Chiến lược đầu tư trung bình chi phí đô la với Dải Bollinger kiểu hồi quy trung bình

Tổng quan

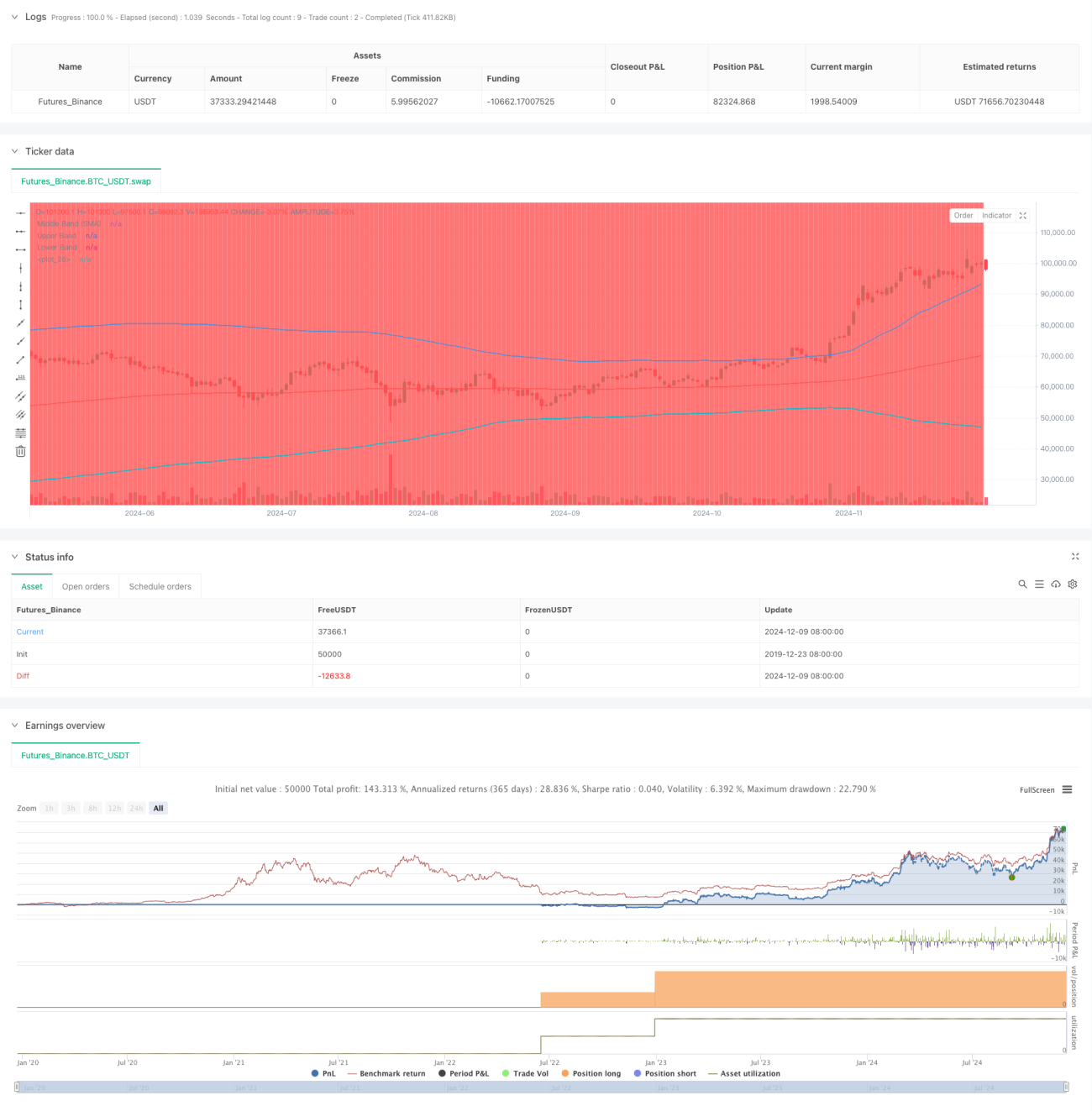

Chiến lược này là một chiến lược đầu tư thông minh kết hợp giữa phương pháp trung bình chi phí đô la (DCA) và chỉ báo Bollinger Bands. Nó xây dựng vị thế một cách có hệ thống trong các đợt điều chỉnh giá, tận dụng nguyên lý hồi quy trung bình để đầu tư. Cốt lõi của chiến lược là thực hiện mua với số tiền cố định khi giá phá vỡ dải dưới của Bollinger Bands, từ đó có được giá vào lệnh tốt hơn trong giai đoạn thị trường điều chỉnh.

Nguyên lý chiến lược

Nguyên lý cốt lõi của chiến lược dựa trên ba nền tảng: 1) Phương pháp trung bình chi phí đô la, giảm thiểu rủi ro thời điểm bằng cách đầu tư số tiền cố định định kỳ; 2) Lý thuyết hồi quy trung bình, cho rằng giá cuối cùng sẽ quay trở lại mức trung bình lịch sử của nó; 3) Chỉ báo Bollinger Bands, dùng để xác định vùng quá mua/quá bán. Khi giá phá vỡ dải dưới của Bollinger Bands sẽ kích hoạt tín hiệu mua, số lượng mua được xác định bằng số tiền đầu tư đã đặt chia cho giá hiện tại. Chiến lược sử dụng đường trung bình động hàm mũ 200 kỳ làm dải giữa của Bollinger Bands, với bội số độ lệch chuẩn là 2 để xác định dải trên và dải dưới.

Ưu điểm chiến lược

- Giảm rủi ro thời điểm - Giảm sai số do con người thông qua việc mua hệ thống thay vì phán đoán chủ quan.

- Nắm bắt cơ hội điều chỉnh - Tự động thực hiện mua khi giá giảm quá mức.

- Cài đặt tham số linh hoạt - Có thể điều chỉnh tham số Bollinger Bands và số tiền đầu tư theo các môi trường thị trường khác nhau.

- Quy tắc vào/thoát rõ ràng - Dựa trên tín hiệu khách quan từ chỉ báo kỹ thuật.

- Thực thi tự động - Không cần can thiệp thủ công, tránh giao dịch cảm tính.

Rủi ro chiến lược

- Rủi ro hồi quy trung bình thất bại - Có thể tạo ra nhiều tín hiệu sai trong thị trường xu hướng.

- Rủi ro quản lý vốn - Cần dự trữ đủ vốn để đối phó với các tín hiệu mua liên tiếp.

- Rủi ro tối ưu tham số - Tối ưu quá mức có thể khiến chiến lược mất hiệu quả.

- Phụ thuộc vào môi trường thị trường - Có thể hoạt động kém trong thị trường biến động mạnh.

Khuyến nghị áp dụng hệ thống quản lý vốn nghiêm ngặt và đánh giá hiệu suất chiến lược định kỳ để quản lý các rủi ro này.

Hướng tối ưu chiến lược

- Đưa vào bộ lọc xu hướng, tránh giao dịch ngược xu hướng mạnh.

- Thêm cơ chế xác nhận đa khung thời gian.

- Tối ưu hệ thống quản lý vốn, điều chỉnh số tiền đầu tư động theo biến động.

- Thêm cơ chế chốt lời, chốt lời khi giá hồi quy về mức trung bình.

- Cân nhắc kết hợp các chỉ báo kỹ thuật khác để tăng độ tin cậy của tín hiệu.

Tổng kết

Đây là một chiến lược vững chắc kết hợp giữa phân tích kỹ thuật và phương pháp đầu tư hệ thống. Bằng cách sử dụng Bollinger Bands để xác định cơ hội giảm quá mức, kết hợp với phương pháp trung bình chi phí đô la để giảm rủi ro. Chìa khóa thành công của chiến lược nằm ở việc thiết lập tham số hợp lý và kỷ luật thực thi nghiêm ngặt. Mặc dù có một số rủi ro nhất định, nhưng thông qua tối ưu hóa liên tục và quản lý rủi ro, có thể nâng cao tính ổn định của chiến lược.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("DCA Strategy with Mean Reversion and Bollinger Band", overlay=true) // Define the strategy name and set overlay=true to display on the main chart

// Inputs for investment amount and dates- 1