Tổng quan

Chiến lược này là một hệ thống giao dịch tổng hợp dựa trên Kênh Keltner (Keltner Channel) và các mức hỗ trợ/kháng cự động. Bằng cách phân tích nhiều khung thời gian, kết hợp với chỉ báo đường trung bình động và chỉ báo biến động, nó hình thành một khuôn khổ ra quyết định giao dịch hoàn chỉnh. Cốt lõi của chiến lược là xác định thời điểm giá phá vỡ các mức kỹ thuật quan trọng, đồng thời xem xét xu hướng thị trường và mức độ biến động, từ đó nắm bắt các cơ hội giao dịch có xác suất cao.

Nguyên lý chiến lược

Chiến lược sử dụng hệ thống chỉ báo kỹ thuật đa lớp để phân tích:

- Sử dụng Kênh Keltner chu kỳ 21 làm công cụ xác định xu hướng chính, độ rộng kênh được xác định bởi giá trị ATR.

- Tính toán các mức hỗ trợ/kháng cự chính dựa trên 21 nến bên trái và 8 nến bên phải.

- Đưa vào đường trung bình động của khung thời gian cao hơn làm bộ lọc xu hướng.

- Kết hợp đường trung bình động ngắn hạn (chu kỳ 5) và dài hạn (chu kỳ 30) để xác định thời điểm vào lệnh.

- Sử dụng ATR để điều chỉnh vị trí cắt lỗ một cách linh hoạt.

Ưu điểm của chiến lược

- Các chỉ báo kỹ thuật đa chiều xác nhận lẫn nhau, giảm hiệu quả các tín hiệu nhiễu.

- Các mức hỗ trợ/kháng cự động được cập nhật theo thời gian thực, thích ứng với biến động thị trường.

- Phân tích khung thời gian cao hơn giúp lọc bỏ các biến động phụ.

- Tham số cắt lỗ được điều chỉnh linh hoạt theo các khung thời gian khác nhau.

- Áp dụng quản lý vị thế theo tỷ lệ phần trăm, kiểm soát rủi ro hiệu quả.

Rủi ro của chiến lược

- Trong thị trường đi ngang có thể phát sinh tín hiệu giao dịch thường xuyên.

- Việc xác nhận bằng nhiều chỉ báo có thể khiến bỏ lỡ một số cơ hội giao dịch.

- Việc tối ưu hóa tham số có nguy cơ quá khớp (overfitting).

- Trong môi trường biến động cao, vị trí cắt lỗ có thể quá rộng.

- Khi thị trường biến động mạnh, các mức hỗ trợ/kháng cự có thể mất hiệu lực.

Hướng tối ưu hóa chiến lược

- Đưa chỉ báo khối lượng giao dịch vào để hỗ trợ đánh giá độ tin cậy của các phá vỡ.

- Bổ sung mô-đun phân tích biến động thị trường, điều chỉnh tham số động.

- Tối ưu hóa phương pháp tính toán các mức hỗ trợ/kháng cự, nâng cao độ chính xác.

- Thêm đánh giá cường độ xu hướng, làm rõ điều kiện vào lệnh.

- Hoàn thiện hệ thống quản lý vị thế, đạt được kiểm soát rủi ro tinh tế hơn.

Tổng kết

Đây là một chiến lược giao dịch định lượng có cấu trúc hoàn chỉnh và logic chặt chẽ. Nhờ sự phối hợp của các chỉ báo kỹ thuật đa lớp, chiến lược vừa đảm bảo độ tin cậy của tín hiệu giao dịch, vừa đạt được khả năng kiểm soát rủi ro hiệu quả. Khả năng mở rộng của chiến lược cao, thông qua tối ưu hóa và cải tiến liên tục, nó có thể duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau.

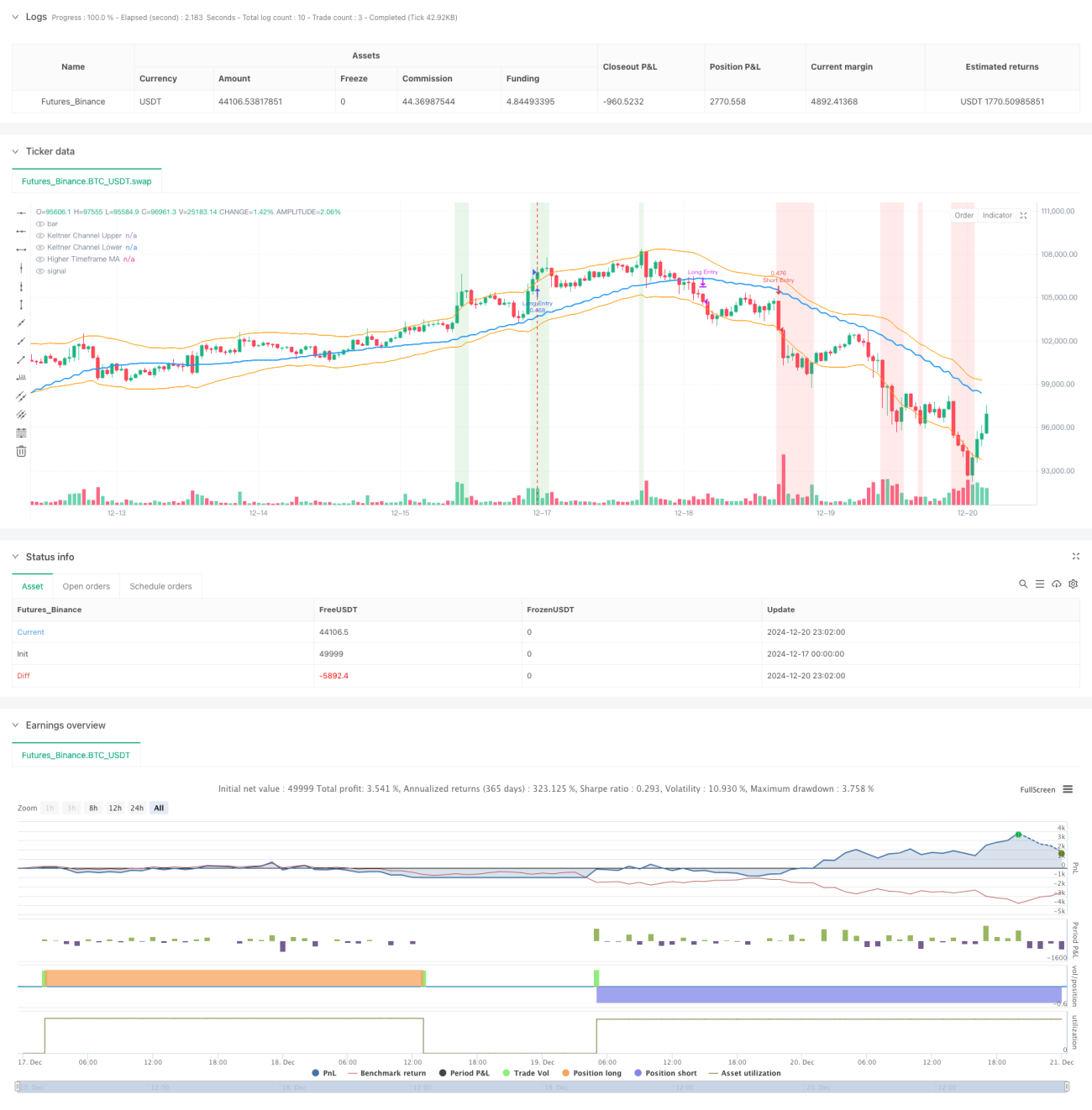

/*backtest

start: 2024-12-17 00:00:00

end: 2024-12-21 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © sathcm

//@version=5

strategy("KMS", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.05, slippage=3)- 1