Chiến lược định lượng bản đồ nhiệt trung tâm thanh khoản đa khung thời gian

Tổng quan

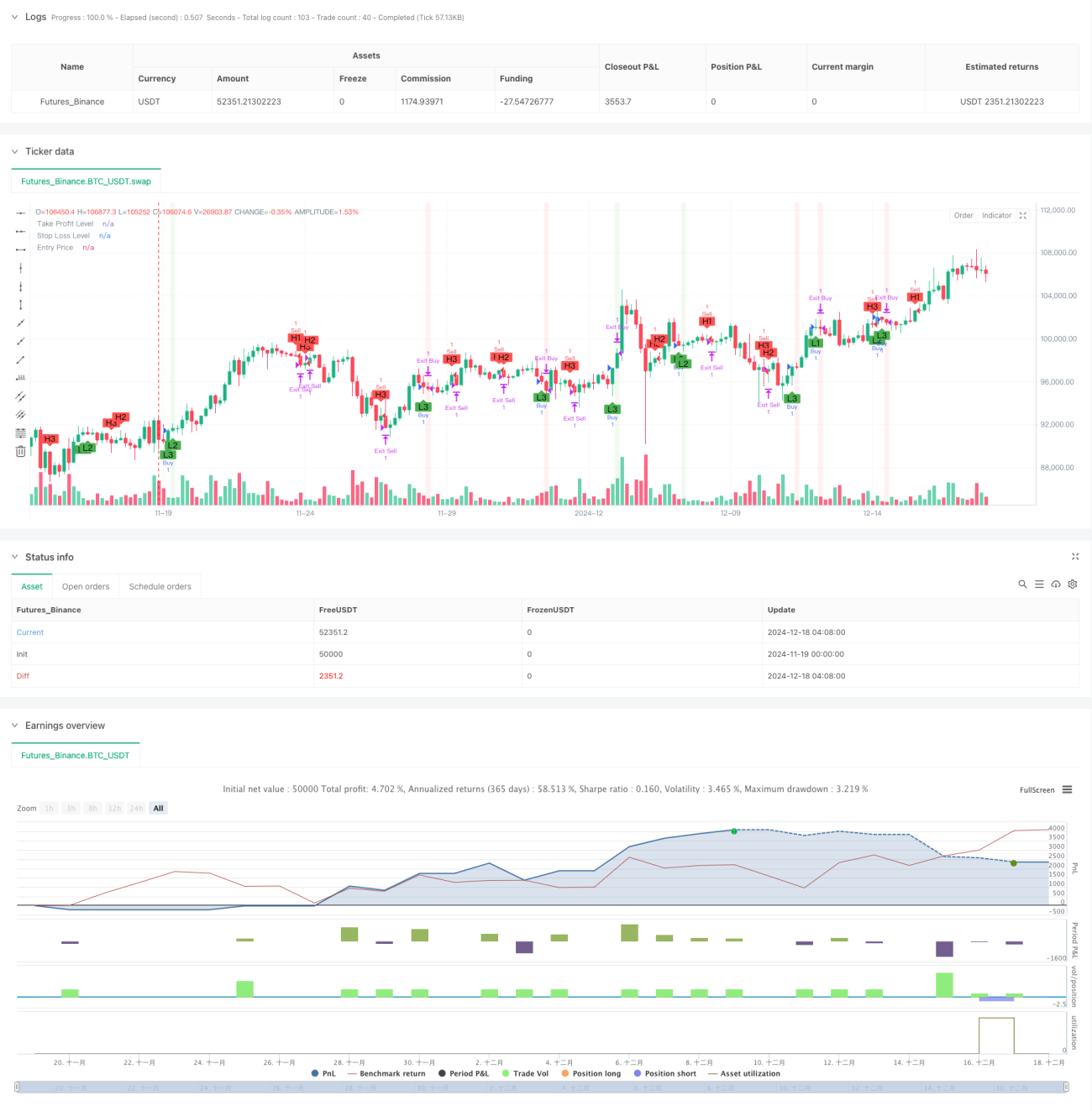

Chiến lược này là một hệ thống giao dịch định lượng dựa trên phát hiện điểm xoay (liquidity pivot) đa khung thời gian. Nó phân tích hành vi giá trên ba khung thời gian khác nhau (15 phút, 1 giờ và 4 giờ) để xác định các mức hỗ trợ và kháng cự quan trọng, từ đó đưa ra quyết định giao dịch. Hệ thống tích hợp chức năng quản lý vốn, bao gồm cài đặt chốt lời/cắt lỗ theo số tiền cố định, đồng thời cung cấp phản hồi trực quan trực quan, giúp nhà giao dịch hiểu rõ hơn về cấu trúc thị trường.

Nguyên lý chiến lược

Cốt lõi của chiến lược là sử dụng các hàm ta.pivothigh và ta.pivotlow để phát hiện các điểm xoay giá trên nhiều khung thời gian. Đối với mỗi khung thời gian, hệ thống sử dụng số nến tham chiếu trái phải (mặc định là 7) để xác định các đỉnh và đáy đáng kể. Khi xuất hiện đáy xoay mới trên bất kỳ khung thời gian nào, hệ thống tạo tín hiệu LONG; khi xuất hiện đỉnh xoay mới, hệ thống tạo tín hiệu SHORT. Việc thực hiện giao dịch sử dụng quản lý chốt lời/cắt lỗ theo số tiền cố định, thông qua hàm moneyToSLPoints để chuyển đổi số tiền USD thành số điểm tương ứng.

Lợi thế của chiến lược

- Phân tích đa khung thời gian cung cấp góc nhìn thị trường toàn diện hơn, giúp nắm bắt các cơ hội giao dịch ở các cấp độ khác nhau.

- Logic giao dịch dựa trên điểm xoay có nền tảng phân tích kỹ thuật vững chắc, dễ hiểu và dễ thực hiện.

- Chức năng quản lý vốn tích hợp giúp kiểm soát rủi ro hiệu quả cho mỗi giao dịch.

- Giao diện trực quan hiển thị trạng thái giao dịch, bao gồm vị trí, mức chốt lời/cắt lỗ và vùng lãi/lỗ.

- Các tham số chiến lược có thể điều chỉnh, khả năng thích ứng cao, có thể tối ưu hóa theo các điều kiện thị trường khác nhau.

Rủi ro của chiến lược

- Tín hiệu đa khung thời gian có thể xung đột, cần thiết lập cơ chế ưu tiên tín hiệu hợp lý.

- Chốt lời/cắt lỗ theo số tiền cố định có thể không phù hợp với mọi điều kiện thị trường, khuyến nghị điều chỉnh linh hoạt dựa trên biến động.

- Độ trễ trong phát hiện điểm xoay có thể dẫn đến thời điểm vào lệnh bị chậm.

- Trong thời kỳ biến động mạnh, có thể xuất hiện tín hiệu phá vỡ giả.

- Cần lưu ý sự khác biệt về thanh khoản giữa các khung thời gian.

Hướng tối ưu hóa chiến lược

- Đưa chỉ báo biến động vào, điều chỉnh linh hoạt mức chốt lời/cắt lỗ.

- Thêm cơ chế xác nhận khối lượng giao dịch, tăng độ tin cậy của các điểm xoay.

- Phát triển hệ thống ưu tiên khung thời gian, giải quyết vấn đề xung đột tín hiệu.

- Tích hợp bộ lọc xu hướng, tránh giao dịch quá mức trong thị trường đi ngang.

- Cân nhắc thêm phân tích cấu trúc giá, nâng cao độ chính xác của thời điểm vào lệnh.

Tổng kết

Chiến lược định lượng nhiệt độ điểm xoay thanh khoản đa khung thời gian là một hệ thống giao dịch có cấu trúc hoàn chỉnh và logic rõ ràng. Nó cung cấp một khuôn khổ giao dịch đáng tin cậy cho các nhà giao dịch thông qua phân tích thị trường đa chiều và quản lý rủi ro nghiêm ngặt. Mặc dù tồn tại một số rủi ro và hạn chế cố hữu, nhưng thông qua việc tối ưu hóa và cải tiến liên tục, chiến lược này hứa hẹn duy trì hiệu suất ổn định trong nhiều điều kiện thị trường khác nhau.

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pmotta41

//@version=5

strategy("GPT Session Liquidity Heatmap Strategy", overlay=true)- 1