Chiến lược chốt lời cắt lỗ thích ứng theo dõi drawdown cho giao dịch cân bằng

Tổng quan

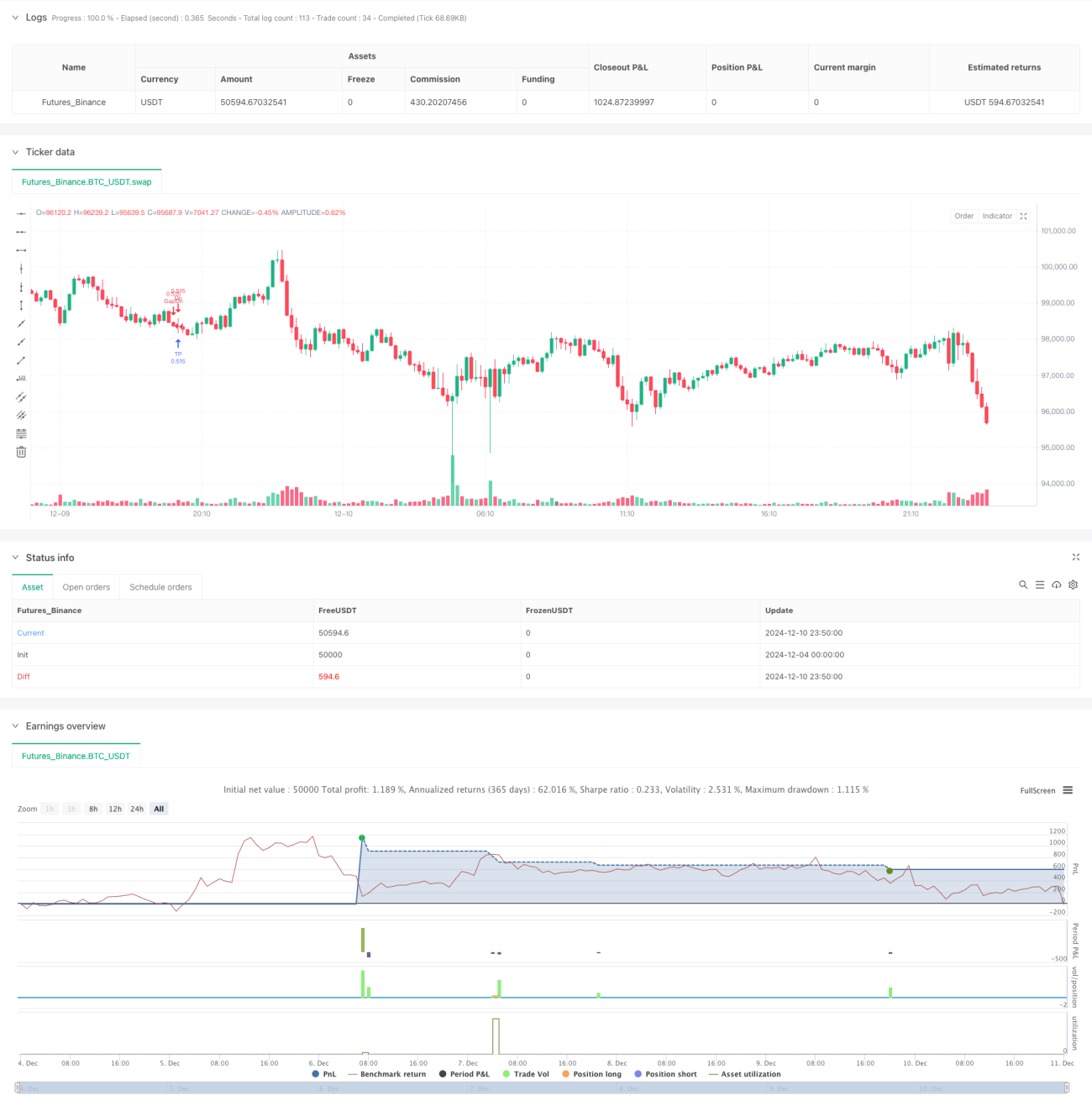

Chiến lược này là một hệ thống giao dịch thích ứng dựa trên biến động giá và các khoảng trống (gap), đạt được lợi nhuận ổn định thông qua việc thiết lập điểm vào linh hoạt và cắt lỗ/chốt lời động. Chiến lược sử dụng phương pháp tăng vị thế kiểu kim tự tháp (pyramid adding), kết hợp với hệ thống quản lý lệnh OCA để kiểm soát rủi ro. Hệ thống sẽ tự động điều chỉnh hướng nắm giữ dựa trên diễn biến thị trường và đóng vị thế cắt lỗ kịp thời khi có tín hiệu đảo chiều.

Nguyên lý chiến lược

Chiến lược hoạt động chủ yếu thông qua các cơ chế cốt lõi sau:

- Cơ chế giao dịch Gap: Nhận diện khoảng trống tăng và giảm, đặt lệnh stop-loss để vào lệnh tại vị trí gap.

- Theo dõi xu hướng: Xác định hướng xu hướng dựa trên mối quan hệ giữa giá mở cửa và giá đóng cửa.

- Tăng vị thế kim tự tháp: Cho phép nắm giữ tối đa 100 lệnh trong cùng một hướng.

- Chốt lời/Cắt lỗ động: Thiết lập mức chốt lời/cắt lỗ dựa trên giá nắm giữ trung bình.

- Quản lý lệnh OCA: Sử dụng tổ hợp lệnh OCA để đảm bảo lệnh chốt lời và cắt lỗ loại trừ lẫn nhau.

- Giới hạn giao dịch trong ngày: Kiểm soát rủi ro bằng cách đặt giới hạn số lượng lệnh khớp tối đa trong ngày.

Ưu điểm chiến lược

- Khả năng thích ứng cao: Chiến lược có thể tự động điều chỉnh hướng giao dịch và khối lượng nắm giữ theo tình hình thị trường.

- Rủi ro có thể kiểm soát: Kiểm soát rủi ro thông qua nhiều cơ chế, bao gồm cắt lỗ, lệnh OCA và giới hạn giao dịch trong ngày.

- Tính linh hoạt cao: Hỗ trợ tăng vị thế kiểu kim tự tháp, có thể thu được nhiều lợi nhuận hơn trong thị trường có xu hướng.

- Hiệu quả thực thi cao: Sử dụng lệnh stop-loss để vào lệnh, có thể nhanh chóng tạo vị thế ở các mức giá quan trọng.

- Mức độ hệ thống hóa cao: Quyết định giao dịch hoàn toàn được hệ thống hóa, giảm thiểu tác động cảm xúc từ sự can thiệp của con người.

Rủi ro chiến lược

- Rủi ro trượt giá: Có thể đối mặt với trượt giá nghiêm trọng trong điều kiện thị trường biến động nhanh.

- Rủi ro giao dịch quá mức: Vào lệnh và thoát lệnh thường xuyên có thể dẫn đến chi phí giao dịch cao.

- Rủi ro hệ thống: Có thể chịu tổn thất lớn trong thị trường biến động mạnh.

- Rủi ro quản lý vốn: Tăng vị thế kiểu kim tự tháp có thể dẫn đến tỷ lệ sử dụng vốn quá cao.

- Rủi ro kỹ thuật: Gián đoạn chương trình chạy có thể gây ra vấn đề trong quản lý lệnh.

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo biến động: Điều chỉnh tham số chốt lời/cắt lỗ một cách động dựa trên biến động thị trường.

- Tối ưu hóa cơ chế tăng vị thế: Thiết kế quy tắc tăng vị thế chi tiết hơn, tránh sử dụng vốn quá mức.

- Hoàn thiện hệ thống kiểm soát rủi ro: Bổ sung thêm các chỉ báo kiểm soát rủi ro, như giới hạn sụt giảm tối đa trong ngày.

- Cải thiện thực thi lệnh: Tối ưu hóa cơ chế chuyển tiếp lệnh, giảm tác động của trượt giá.

- Tăng cường đánh giá tâm lý thị trường: Kết hợp các chỉ báo như khối lượng giao dịch để tối ưu hóa thời điểm vào lệnh.

Tổng kết

Đây là một chiến lược giao dịch được thiết kế hợp lý, logic chặt chẽ, đảm bảo tính ổn định và an toàn của giao dịch thông qua nhiều cơ chế. Ưu điểm cốt lõi của chiến lược nằm ở khả năng thích ứng và kiểm soát rủi ro, nhưng đồng thời cũng cần chú ý đến rủi ro do biến động thị trường gây ra. Thông qua việc tối ưu hóa và hoàn thiện liên tục, chiến lược có thể duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau.

/*backtest

start: 2024-12-04 00:00:00

end: 2024-12-11 00:00:00

period: 10m

basePeriod: 10m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Greedy Strategy - maclaurin", pyramiding = 100, calc_on_order_fills=false, overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

backtestStartDate = input(timestamp("1 Jan 1990"),

title="Start Date", group="Backtest Time Period",- 1