu.

Tổng kết

Đây là một chiến lược giao dịch theo xu hướng được thiết kế hoàn chỉnh, kết hợp đột phá động lượng và xu hướng EMA để nắm bắt cơ hội thị trường. Chiến lược có hệ thống quản lý rủi ro đầy đủ, chức năng phân tích thống kê mạnh mẽ, mang tính thực tiễn và khả năng mở rộng tốt. Thông qua việc tối ưu hóa và hoàn thiện liên tục, chiến lược này có khả năng duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau.

- 1