Chiến lược giao dịch chốt lời động đa cấp dựa trên chỉ báo Bollinger và bộ lọc phân vị khối lượng

Tổng quan

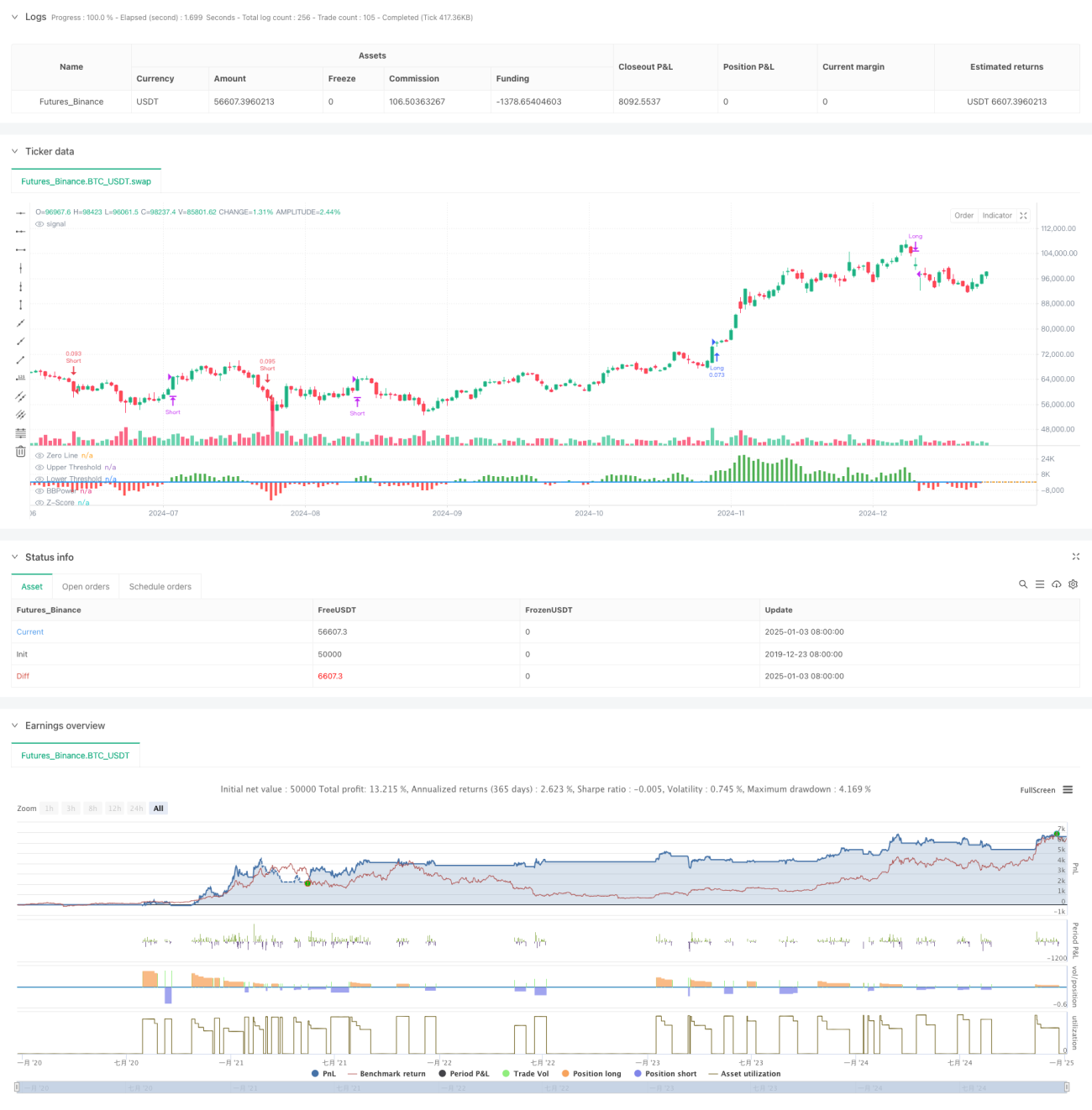

Chiến lược này là một hệ thống giao dịch định lượng kết hợp chỉ báo Bull Bear Power (BBP) và hệ thống chốt lời động đa cấp dựa trên phân vị khối lượng. Bằng cách phân tích dữ liệu đa chiều như giá, khối lượng và động lượng, chiến lược xây dựng một hệ thống giao dịch có khả năng thích ứng cao và kiểm soát rủi ro tốt. Logic cốt lõi bao gồm sử dụng giá trị Z-Score chuẩn hóa của chỉ báo BBP làm điều kiện kích hoạt tín hiệu giao dịch, kết hợp phân tích phân vị khối lượng để điều chỉnh linh hoạt mức chốt lời, nhờ đó nắm bắt chính xác các trạng thái biến động khác nhau của thị trường.

Nguyên lý chiến lược

Tính toán cốt lõi của chiến lược bao gồm các phần chính sau:

- Tính chỉ báo BBP: Đo lường sức mạnh thị trường thông qua tổng chênh lệch giữa giá cao nhất và EMA (sức mua) và chênh lệch giữa giá thấp nhất và EMA (sức bán).

- Chuẩn hóa Z-Score: Chuẩn hóa giá trị BBP để đánh giá mức độ lệch của cường độ thị trường hiện tại so với trung bình.

- Phân tích khối lượng: Tính tỷ lệ khối lượng hiện tại so với đường trung bình động để đánh giá mức độ sôi động của thị trường.

- Phân tích phân vị: Tính phân vị lịch sử của giá và khối lượng để xác định vị trí phân phối xác suất của trạng thái thị trường.

- Chốt lời động: Điều chỉnh linh hoạt khoảng cách chốt lời dựa trên điểm tổng hợp từ ATR, phân vị khối lượng và phân vị giá.

Ưu điểm của chiến lược

- Phân tích đa chiều: Kết hợp động lượng giá, khối lượng và vị thế thị trường, mang lại góc nhìn toàn diện hơn.

- Khả năng thích ứng cao: Cơ chế chốt lời động giúp thích nghi với các môi trường thị trường khác nhau.

- Phân tán rủi ro: Sử dụng chiến lược chốt lời đa cấp, giải phóng lợi nhuận ở các mức giá khác nhau.

- Lợi thế xác suất: Thông qua Z-Score và phân tích phân vị, có lợi thế thống kê đáng kể.

- Khả năng mở rộng: Khung chiến lược có khả năng mở rộng tốt, có thể bổ sung các chiều phân tích mới khi cần.

Rủi ro của chiến lược

- Nhạy cảm với tham số: Chiến lược bao gồm nhiều tham số, cần tối ưu hóa cho từng môi trường thị trường khác nhau.

- Phụ thuộc vào môi trường thị trường: Có thể hoạt động kém trong giai đoạn biến động mạnh hoặc chuyển đổi xu hướng.

- Trượt giá thực thi: Các lệnh chốt lời đa cấp có thể gặp trượt giá thực thi, ảnh hưởng đến lợi nhuận thực tế.

- Độ phức tạp tính toán: Tính toán đồng thời nhiều chỉ báo có thể gây tải hệ thống nhất định.

- Nguy cơ tín hiệu giả: Trong thị trường đi ngang có thể phát sinh tín hiệu giao dịch sai.

Hướng tối ưu hóa

- Tham số tự động thích ứng: Áp dụng phương pháp học máy để tự động tối ưu hóa tham số.

- Dự báo thị trường: Bổ sung mô-đun phân loại môi trường thị trường, xác định sớm môi trường giao dịch bất lợi.

- Tối ưu hóa cắt lỗ: Đưa vào cơ chế cắt lỗ động, nâng cao độ chính xác của kiểm soát rủi ro.

- Lọc tín hiệu: Thêm bộ lọc cường độ xu hướng để giảm tín hiệu giả.

- Quản lý vị thế: Tối ưu hóa thuật toán phân bổ vị thế, nâng cao hiệu quả sử dụng vốn.

Tổng kết

Chiến lược này kết hợp chỉ báo BBP truyền thống với các phương pháp phân tích định lượng hiện đại, xây dựng một hệ thống giao dịch có nền tảng lý thuyết vững chắc và tính thực tiễn cao. Thông qua cơ chế chốt lời đa cấp và điều chỉnh động, chiến lược cân bằng tốt giữa lợi nhuận và rủi ro. Mặc dù có độ khó nhất định trong tối ưu hóa tham số, nhưng khả năng mở rộng của khung chiến lược mang lại không gian phát triển cho các cải tiến sau này. Trong ứng dụng thực tế, nhà giao dịch nên điều chỉnh phù hợp dựa trên đặc điểm thị trường cụ thể và khẩu vị rủi ro cá nhân.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability. - 1