Chiến lược tối ưu hóa ba lớp SuperTrend với theo dõi xu hướng động và hỗ trợ đường trung bình

Tổng quan

Đây là một chiến lược giao dịch theo xu hướng dựa trên chỉ báo SuperTrend, đường trung bình động hàm mũ (EMA) và Average True Range (ATR). Chiến lược này kết hợp nhiều chỉ báo kỹ thuật, cùng với cơ chế cắt lỗ ban đầu và cắt lỗ động, nhằm theo dõi xu hướng thị trường một cách linh hoạt và kiểm soát rủi ro. Cốt lõi của chiến lược nằm ở việc sử dụng chỉ báo SuperTrend để phát hiện sự thay đổi hướng đi của xu hướng, đồng thời sử dụng EMA để xác nhận xu hướng, đồng thời thiết lập cơ chế cắt lỗ kép để bảo vệ lợi nhuận.

Nguyên lý chiến lược

Chiến lược hoạt động dựa trên các thành phần cốt lõi sau:

- Chỉ báo SuperTrend được sử dụng để xác định sự thay đổi hướng đi của xu hướng, chỉ báo này được tính toán dựa trên chu kỳ ATR là 16 và hệ số 3,02.

- EMA chu kỳ 49 đóng vai trò như một bộ lọc xu hướng, dùng để xác nhận hướng đi của xu hướng.

- Mức cắt lỗ ban đầu được thiết lập ở mức 50 điểm, cung cấp sự bảo vệ cơ bản cho mỗi giao dịch.

- Cắt lỗ động được kích hoạt sau khi lợi nhuận đạt 70 điểm, theo dõi động biến động giá.

Khi hướng của SuperTrend chuyển xuống và giá đóng cửa nằm trên đường EMA, hệ thống sẽ phát tín hiệu mua nếu chưa có vị thế nào. Ngược lại, khi hướng của SuperTrend chuyển lên và giá đóng cửa nằm dưới đường EMA, hệ thống sẽ phát tín hiệu bán.

Lợi thế của chiến lược

- Cơ chế xác nhận nhiều lớp: Bằng cách kết hợp SuperTrend và EMA, giảm thiểu tác động của các tín hiệu nhiễu.

- Kiểm soát rủi ro hoàn chỉnh: Sử dụng cơ chế cắt lỗ kép, vừa có cắt lỗ cố định bảo vệ vừa có cắt lỗ động theo dõi.

- Quản lý vị thế linh hoạt: Chiến lược mặc định sử dụng 15% giá trị tài khoản ròng làm tỷ lệ nắm giữ, có thể điều chỉnh theo nhu cầu.

- Khả năng thích ứng xu hướng cao: Có thể tự điều chỉnh trong các môi trường thị trường khác nhau, đặc biệt phù hợp với các thị trường biến động mạnh.

- Khả năng tối ưu hóa tham số: Các tham số chính đều có thể được tối ưu hóa và điều chỉnh dựa trên đặc điểm của từng thị trường.

Rủi ro của chiến lược

- Rủi ro thị trường đi ngang: Trong thị trường dao động ngang, có thể giao dịch thường xuyên, dẫn đến cắt lỗ liên tiếp.

- Rủi ro trượt giá: Trong các đợt giá biến động nhanh, giá thực hiện cắt lỗ có thể chênh lệch đáng kể so với kỳ vọng.

- Nhạy cảm với tham số: Hiệu quả của chiến lược khá nhạy với cài đặt tham số, các môi trường thị trường khác nhau có thể yêu cầu điều chỉnh tham số.

- Rủi ro đảo chiều xu hướng: Tại các điểm đảo chiều xu hướng, có thể xảy ra khoản lỗ lớn trước khi kích hoạt cắt lỗ.

- Rủi ro quản lý vốn: Tỷ lệ vị thế cố định có thể mang lại rủi ro lớn trong các biến động mạnh.

Hướng tối ưu hóa chiến lược

- Điều chỉnh tham số động: Có thể tự động điều chỉnh các tham số của SuperTrend và EMA dựa trên mức biến động của thị trường.

- Lọc môi trường thị trường: Thêm cơ chế đánh giá môi trường thị trường, dừng giao dịch trong các môi trường không phù hợp.

- Tối ưu hóa cắt lỗ: Có thể đưa vào cài đặt cắt lỗ động dựa trên ATR, giúp cắt lỗ thích ứng hơn với biến động thị trường.

- Tối ưu hóa quản lý vị thế: Phát triển hệ thống quản lý vị thế động dựa trên biến động.

- Thêm mục tiêu lợi nhuận: Thiết lập mục tiêu lợi nhuận động dựa trên biến động thị trường.

Tổng kết

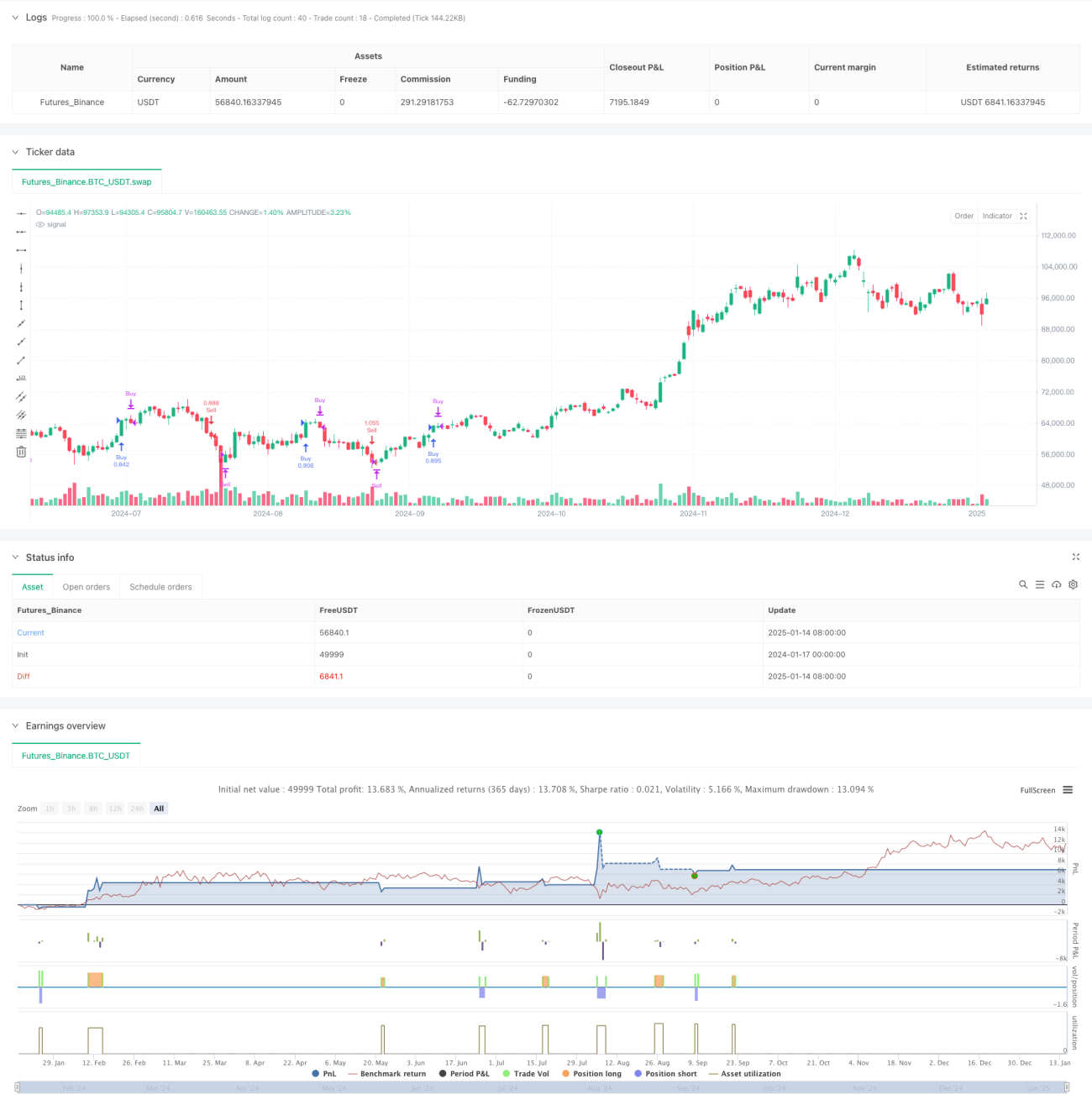

Đây là một chiến lược giao dịch hoàn chỉnh kết hợp nhiều chỉ báo kỹ thuật và cơ chế kiểm soát rủi ro. Bằng cách sử dụng SuperTrend để bắt xu hướng, EMA để xác nhận hướng, kết hợp với cơ chế cắt lỗ kép, chiến lược đạt được tỷ lệ rủi ro-lợi nhuận tốt. Không gian tối ưu hóa chính nằm ở việc điều chỉnh tham số động, đánh giá môi trường thị trường và hoàn thiện hệ thống quản lý rủi ro. Trong ứng dụng thực tế, nên thực hiện backtest đầy đủ trên dữ liệu lịch sử, và điều chỉnh tham số dựa trên đặc điểm của từng sản phẩm giao dịch.

/*backtest

start: 2024-01-17 00:00:00

end: 2025-01-15 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=5

strategy(" nifty supertrend triton", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parameters- 1