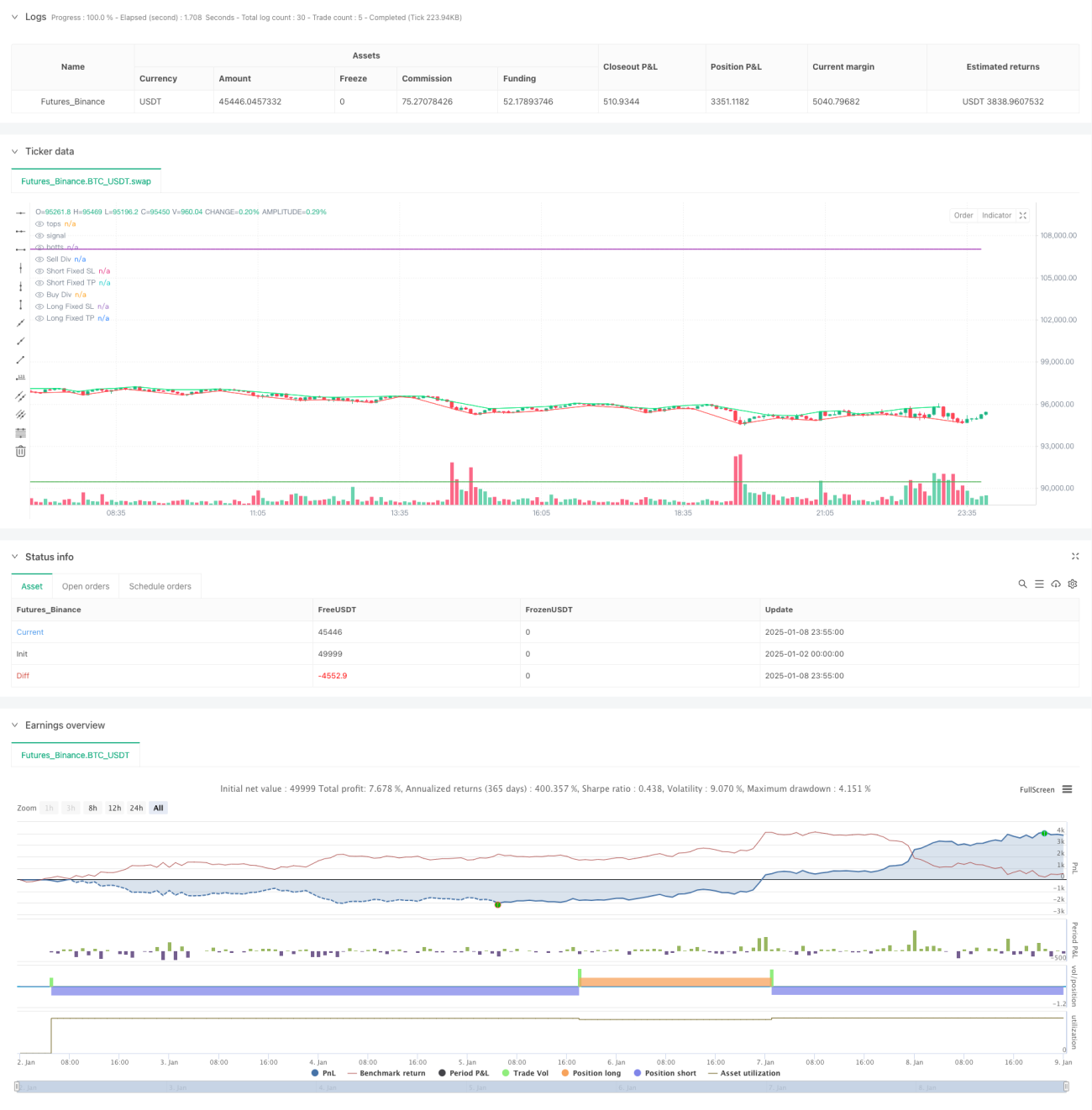

Hệ thống giám sát động chỉ báo và tối ưu hóa thích ứng cho chiến lược định lượng phân kỳ giá RSI

Tổng quan

Chiến lược này là một hệ thống giao dịch thông minh dựa trên RSI và sự phân kỳ giá, thông qua việc theo dõi động thái mối quan hệ phân kỳ giữa chỉ báo RSI và xu hướng giá để bắt tín hiệu đảo chiều thị trường. Chiến lược tích hợp lý thuyết Fractals làm xác nhận hỗ trợ, đồng thời được trang bị cơ chế chốt lời cắt lỗ thích ứng, giúp thực hiện giao dịch hoàn toàn tự động. Hệ thống hỗ trợ ứng dụng đa sản phẩm, đa khung thời gian, có tính linh hoạt và thực tiễn cao.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Nhận diện phân kỳ RSI: Bằng cách so sánh chỉ báo RSI và các điểm cao/thấp của xu hướng giá, nhận diện các mô hình phân kỳ tiềm năng. Khi giá tạo đỉnh cao hơn nhưng RSI không tạo đỉnh cao hơn, hình thành tín hiệu bán phân kỳ đỉnh; khi giá tạo đáy thấp hơn nhưng RSI không tạo đáy thấp hơn, hình thành tín hiệu mua phân kỳ đáy.

- Xác nhận Fractals: Sử dụng lý thuyết Fractals để phân tích cấu trúc giá, thông qua việc phát hiện các điểm cao/thấp cục bộ nhằm xác nhận tính hiệu quả của phân kỳ, tăng độ tin cậy của tín hiệu.

- Thích ứng tham số: Hệ thống đưa vào tham số Độ nhạy (Sensitivity) để điều chỉnh động khoảng xác định Fractals, đạt được khả năng thích ứng với các môi trường thị trường khác nhau.

- Kiểm soát rủi ro: Tích hợp cơ chế cắt lỗ (Stop Loss) và chốt lời (Take Profit) dựa trên tỷ lệ phần trăm, đảm bảo rủi ro mỗi giao dịch được kiểm soát.

Ưu điểm chiến lược

- Độ tin cậy tín hiệu cao: Thông qua cơ chế xác nhận kép giữa phân kỳ RSI và lý thuyết Fractals, độ chính xác của tín hiệu giao dịch được cải thiện đáng kể.

- Khả năng thích ứng mạnh: Chiến lược có thể linh hoạt điều chỉnh tham số theo các điều kiện thị trường khác nhau, có khả năng thích ứng với môi trường tốt.

- Quản lý rủi ro hoàn thiện: Tích hợp cơ chế chốt lời cắt lỗ động, có thể kiểm soát hiệu quả mức độ rủi ro của mỗi giao dịch.

- Mức độ tự động hóa cao: Từ nhận diện tín hiệu đến thực hiện giao dịch đều tự động hóa hoàn toàn, giảm thiểu ảnh hưởng cảm xúc do can thiệp thủ công.

- Khả năng mở rộng tốt: Khung chiến lược hỗ trợ ứng dụng đa sản phẩm, đa khung thời gian, thuận tiện cho việc đầu tư kết hợp.

Rủi ro chiến lược

- Phụ thuộc vào môi trường thị trường: Trong thị trường có xu hướng rõ ràng, độ tin cậy của tín hiệu phân kỳ có thể giảm, cần thêm cơ chế lọc xu hướng.

- Nhạy cảm với tham số: Các tham số chính của chiến lược như ngưỡng RSI, khoảng xác định Fractals cần được tinh chỉnh cẩn thận; cài đặt tham số không phù hợp có thể ảnh hưởng đến hiệu suất chiến lược.

- Độ trễ tín hiệu: Do cần chờ mô hình phân kỳ hình thành hoàn chỉnh mới xác nhận tín hiệu, có thể có độ trễ nhất định về thời điểm vào lệnh.

- Nhiễu thị trường: Trong thị trường biến động mạnh, có thể phát sinh tín hiệu phân kỳ giả, cần thêm điều kiện lọc.

Hướng tối ưu hóa chiến lược

- Thêm bộ lọc xu hướng: Đưa vào chỉ báo xác định xu hướng, lọc các tín hiệu ngược chiều trong thị trường xu hướng mạnh, nâng cao khả năng thích ứng của chiến lược trong các môi trường thị trường khác nhau.

- Tối ưu hóa thích ứng tham số: Phát triển cơ chế điều chỉnh tham số động dựa trên biến động thị trường, nâng cao khả năng phản ứng của chiến lược với sự thay đổi của thị trường.

- Hoàn thiện kiểm soát rủi ro: Đưa vào cơ chế cắt lỗ động, tự động điều chỉnh vị trí cắt lỗ theo biến động thị trường, tối ưu hóa hiệu quả quản lý vốn.

- Tăng cường xác nhận tín hiệu: Kết hợp các chỉ báo vi cấu trúc thị trường như khối lượng giao dịch, biến động, thiết lập hệ thống xác nhận tín hiệu hoàn thiện hơn.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch vững chắc thông qua sự kết hợp sáng tạo giữa phân kỳ RSI và lý thuyết Fractals. Ưu điểm của chiến lược nằm ở độ tin cậy tín hiệu cao, khả năng thích ứng mạnh, đồng thời có cơ chế kiểm soát rủi ro hoàn thiện. Thông qua việc tối ưu hóa và cải tiến liên tục, chiến lược có tiềm năng duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau. Khuyến nghị khi ứng dụng thực tế, cần kết hợp đặc điểm thị trường để kiểm tra và tối ưu hóa tham số đầy đủ, đồng thời thực hiện nghiêm ngặt các biện pháp kiểm soát rủi ro.

- 1