Chiến lược giao dịch đột phá dao động VWAP động với hai độ lệch chuẩn dựa trên thống kê định lượng

Tổng quan

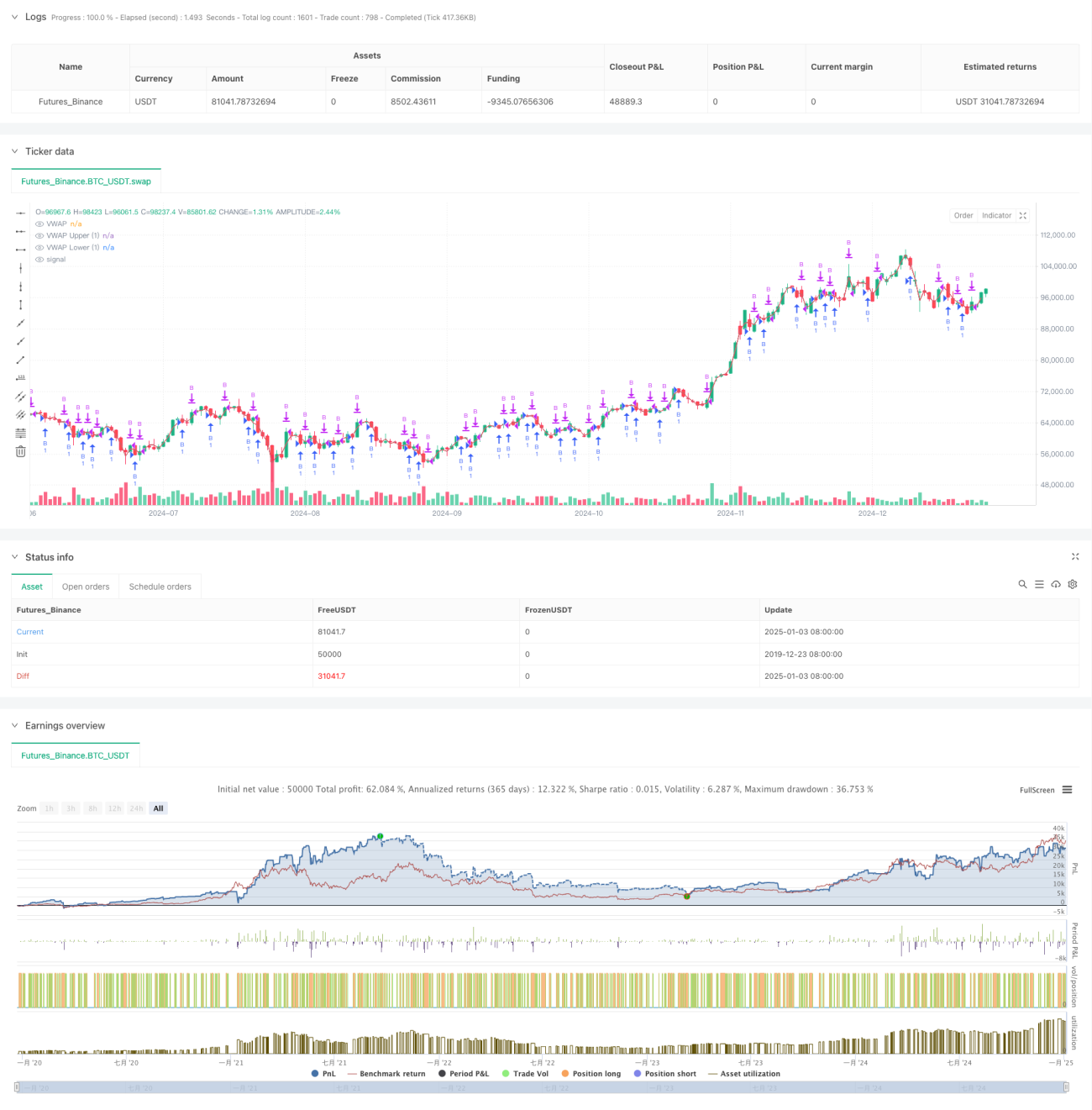

Chiến lược này là một chiến lược đột phá xu hướng dựa trên VWAP (Giá trung bình gia quyền theo khối lượng) và dải độ lệch chuẩn. Bằng cách tính toán VWAP và các dải độ lệch chuẩn trên/dưới, nó xây dựng một khoảng biến động giá động, được sử dụng để nắm bắt cơ hội giao dịch khi giá phá vỡ lên trên. Chiến lược chủ yếu dựa vào tín hiệu phá vỡ từ dải độ lệch chuẩn để thực hiện giao dịch, đồng thời đặt mục tiêu lợi nhuận và khoảng cách giữa các lệnh để kiểm soát rủi ro.

Nguyên lý chiến lược

- Tính toán chỉ báo cốt lõi:

- Sử dụng giá HL2 trong ngày và khối lượng để tính VWAP

- Tính độ lệch chuẩn dựa trên biến động giá

- Thiết lập dải trên/dưới với hệ số 1,28 lần độ lệch chuẩn

- Logic giao dịch:

- Điều kiện vào lệnh: Giá xuyên xuống dưới dải dưới sau đó hồi phục lên trên

- Điều kiện thoát lệnh: Đạt mục tiêu lợi nhuận cài đặt trước

- Đặt khoảng cách tối thiểu giữa các lệnh để tránh giao dịch quá thường xuyên

Ưu điểm chiến lược

- Cơ sở thống kê

- Tham chiếu trung tâm giá dựa trên VWAP

- Sử dụng độ lệch chuẩn để đo lường biến động

- Điều chỉnh khoảng giao dịch động

- Kiểm soát rủi ro

- Đặt mục tiêu lợi nhuận cố định

- Kiểm soát tần suất giao dịch

- Chỉ giao dịch long giúp giảm rủi ro

Rủi ro chiến lược

- Rủi ro thị trường

- Biến động mạnh có thể dẫn đến phá vỡ giả

- Khó nắm bắt chính xác điểm đảo chiều xu hướng

- Tổn thất gia tăng trong thị trường giảm một chiều

- Rủi ro tham số

- Cài đặt hệ số độ lệch chuẩn nhạy cảm

- Mục tiêu lợi nhuận cần được tối ưu hóa

- Khoảng cách giữa các lệnh ảnh hưởng đến hiệu suất lợi nhuận

Hướng tối ưu hóa

- Tối ưu tín hiệu

- Thêm bộ lọc xác định xu hướng

- Kết hợp xác nhận biến động khối lượng

- Bổ sung xác thực từ các chỉ báo kỹ thuật khác

- Tối ưu quản lý rủi ro

- Đặt điểm dừng lỗ động

- Điều chỉnh khối lượng vị thế theo biến động

- Hoàn thiện cơ chế quản lý lệnh

Kết luận

Đây là một chiến lược giao dịch định lượng kết hợp nguyên lý thống kê và phân tích kỹ thuật. Thông qua sự phối hợp giữa VWAP và dải độ lệch chuẩn, một hệ thống giao dịch tương đối đáng tin cậy đã được xây dựng. Ưu điểm cốt lõi của chiến lược nằm ở nền tảng thống kê khoa học và cơ chế kiểm soát rủi ro hoàn chỉnh, nhưng vẫn cần liên tục tối ưu hóa tham số và logic giao dịch trong ứng dụng thực tế.

- 1