Chiến lược Theo dõi Xu hướng Cao cấp với Cắt lỗ Thích ứng Tự động

Tổng quan

Đây là một chiến lược giao dịch theo xu hướng dựa trên chỉ báo Supertrend, kết hợp với cơ chế trailing stop thích ứng. Chiến lược này chủ yếu xác định hướng xu hướng thị trường thông qua chỉ báo Supertrend, đồng thời sử dụng trailing stop được điều chỉnh linh hoạt để quản lý rủi ro và tối ưu hóa thời điểm thoát lệnh. Chiến lược hỗ trợ nhiều phương pháp cắt lỗ, bao gồm cắt lỗ theo phần trăm, cắt lỗ theo ATR và cắt lỗ theo số pip cố định, có thể linh hoạt điều chỉnh tùy theo môi trường thị trường khác nhau.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Sử dụng chỉ báo Supertrend làm cơ sở chính để xác định xu hướng, chỉ báo này kết hợp ATR (Dải biên độ thực trung bình) để đo lường biến động thị trường

- Tín hiệu vào lệnh được kích hoạt bởi sự thay đổi hướng của Supertrend, hỗ trợ giao dịch mua, bán hoặc cả hai chiều

- Cơ chế cắt lỗ sử dụng trailing stop thích ứng, có thể tự động điều chỉnh vị trí cắt lỗ dựa trên biến động thị trường

- Hệ thống quản lý giao dịch bao gồm quản lý vị thế (mặc định 15% tài khoản) và cơ chế lọc thời gian

Ưu điểm của chiến lược

- Khả năng bắt xu hướng mạnh mẽ: Thông qua chỉ báo Supertrend, có thể xác định hiệu quả xu hướng chính, giảm thiểu đánh giá sai

- Kiểm soát rủi ro hoàn thiện: Sử dụng cơ chế cắt lỗ đa dạng, có thể thích ứng với các môi trường thị trường khác nhau

- Tính linh hoạt cao: Hỗ trợ cấu hình nhiều hướng giao dịch và phương pháp cắt lỗ

- Khả năng thích ứng mạnh mẽ: Trailing stop tự động điều chỉnh theo biến động thị trường, nâng cao khả năng thích ứng của chiến lược

- Hệ thống backtest hoàn chỉnh: Tích hợp chức năng lọc thời gian, thuận tiện cho việc phân tích hiệu suất trong quá khứ

Rủi ro của chiến lược

- Rủi ro đảo chiều xu hướng: Có thể xuất hiện tín hiệu giả trong thị trường biến động mạnh

- Rủi ro trượt giá: Việc thực hiện trailing stop có thể bị ảnh hưởng bởi tính thanh khoản thị trường

- Nhạy cảm với tham số: Cài đặt factor và chu kỳ ATR của Supertrend ảnh hưởng lớn đến hiệu suất chiến lược

- Phụ thuộc vào môi trường thị trường: Trong thị trường đi ngang, có thể giao dịch thường xuyên dẫn đến tăng chi phí

Hướng tối ưu hóa chiến lược

- Tối ưu hóa lọc tín hiệu: Có thể thêm các chỉ báo kỹ thuật bổ sung để lọc tín hiệu giả

- Tối ưu hóa quản lý vị thế: Có thể điều chỉnh tỷ lệ nắm giữ một cách linh hoạt dựa trên biến động thị trường

- Tăng cường cơ chế cắt lỗ: Có thể kết hợp giá vốn trung bình để thiết kế logic cắt lỗ phức tạp hơn

- Tối ưu hóa thời điểm vào lệnh: Có thể bổ sung phân tích cấu trúc giá để nâng cao độ chính xác khi vào lệnh

- Hoàn thiện hệ thống backtest: Có thể thêm nhiều chỉ số thống kê hơn để đánh giá hiệu suất chiến lược

Tổng kết

Đây là một chiến lược giao dịch theo xu hướng được thiết kế hợp lý, có thể kiểm soát rủi ro. Bằng cách kết hợp chỉ báo Supertrend và cơ chế cắt lỗ linh hoạt, chiến lược có thể duy trì khả năng sinh lời cao đồng thời kiểm soát rủi ro hiệu quả. Chiến lược có tính cấu hình cao, phù hợp để sử dụng trong các môi trường thị trường khác nhau, nhưng cần được tối ưu hóa tham số và kiểm chứng backtest đầy đủ. Trong tương lai, có thể nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược bằng cách thêm nhiều công cụ phân tích kỹ thuật và biện pháp kiểm soát rủi ro.

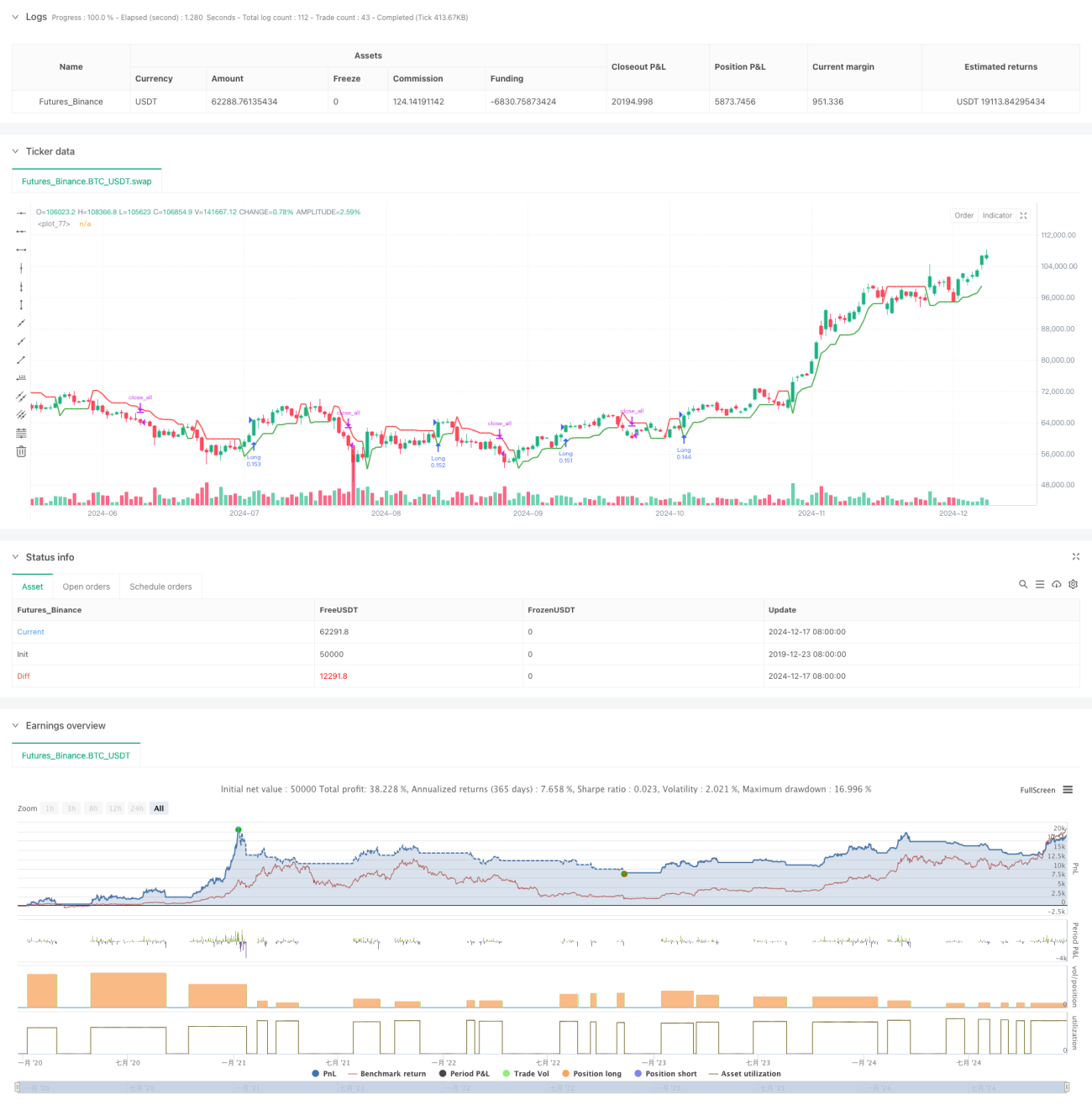

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Supertrend Strategy with Adjustable Trailing Stop [Bips]", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15)

// Inputs- 1