Chiến lược đa chu kỳ kênh Gaussian thích ứng động lượng

Tổng quan

Chiến lược này là một hệ thống giao dịch động lượng dựa trên kênh Gaussian và chỉ báo Stochastic RSI, kết hợp bộ lọc theo mùa và quản lý biến động. Chiến lược sử dụng kênh Gaussian thích ứng để xác định xu hướng thị trường, Stochastic RSI để xác nhận động lượng, và thực hiện giao dịch trong các cửa sổ theo mùa cụ thể. Hệ thống cũng tích hợp quản lý vị thế dựa trên ATR để kiểm soát rủi ro cho mỗi giao dịch.

Nguyên lý chiến lược

Cốt lõi của chiến lược là một kênh giá được xây dựng dựa trên bộ lọc Gaussian đa cực. Kênh này tính toán giá trị lọc Gaussian của giá HLC3, kết hợp với kết quả lọc của Phạm vi biến động thực (TR), tạo thành các dải trên và dưới động. Tín hiệu giao dịch được phát sinh khi đáp ứng các điều kiện sau:

- Giá phá vỡ dải trên và xu hướng chính của bộ lọc đang đi lên

- Chỉ báo Stochastic RSI cho thấy trạng thái quá mua

- Thời gian hiện tại nằm trong cửa sổ theo mùa đã định trước

- Quy mô vị thế được tính toán động dựa trên ATR

Tín hiệu đóng vị thế được kích hoạt khi giá phá vỡ dải dưới. Toàn bộ hệ thống thông qua cơ chế lọc nhiều lớp, giúp tăng tính ổn định của giao dịch.

Lợi thế của chiến lược

- Bộ lọc Gaussian có khả năng lọc nhiễu tuyệt vời, có thể nắm bắt hiệu quả xu hướng thị trường thực sự

- Thiết kế đa cực cung cấp ranh giới kênh giá chính xác hơn

- Tích hợp các chỉ báo động lượng và xu hướng, tăng độ tin cậy của tín hiệu

- Bộ lọc theo mùa giúp tránh các môi trường thị trường bất lợi

- Quản lý vị thế động đảm bảo tính nhất quán của rủi ro

- Các tham số hệ thống có thể được tối ưu hóa theo các điều kiện thị trường khác nhau

Rủi ro của chiến lược

- Tính toán bộ lọc Gaussian phức tạp, có thể gây ra độ trễ thực thi

- Nhiều điều kiện lọc có thể bỏ lỡ một số cơ hội giao dịch quan trọng

- Hệ thống khá nhạy với cài đặt tham số, cần tối ưu hóa cẩn thận

- Cài đặt cửa sổ theo mùa cố định có thể không thích ứng với sự thay đổi của môi trường thị trường

- Trong thời kỳ biến động cao, kiểm soát vị thế dựa trên ATR có thể quá thận trọng

Hướng tối ưu hóa chiến lược

- Giới thiệu cửa sổ theo mùa thích ứng, điều chỉnh thời gian giao dịch động theo điều kiện thị trường

- Tối ưu hóa hiệu suất tính toán của bộ lọc Gaussian, giảm độ trễ thực thi

- Bổ sung cơ chế điều chỉnh biến động thị trường, điều chỉnh điều kiện lọc trong các môi trường thị trường khác nhau

- Phát triển hệ thống quản lý vị thế linh hoạt hơn, cân bằng rủi ro và lợi nhuận

- Tăng cường phân tích đa khung thời gian, nâng cao độ tin cậy của tín hiệu

Tổng kết

Đây là một hệ thống giao dịch theo xu hướng được xây dựng hoàn chỉnh, thông qua cơ chế lọc nhiều lớp và quản lý rủi ro giúp tăng tính ổn định của giao dịch. Mặc dù còn một số không gian tối ưu, nhưng thiết kế tổng thể phù hợp với yêu cầu của giao dịch định lượng hiện đại. Chìa khóa thành công của chiến lược nằm ở việc điều chỉnh chính xác các tham số và khả năng thích ứng với môi trường thị trường.

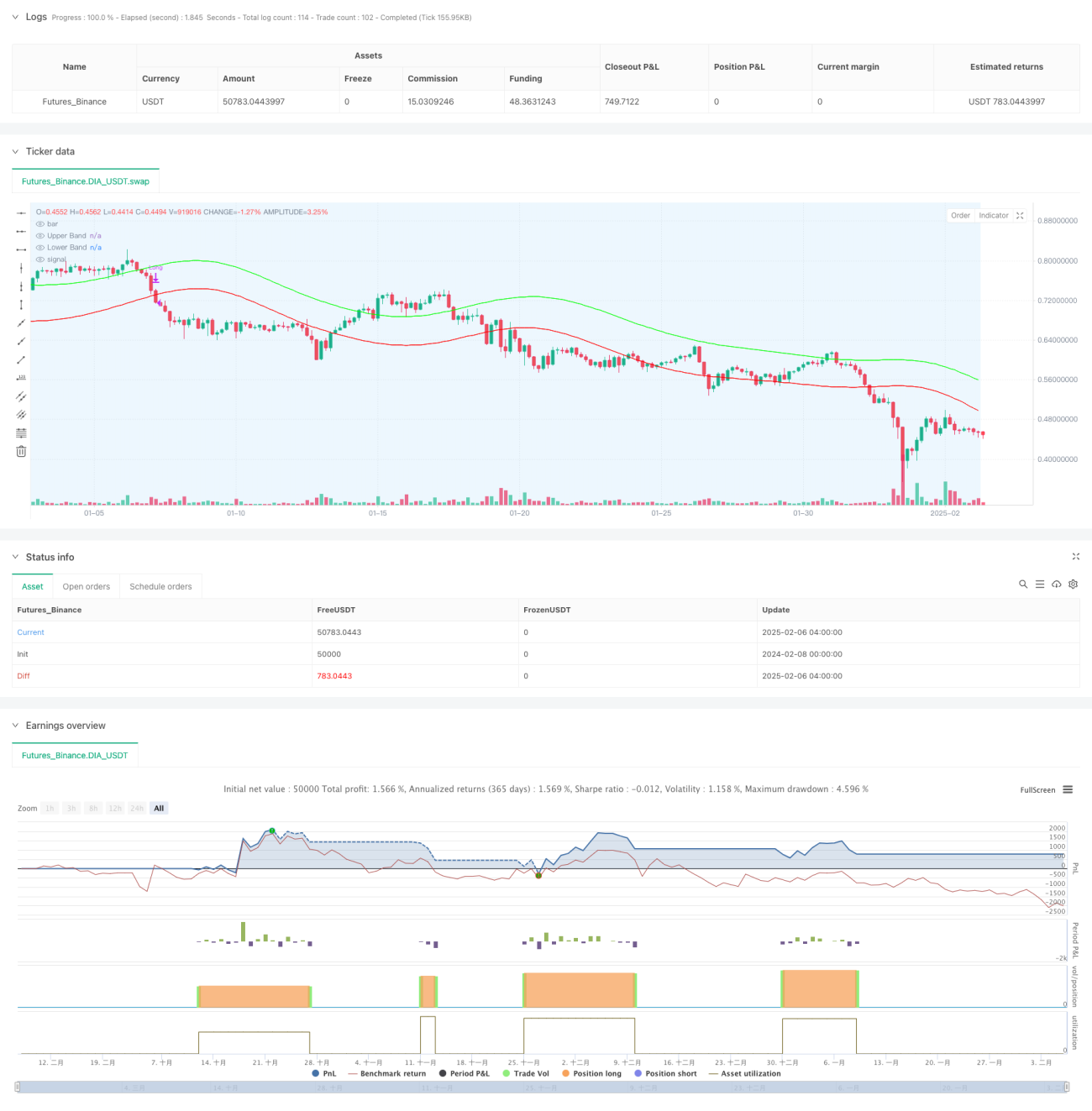

/*backtest

start: 2024-02-08 00:00:00

end: 2025-02-06 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"DIA_USDT"}]

*/

//@version=6

strategy("Demo GPT - Gold Gaussian Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1)

// ====== INPUTS ======- 1