Tổng quan

Chiến lược này là một hệ thống giao dịch cao cấp dựa trên chỉ báo KDJ, phân tích sâu các mẫu hình giao cắt của đường K, D và J để nắm bắt xu hướng thị trường. Hệ thống tích hợp thuật toán làm mịn BCWSMA tùy chỉnh, nâng cao độ tin cậy của tín hiệu thông qua tính toán tối ưu hóa chỉ báo ngẫu nhiên. Hệ thống áp dụng cơ chế quản lý rủi ro nghiêm ngặt, bao gồm các chức năng cắt lỗ và cắt lỗ trượt, nhằm quản lý vốn hiệu quả.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Sử dụng thuật toán BCWSMA (trung bình động trọng số tùy chỉnh) để tính chỉ báo KDJ, cải thiện độ mượt và ổn định của chỉ báo

- Thông qua tính toán RSV (giá trị ngẫu nhiên chưa chín), chuyển đổi giá thành giá trị trong khoảng 0-100, phản ánh tốt hơn vị trí của giá giữa các mức cao và thấp

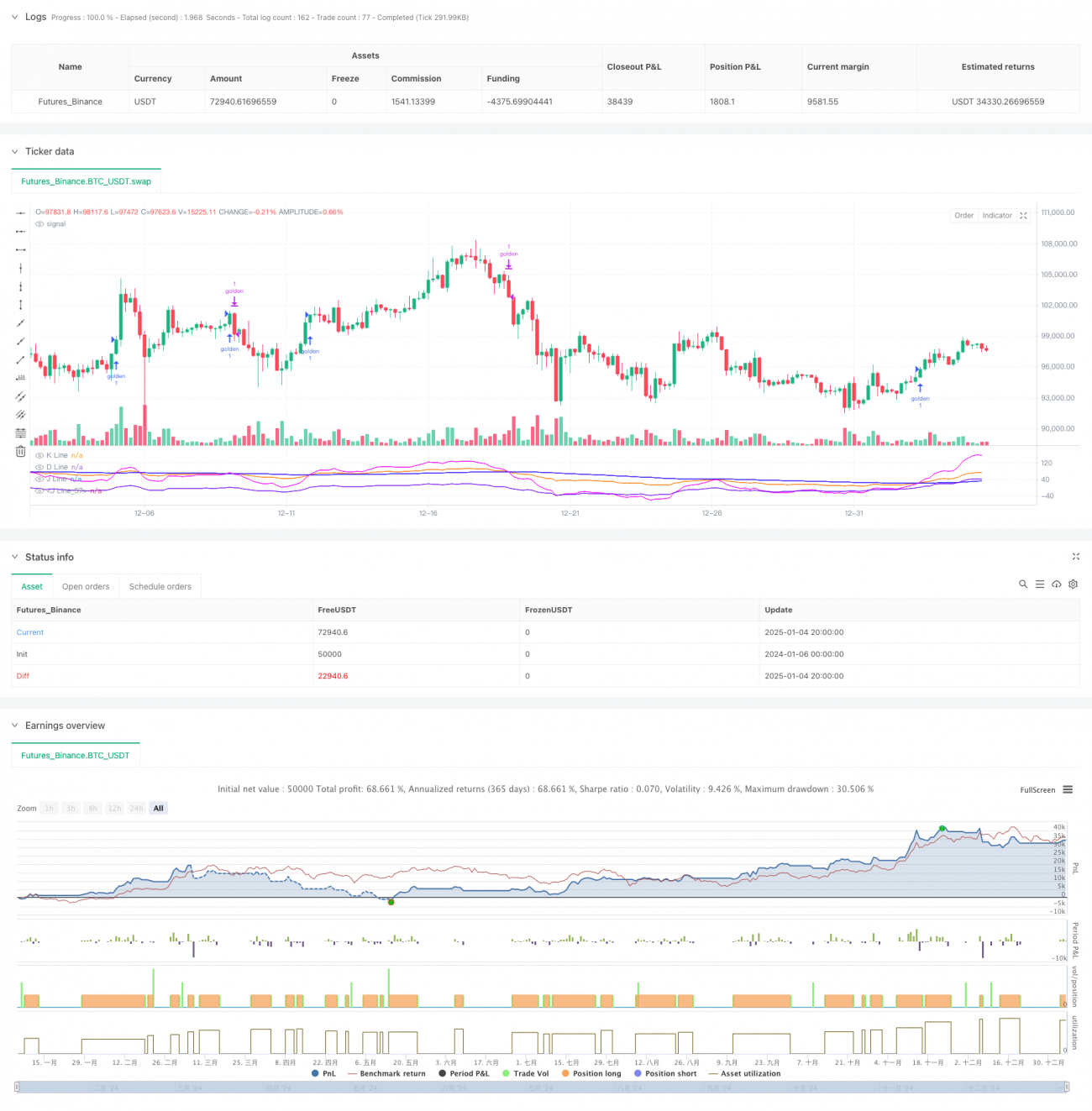

- Thiết kế cơ chế xác nhận chéo giữa đường J và đường J5 (chỉ báo phái sinh), nâng cao độ chính xác của tín hiệu giao dịch thông qua xác nhận nhiều lần

- Xây dựng cơ chế xác nhận xu hướng dựa trên tính liên tục, yêu cầu đường J duy trì trên đường D trong 3 ngày liên tiếp mới xác nhận hiệu lực của xu hướng

- Tích hợp hệ thống kiểm soát rủi ro phức hợp bao gồm cắt lỗ theo tỷ lệ phần trăm và cắt lỗ trượt

Lợi thế của chiến lược

- Cơ chế tạo tín hiệu tiên tiến: thông qua xác nhận chéo nhiều chỉ báo kỹ thuật, giảm đáng kể tác động của tín hiệu sai

- Kiểm soát rủi ro hoàn thiện: sử dụng cơ chế kiểm soát rủi ro đa cấp, bao gồm cắt lỗ cố định và cắt lỗ trượt, kiểm soát hiệu quả rủi ro giảm giá

- Tính linh hoạt của tham số cao: các tham số chính như chu kỳ KDJ, hệ số làm mịn tín hiệu có thể điều chỉnh linh hoạt theo điều kiện thị trường

- Hiệu quả tính toán cao: sử dụng thuật toán BCWSMA tối ưu hóa, giảm độ phức tạp tính toán, nâng cao hiệu suất thực thi chiến lược

- Khả năng thích ứng tốt: có thể thích ứng với các môi trường thị trường khác nhau, tối ưu hóa hiệu suất chiến lược thông qua điều chỉnh tham số

Rủi ro của chiến lược

- Rủi ro thị trường dao động: trong thị trường dao động ngang, có thể phát sinh tín hiệu phá vỡ giả thường xuyên, làm tăng chi phí giao dịch

- Rủi ro độ trễ: do sử dụng xử lý làm mịn đường trung bình, tín hiệu có thể xuất hiện độ trễ nhất định

- Tính nhạy cảm với tham số: hiệu quả chiến lược khá nhạy cảm với cài đặt tham số, cài đặt tham số không phù hợp có thể làm giảm đáng kể hiệu quả chiến lược

- Phụ thuộc vào môi trường thị trường: trong một số môi trường thị trường cụ thể, hiệu suất chiến lược có thể không lý tưởng

Hướng tối ưu hóa chiến lược

- Tối ưu hóa cơ chế lọc tín hiệu: có thể đưa vào các chỉ báo phụ trợ như khối lượng giao dịch, độ biến động, nâng cao độ tin cậy của tín hiệu

- Điều chỉnh tham số động: điều chỉnh động các tham số KDJ và tham số cắt lỗ dựa trên biến động thị trường

- Nhận dạng môi trường thị trường: thêm mô-đun đánh giá môi trường thị trường, áp dụng các chiến lược giao dịch khác nhau trong các môi trường thị trường khác nhau

- Tăng cường kiểm soát rủi ro: có thể thêm các biện pháp kiểm soát rủi ro bổ sung như kiểm soát drawdown tối đa, giới hạn thời gian nắm giữ

- Tối ưu hóa hiệu suất: tối ưu hóa thêm thuật toán BCWSMA, nâng cao hiệu quả tính toán

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh thông qua sự kết hợp sáng tạo của các chỉ báo kỹ thuật và kiểm soát rủi ro nghiêm ngặt. Lợi thế cốt lõi của chiến lược nằm ở cơ chế xác nhận tín hiệu nhiều lần và hệ thống kiểm soát rủi ro hoàn thiện, nhưng cũng cần chú ý đến vấn đề tối ưu hóa tham số và khả năng thích ứng với môi trường thị trường. Thông qua tối ưu hóa và cải tiến liên tục, chiến lược hứa hẹn duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau.

- 1