Chiến lược giao dịch Kim tự tháp động Siêu xu hướng Đa chu kỳ

Tổng quan

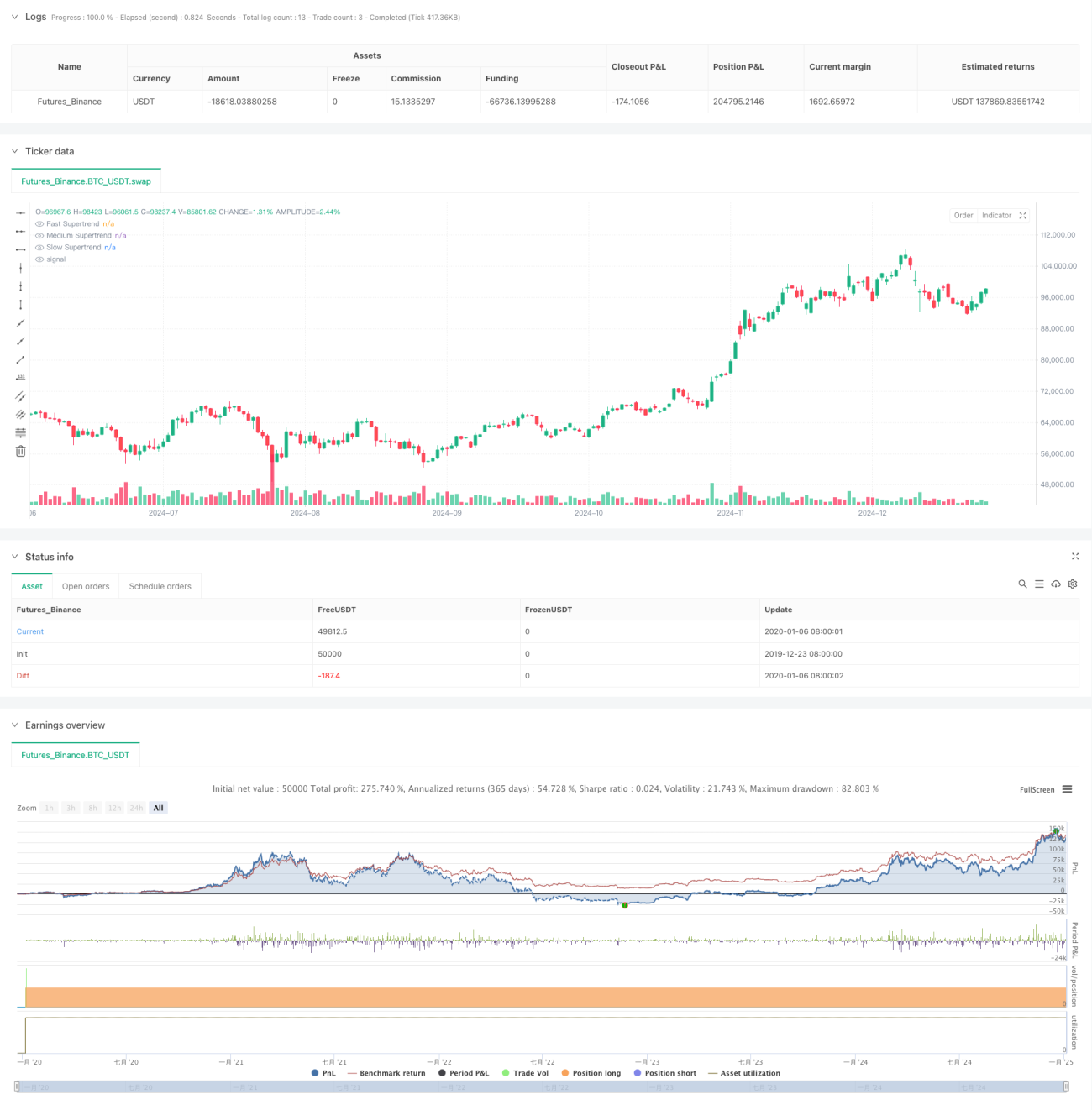

Đây là chiến lược giao dịch kim tự tháp dựa trên chỉ báo Supertrend nhiều lớp. Nó sử dụng ba chỉ báo Supertrend với chu kỳ và hệ số nhân khác nhau để xác định các cơ hội giao dịch xác suất cao. Chiến lược áp dụng phương pháp thêm vị thế kim tự tháp động, cho phép tối đa ba lần vào lệnh, kết hợp với stop loss động và điều kiện thoát linh hoạt để tối đa hóa lợi nhuận và kiểm soát rủi ro.

Nguyên lý chiến lược

Chiến lược sử dụng ba chỉ báo Supertrend với các tham số khác nhau: nhanh, trung bình và chậm. Tín hiệu vào lệnh dựa trên sự giao nhau và hướng xu hướng của ba chỉ báo này, áp dụng kiểu thêm vị thế ba lớp: Lớp thứ nhất vào lệnh khi chỉ báo nhanh hướng xuống, chỉ báo trung bình hướng lên và chỉ báo chậm hướng xuống; Lớp thứ hai vào lệnh theo kiểu phá vỡ khi cả chỉ báo nhanh và trung bình cùng hướng xuống; Lớp thứ ba vào lệnh theo kiểu phá vỡ khi thị trường tạo đỉnh mới. Thoát lệnh sử dụng nhiều cơ chế như stop loss động, stop loss trung bình giá và đảo chiều xu hướng tổng thể.

Ưu điểm của chiến lược

- Cơ chế xác nhận nhiều lớp giúp tăng độ chính xác của giao dịch.

- Cách thêm vị thế kim tự tháp có thể khuếch đại đáng kể lợi nhuận trong xu hướng.

- Cơ chế stop loss động vừa bảo vệ lợi nhuận vừa cho phép xu hướng phát triển đầy đủ.

- Cơ chế thoát linh hoạt giúp ứng phó tốt với các điều kiện thị trường khác nhau.

- Sử dụng kiểm soát tỷ lệ phần trăm vốn, phù hợp với quy mô vốn khác nhau.

Rủi ro của chiến lược

- Trong thị trường dao động (sideway) có thể tạo ra nhiều tín hiệu giả.

- Thêm vị thế kim tự tháp có thể gây ra drawdown lớn khi xu hướng đảo chiều đột ngột.

- Nhiều chỉ báo có thể dẫn đến độ trễ tín hiệu.

- Tối ưu hóa tham số có nguy cơ overfitting.

Khuyến nghị áp dụng quản lý vốn chặt chẽ và kiểm tra backtest để kiểm soát các rủi ro này.

Hướng tối ưu hóa chiến lược

- Thêm cơ chế lọc môi trường thị trường, điều chỉnh tham số động theo các điều kiện biến động khác nhau.

- Tối ưu hóa khoảng cách thêm vị thế và tỷ lệ phân bổ vị thế.

- Đưa thêm các chỉ báo kỹ thuật khác để lọc tín hiệu giả.

- Phát triển cơ chế tham số thích ứng để thích ứng với sự thay đổi của thị trường.

- Hoàn thiện cơ chế thoát lệnh, có thể xem xét thêm mục tiêu lợi nhuận và stop loss theo thời gian.

Tổng kết

Chiến lược này nắm bắt cơ hội xu hướng thông qua chỉ báo Supertrend nhiều lớp và phương pháp thêm vị thế kim tự tháp, kết hợp với stop loss động và cơ chế thoát linh hoạt để kiểm soát rủi ro. Mặc dù có một số hạn chế nhất định, nhưng thông qua tối ưu hóa liên tục và kiểm soát rủi ro nghiêm ngặt, chiến lược này có giá trị ứng dụng thực tế tốt.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('4Vietnamese 3x Supertrend', overlay=true, max_bars_back=1000, initial_capital = 10000000000, slippage = 2, commission_type = strategy.commission.percent, commission_value = 0.013, default_qty_type=strategy.percent_of_equity, default_qty_value = 33.33, pyramiding = 3, margin_long = 0, margin_short = 0)

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////- 1