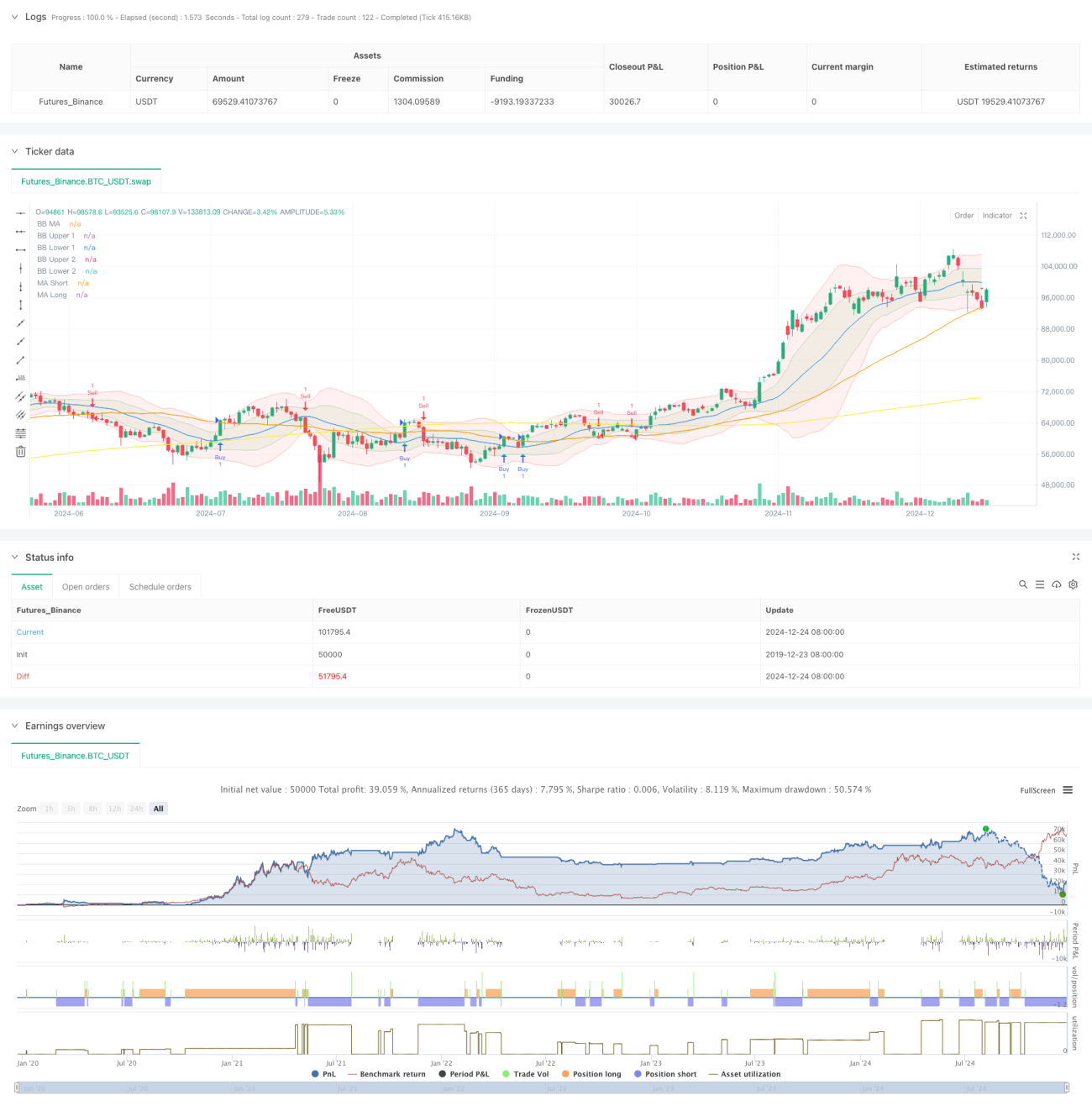

Tổng quan

Chiến lược này là một hệ thống giao dịch đa chỉ báo kết hợp Dải Bollinger (Bollinger Bands), Chỉ số Kênh Hàng hóa Woodies (Woodies CCI), Đường trung bình động (MA) và Chỉ số Khối lượng Cân bằng (OBV). Chiến lược sử dụng Dải Bollinger để cung cấp vùng biến động thị trường, dùng chỉ báo CCI để lọc tín hiệu giao dịch, kết hợp với hệ thống đường trung bình và xác nhận khối lượng, từ đó giao dịch khi xu hướng thị trường rõ ràng. Đồng thời sử dụng ATR để đặt chốt lời và cắt lỗ động, kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Sử dụng dải Bollinger hai độ lệch chuẩn (1 lần và 2 lần) để xây dựng kênh biến động giá, cung cấp tham chiếu phạm vi biến động thị trường

- Sử dụng chỉ báo CCI chu kỳ 6 và 14 làm bộ lọc tín hiệu, yêu cầu CCI của hai chu kỳ xác nhận cùng chiều

- Kết hợp đường trung bình động 50 và 200 chu kỳ để xác định xu hướng thị trường, tạo tín hiệu giao dịch ban đầu khi các đường trung bình cắt nhau

- Xác nhận xu hướng khối lượng thông qua làm mịn 10 chu kỳ của chỉ báo OBV

- Sử dụng ATR 14 chu kỳ để đặt chốt lời và cắt lỗ động, chốt lời vị thế mua là 2 lần ATR, cắt lỗ là 1 lần ATR, vị thế bán ngược lại

Ưu điểm của chiến lược

- Xác nhận chéo đa chỉ báo, giảm đáng kể xác suất tín hiệu giả

- Kết hợp Dải Bollinger và CCI cung cấp đánh giá biến động thị trường chính xác

- Hệ thống đường trung bình ngắn và dài nắm bắt hiệu quả xu hướng lớn

- OBV xác nhận hỗ trợ khối lượng giao dịch, tăng độ tin cậy của tín hiệu

- Thiết lập chốt lời/cắt lỗ động, thích ứng với các môi trường thị trường khác nhau

- Tín hiệu giao dịch rõ ràng, tiêu chuẩn thực hiện, dễ dàng định lượng

Rủi ro của chiến lược

- Đa chỉ báo có thể dẫn đến tín hiệu chậm, bỏ lỡ thời điểm vào lệnh tốt nhất

- Trong thị trường dao động, có thể kích hoạt cắt lỗ thường xuyên

- Tối ưu hóa tham số có nguy cơ quá khớp (overfitting)

- Trong thời kỳ biến động mạnh, cắt lỗ có thể không kịp thời

Biện pháp khắc phục:

- Điều chỉnh động tham số chỉ báo theo chu kỳ thị trường khác nhau

- Giám sát drawdown theo thời gian thực, kiểm soát vị thế

- Kiểm tra định kỳ hiệu quả của tham số

- Thiết lập giới hạn thua lỗ tối đa

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo biến động thị trường, điều chỉnh vị thế trong thời kỳ biến động cao

- Thêm bộ lọc cường độ xu hướng, tránh giao dịch trong thị trường dao động

- Tối ưu lựa chọn chu kỳ CCI, tăng độ nhạy của tín hiệu

- Hoàn thiện cơ chế chốt lời/cắt lỗ, ví dụ xem xét chốt lời theo từng phần

- Thêm cơ chế cảnh báo khối lượng giao dịch bất thường

Tổng kết

Đây là một hệ thống giao dịch hoàn chỉnh dựa trên tổ hợp chỉ báo kỹ thuật, nâng cao độ chính xác giao dịch thông qua xác nhận đa tín hiệu. Chiến lược được thiết kế hợp lý, kiểm soát rủi ro tốt, có giá trị ứng dụng thực tế cao. Khuyến nghị thử nghiệm với vị thế thận trọng trong giao dịch thực tế và liên tục tối ưu tham số theo tình hình thị trường.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-25 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy(shorttitle="BB Debug + Woodies CCI Filter", title="Debug Buy/Sell Signals with Woodies CCI Filter", overlay=true)

// Input Parameters- 1