动态趋势动量优化策略结合G通道指标

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng cao cấp kết hợp các chỉ báo G Channel, RSI và MACD. Nó xác định các cơ hội giao dịch có xác suất cao bằng cách tính toán động các vùng hỗ trợ và kháng cự, kết hợp với các chỉ báo động lượng. Cốt lõi của chiến lược là sử dụng chỉ báo G Channel tùy chỉnh để xác định xu hướng thị trường, đồng thời sử dụng RSI và MACD để xác nhận sự thay đổi động lượng, từ đó tạo ra các tín hiệu giao dịch chính xác hơn.

Nguyên lý chiến lược

Chiến lược áp dụng cơ chế lọc ba lớp để đảm bảo độ tin cậy của tín hiệu giao dịch. Đầu tiên, G Channel xây dựng động các vùng hỗ trợ và kháng cự bằng cách tính toán giá cao nhất và thấp nhất trong một chu kỳ xác định. Khi giá phá vỡ kênh, hệ thống sẽ nhận diện các điểm đảo chiều xu hướng tiềm năng. Thứ hai, chỉ báo RSI được sử dụng để xác nhận thị trường có đang ở trạng thái quá mua hay quá bán, giúp chọn lọc các cơ hội giao dịch giá trị hơn. Cuối cùng, chỉ báo MACD xác nhận hướng và sức mạnh của động lượng thông qua giá trị dương/âm của biểu đồ cột. Chỉ khi cả ba điều kiện này đều thỏa mãn, hệ thống mới phát tín hiệu giao dịch.

Lợi thế của chiến lược

- Cơ chế xác nhận tín hiệu đa chiều giúp tăng đáng kể độ chính xác của giao dịch

- Cài đặt dừng lỗ và chốt lời linh hoạt, kiểm soát rủi ro hiệu quả

- Tính thích ứng của G Channel giúp chiến lược thích nghi với các môi trường thị trường khác nhau

- Hệ thống quản lý rủi ro hoàn chỉnh, bao gồm quản lý vị thế và quản lý vốn

- Hệ thống nhãn trực quan hiển thị tín hiệu giao dịch, thuận tiện cho việc phân tích và tối ưu hóa

Rủi ro của chiến lược

- Có thể phát sinh tín hiệu nhiễu trong thị trường đi ngang, cần nhận diện môi trường thị trường

- Tối ưu hóa tham số quá mức có thể dẫn đến rủi ro quá khớp

- Nhiều chỉ báo có thể gây ra hiệu ứng trễ trong giai đoạn biến động cao

- Cài đặt mức dừng lỗ không phù hợp có thể dẫn đến sụt giảm quá lớn

Hướng tối ưu hóa chiến lược

- Đưa vào mô-đun nhận diện môi trường thị trường, sử dụng các tham số khác nhau trong các trạng thái thị trường khác nhau

- Phát triển cơ chế dừng lỗ thích ứng, điều chỉnh linh hoạt mức dừng lỗ dựa trên biến động thị trường

- Thêm các chỉ báo phân tích khối lượng giao dịch để tăng độ tin cậy của tín hiệu

- Tối ưu hóa phương pháp tính toán G Channel để giảm hiệu ứng trễ

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách kết hợp tổng hợp nhiều chỉ báo kỹ thuật. Lợi thế cốt lõi nằm ở cơ chế xác nhận tín hiệu đa chiều và hệ thống quản lý rủi ro hoàn chỉnh. Thông qua việc liên tục tối ưu hóa và cải tiến, chiến lược có tiềm năng duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau. Khuyến nghị nhà giao dịch nên kiểm tra đầy đủ các tổ hợp tham số khác nhau trước khi giao dịch thực tế và điều chỉnh phù hợp dựa trên đặc điểm cụ thể của thị trường.

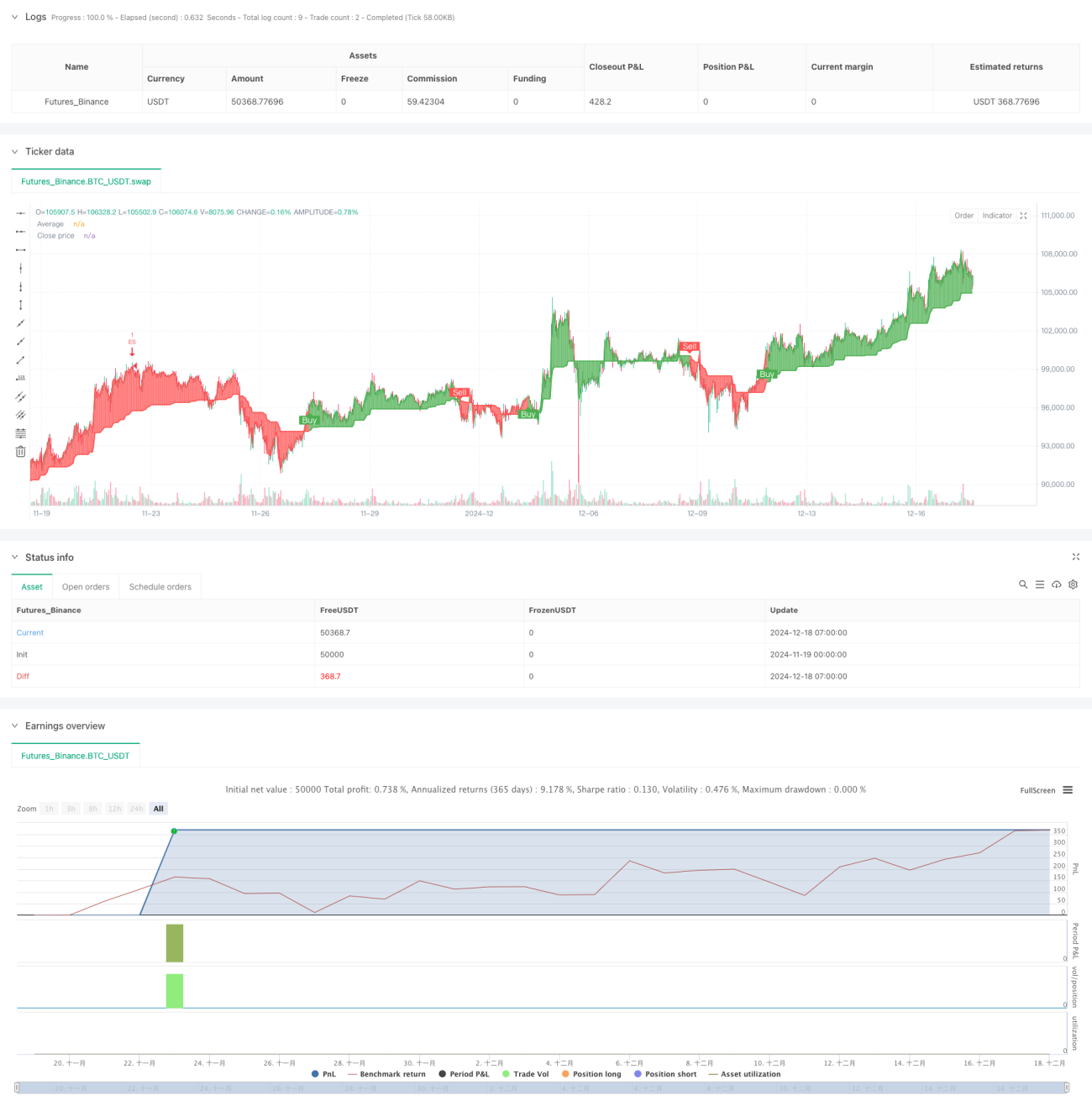

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("VinSpace Optimized Strategy", shorttitle="VinSpace Magic", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input Parameters- 1