Tổng quan chiến lược

Chiến lược này là một hệ thống giao dịch theo xu hướng và đảo chiều dựa trên điểm cân bằng giá. Nó xác định giá cân bằng bằng cách tính giá trị trung bình của mức cao nhất và thấp nhất trong X nến trước đó, sau đó xác định hướng xu hướng dựa trên vị trí của giá đóng cửa so với giá cân bằng. Khi giá liên tục duy trì ở một phía của giá cân bằng trong một số nến nhất định, hệ thống sẽ xác nhận xu hướng hình thành. Tại lần điều chỉnh đầu tiên (giá phá vỡ giá cân bằng), hệ thống sẽ tìm kiếm cơ hội vào lệnh. Chiến lược này có thể chọn chế độ giao dịch theo xu hướng hoặc giao dịch đảo chiều tùy theo cài đặt.

Nguyên lý chiến lược

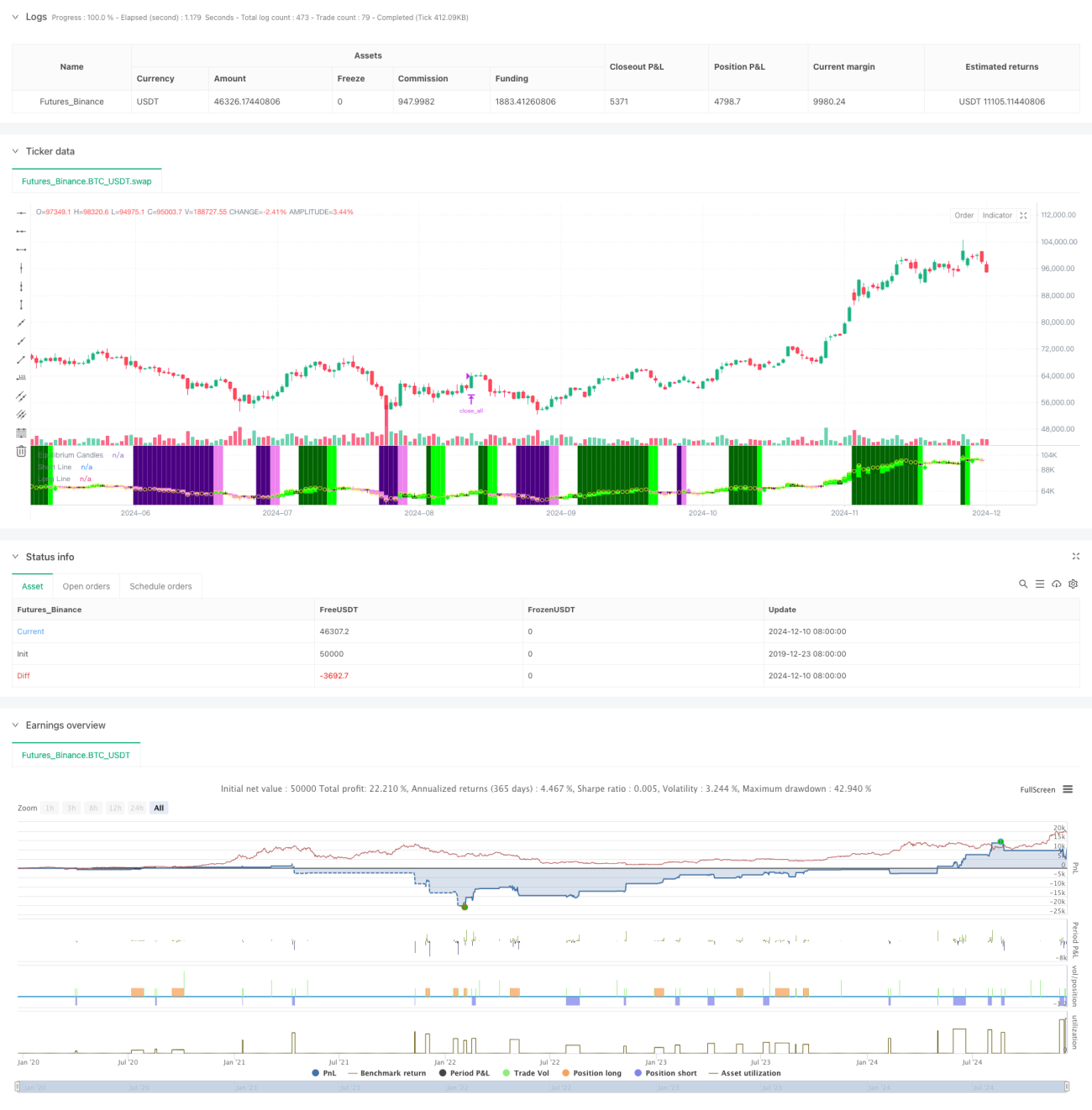

- Tính giá cân bằng: Sử dụng điểm giữa của mức cao nhất và thấp nhất trong X nến trước đó làm giá cân bằng, tương tự phương pháp tính đường cơ sở của Ichimoku Kinko Hyo.

- Xác định xu hướng: Khi giá duy trì liên tục ở cùng một phía của giá cân bằng trong X nến (mặc định 7 nến), xác nhận xu hướng hình thành.

- Tín hiệu vào lệnh: Kích hoạt tín hiệu vào lệnh tại lần điều chỉnh đầu tiên sau khi xu hướng được xác nhận (giá phá vỡ giá cân bằng).

- Cắt lỗ và chốt lời: Sử dụng phân vị 60% của ATR để điều chỉnh khoảng cách cắt lỗ và chốt lời một cách linh hoạt, cung cấp sự linh hoạt trong quản lý rủi ro.

- Bảo vệ biến động lớn: Khi giá lệch khỏi điểm cân bằng vượt quá bội số ATR đã cài đặt, hệ thống sẽ tự động đóng vị thế để ngăn ngừa drawdown lớn.

Ưu điểm chiến lược

- Khả năng thích ứng cao: Có thể linh hoạt chuyển đổi giữa chế độ giao dịch theo xu hướng và giao dịch đảo chiều dựa trên đặc điểm thị trường.

- Quản lý rủi ro hoàn chỉnh: Sử dụng cắt lỗ động dựa trên ATR và có cơ chế bảo vệ biến động lớn.

- Thao tác rõ ràng: Tín hiệu giao dịch minh bạch, không phụ thuộc vào tổ hợp chỉ báo kỹ thuật phức tạp.

- Hiệu quả trực quan tốt: Sử dụng nến màu và nền trực quan để hiển thị trạng thái thị trường một cách trực quan.

- Thân thiện với tự động hóa: Có thể dễ dàng kết nối với các nền tảng giao dịch như MT5 để thực hiện giao dịch tự động.

Rủi ro chiến lược

- Rủi ro thị trường đi ngang: Có thể tạo ra nhiều tín hiệu giả trong thị trường đi ngang tích lũy.

- Ảnh hưởng của trượt giá: Có thể đối mặt với trượt giá lớn trong điều kiện biến động mạnh.

- Nhạy cảm với tham số: Các tham số cốt lõi như chu kỳ cân bằng, chu kỳ xác định xu hướng cần được tối ưu hóa cẩn thận cho từng thị trường.

- Rủi ro chuyển đổi thị trường: Giai đoạn chuyển đổi từ thị trường xu hướng sang đi ngang có thể gây ra drawdown lớn.

Hướng tối ưu hóa chiến lược

- Nhận dạng môi trường thị trường: Thêm module đánh giá môi trường thị trường, điều chỉnh động các tham số chiến lược trong các điều kiện thị trường khác nhau.

- Lọc tín hiệu: Cân nhắc thêm các chỉ báo phụ trợ như khối lượng, độ biến động để lọc tín hiệu giả.

- Quản lý vị thế: Giới thiệu cơ chế quản lý vị thế phức tạp hơn, như điều chỉnh động dựa trên biến động.

- Đa khung thời gian: Tích hợp tín hiệu từ nhiều khung thời gian để nâng cao độ chính xác của giao dịch.

- Tối ưu hóa chi phí giao dịch: Tối ưu hóa thời điểm vào và ra lệnh dựa trên đặc điểm chi phí của từng sản phẩm giao dịch.

Kết luận

Đây là một hệ thống giao dịch xu hướng được thiết kế hợp lý, cung cấp logic giao dịch rõ ràng thông qua khái niệm cốt lõi là giá cân bằng. Đặc điểm lớn nhất của chiến lược này là tính linh hoạt cao, có thể được sử dụng cho cả giao dịch theo xu hướng và giao dịch đảo chiều, đồng thời có cơ chế quản lý rủi ro hoàn chỉnh. Mặc dù có thể đối mặt với thách thức trong một số điều kiện thị trường nhất định, nhưng thông qua tối ưu hóa liên tục và điều chỉnh linh hoạt, chiến lược này có thể duy trì hiệu suất ổn định trong nhiều môi trường thị trường khác nhau.

- 1