Chiến lược theo dõi xu hướng nhiều đường trung bình động với bộ lọc biến động động

Tổng quan

Chiến lược này là một hệ thống giao dịch thông minh kết hợp theo dõi xu hướng và bộ lọc biến động. Nó sử dụng đường trung bình động hàm mũ (EMA) để xác định xu hướng thị trường, sử dụng Phạm vi biến động thực (TR) và bộ lọc biến động động để xác định thời điểm vào lệnh, đồng thời sử dụng cơ chế chốt lời cắt lỗ động dựa trên biến động để quản lý rủi ro. Chiến lược hỗ trợ hai chế độ giao dịch: Scalp (Lướt sóng ngắn) và Swing (Giao dịch sóng), có thể linh hoạt chuyển đổi tùy theo môi trường thị trường và phong cách giao dịch khác nhau.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm các thành phần chính sau:

- Xác định xu hướng: Sử dụng EMA chu kỳ 50 làm bộ lọc xu hướng, chỉ mua khi giá nằm trên EMA và chỉ bán khi giá nằm dưới EMA.

- Bộ lọc biến động: Tính toán EMA của Phạm vi biến động thực (TR) và sử dụng hệ số lọc có thể điều chỉnh (mặc định 1.5) để lọc nhiễu thị trường.

- Điều kiện vào lệnh: Kết hợp phân tích hình thái của 3 nến liên tiếp, yêu cầu biến động giá phải có tính liên tục và tăng tốc.

- Chốt lời cắt lỗ: Trong chế độ Scalp, dựa trên TR hiện tại; trong chế độ Swing, dựa trên đỉnh/đáy trước đó, thực hiện quản lý rủi ro động.

Lợi thế của chiến lược

- Khả năng thích ứng cao: Kết hợp bộ lọc biến động động và theo dõi xu hướng, có thể thích ứng với các môi trường thị trường khác nhau.

- Quản lý rủi ro hoàn chỉnh: Cung cấp cơ chế chốt lời cắt lỗ động cho hai chế độ giao dịch, có thể linh hoạt lựa chọn dựa trên đặc điểm thị trường.

- Tính điều chỉnh tham số tốt: Các tham số chính như hệ số lọc, chu kỳ xu hướng có thể được tối ưu hóa dựa trên đặc điểm của sản phẩm giao dịch.

- Hiệu ứng trực quan tốt: Cung cấp tín hiệu mua bán rõ ràng và hiển thị mức chốt lời cắt lỗ, thuận tiện cho việc giám sát giao dịch.

Rủi ro của chiến lược

- Rủi ro đảo chiều xu hướng: Có thể xảy ra các lệnh cắt lỗ liên tiếp tại các điểm đảo chiều xu hướng.

- Rủi ro phá vỡ giả: Khi biến động tăng đột biến có thể kích hoạt tín hiệu giả.

- Nhạy cảm với tham số: Thiết lập hệ số lọc không phù hợp có thể dẫn đến quá nhiều hoặc quá ít tín hiệu.

- Ảnh hưởng của trượt giá: Trong thị trường nhanh có thể phải đối mặt với trượt giá lớn, ảnh hưởng đến hiệu suất chiến lược.

Hướng tối ưu hóa chiến lược

- Bổ sung bộ lọc cường độ xu hướng: Có thể giới thiệu các chỉ số như ADX để đánh giá cường độ xu hướng, cải thiện hiệu quả theo dõi xu hướng.

- Tối ưu hóa chốt lời cắt lỗ: Có thể xem xét giới thiệu cắt lỗ động (trailing stop) để bảo vệ nhiều lợi nhuận hơn.

- Hoàn thiện chế độ Swing: Có thể thêm nhiều điều kiện phán đoán đặc thù của giao dịch sóng, nâng cao khả năng nắm giữ trung và dài hạn.

- Bổ sung phân tích khối lượng: Kết hợp thay đổi khối lượng giao dịch để xác nhận tính hiệu quả của sự phá vỡ.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách kết hợp hữu cơ theo dõi xu hướng, bộ lọc biến động và quản lý rủi ro động. Ưu điểm của chiến lược nằm ở khả năng thích ứng cao, rủi ro có thể kiểm soát, đồng thời cung cấp không gian tối ưu hóa lớn. Bằng cách thiết lập tham số hợp lý và lựa chọn chế độ giao dịch phù hợp, chiến lược này có thể duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau. Khuyến nghị nhà giao dịch nên tiến hành backtest và tối ưu hóa tham số đầy đủ trước khi sử dụng thực tế, đồng thời điều chỉnh tương ứng dựa trên đặc điểm của sản phẩm giao dịch cụ thể.

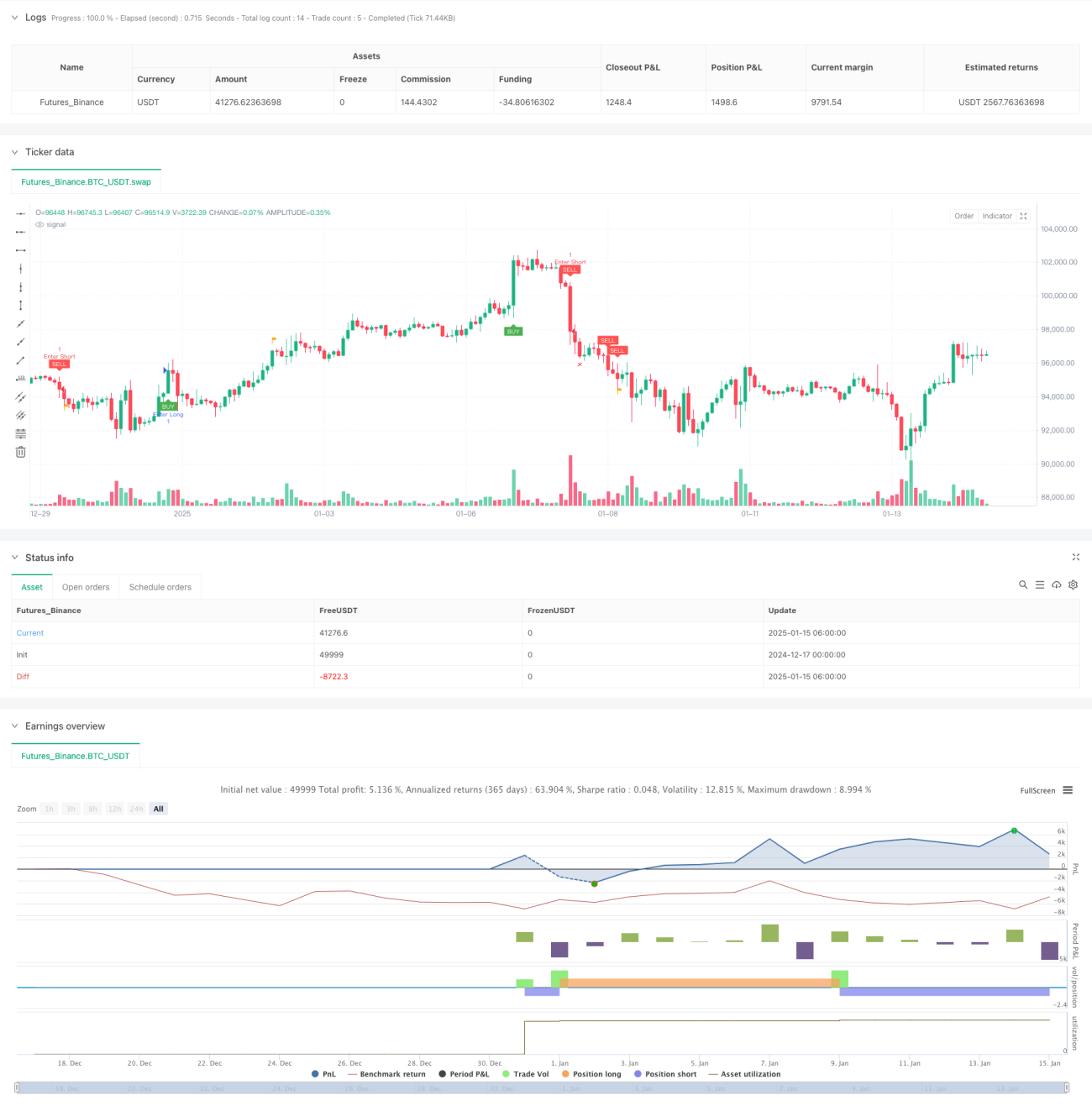

/*backtest

start: 2024-12-17 00:00:00

end: 2025-01-15 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Creativ3mindz

//@version=5- 1