Hệ thống giao dịch xu hướng kết hợp giao cắt nhiều đường trung bình động với hỗ trợ kháng cự Camarilla

Tổng quan

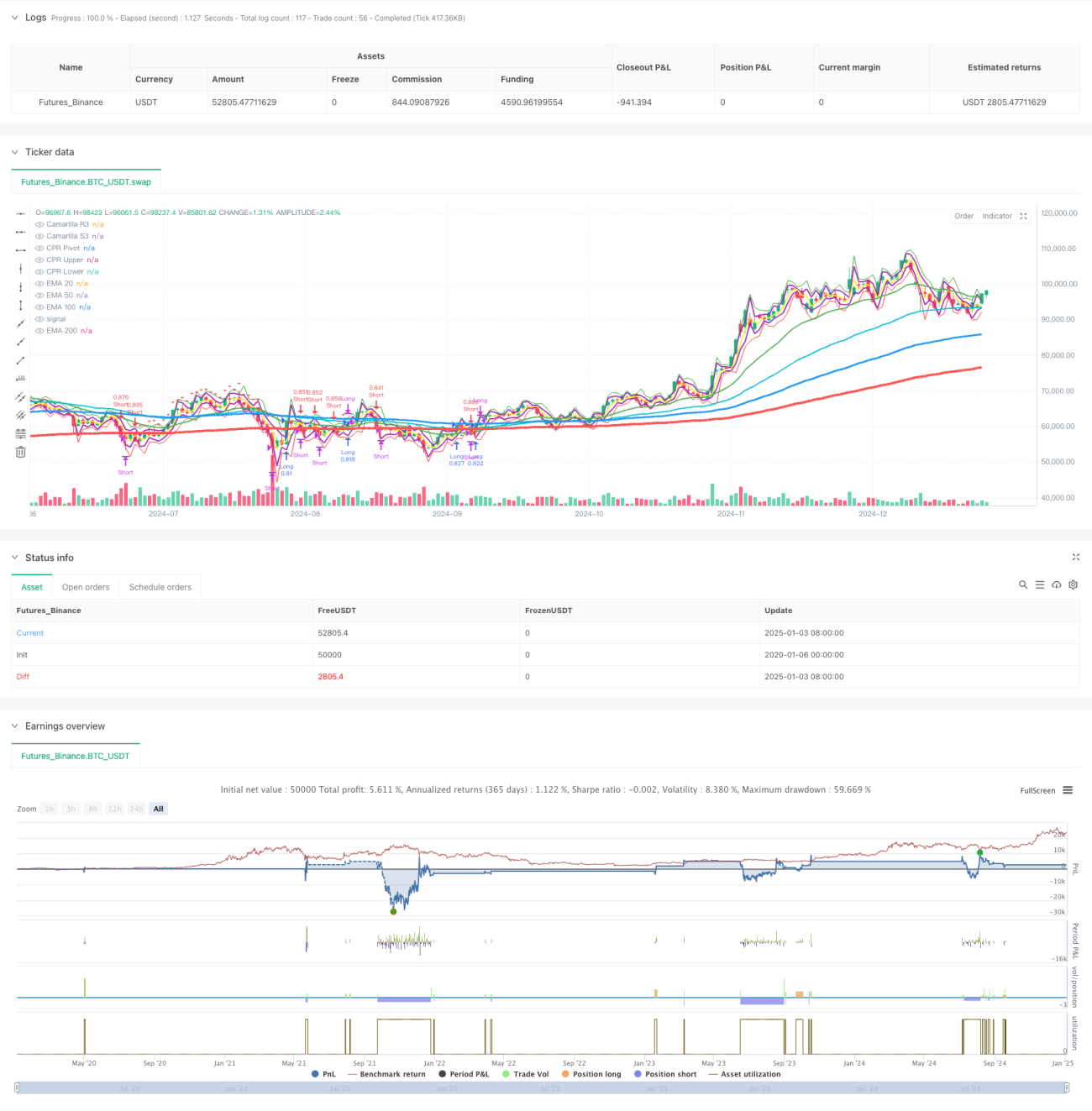

Chiến lược này là một hệ thống giao dịch theo xu hướng kết hợp nhiều đường trung bình động hàm mũ (EMA), các mức hỗ trợ/kháng cự Camarilla và phạm vi trung tâm (CPR). Chiến lược xác định xu hướng thị trường và cơ hội giao dịch tiềm năng thông qua phân tích mối quan hệ giữa giá với nhiều đường trung bình và các vùng giá quan trọng. Hệ thống áp dụng các biện pháp quản lý vốn và kiểm soát rủi ro chặt chẽ, bao gồm quy mô vị thế theo tỷ lệ phần trăm và cơ chế thoát lệnh đa dạng.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa trên các thành phần cốt lõi sau:

- Hệ thống đa đường trung bình (EMA20/50/100/200) dùng để xác định hướng và cường độ xu hướng

- Các mức hỗ trợ/kháng cự Camarilla (R3/S3) dùng để xác định các mức giá quan trọng

- Phạm vi trung tâm (CPR) dùng để xác định vùng giao dịch trong ngày

- Tín hiệu vào lệnh dựa trên sự giao cắt giữa giá và EMA200, kết hợp xác nhận từ EMA20

- Chiến lược thoát lệnh bao gồm hai chế độ: di chuyển cố định theo điểm và di chuyển theo tỷ lệ phần trăm

- Hệ thống quản lý vốn điều chỉnh động quy mô vị thế dựa trên quy mô tài khoản

Ưu điểm chiến lược

- Sự kết hợp của các chỉ báo kỹ thuật đa chiều cung cấp tín hiệu giao dịch đáng tin cậy hơn

- Cơ chế thoát lệnh linh hoạt thích ứng với các điều kiện thị trường khác nhau

- Hệ thống quản lý vốn hoàn chỉnh kiểm soát rủi ro hiệu quả

- Đặc tính bám theo xu hướng giúp nắm bắt các biến động lớn

- Các thành phần trực quan giúp nhà giao dịch dễ dàng hiểu cấu trúc thị trường

Rủi ro chiến lược

- Có thể phát sinh tín hiệu giả trong thị trường đi ngang

- Nhiều chỉ báo có thể dẫn đến tín hiệu giao dịch bị trễ

- Điểm thoát cố định có thể hoạt động kém hiệu quả trong thị trường biến động cao

- Cần quy mô vốn lớn để chịu được sự sụt giảm

- Chi phí giao dịch có thể ảnh hưởng đến lợi nhuận tổng thể của chiến lược

Hướng tối ưu hóa chiến lược

- Đưa chỉ báo biến động để điều chỉnh động các tham số vào/ra lệnh

- Thêm mô-đun nhận diện trạng thái thị trường để thích ứng với các môi trường thị trường khác nhau

- Tối ưu hóa hệ thống quản lý vốn, bổ sung quản lý vị thế động

- Thêm bộ lọc thời gian giao dịch để nâng cao chất lượng tín hiệu

- Cân nhắc thêm phân tích khối lượng để tăng cường độ tin cậy của tín hiệu

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách tích hợp nhiều công cụ phân tích kỹ thuật cổ điển. Ưu điểm của hệ thống nằm ở phân tích thị trường đa chiều và quản lý rủi ro chặt chẽ, nhưng cũng cần chú ý đến khả năng thích ứng với các môi trường thị trường khác nhau. Thông qua tối ưu hóa và cải tiến liên tục, chiến lược có tiềm năng nâng cao lợi nhuận trong khi vẫn duy trì sự ổn định.

- 1