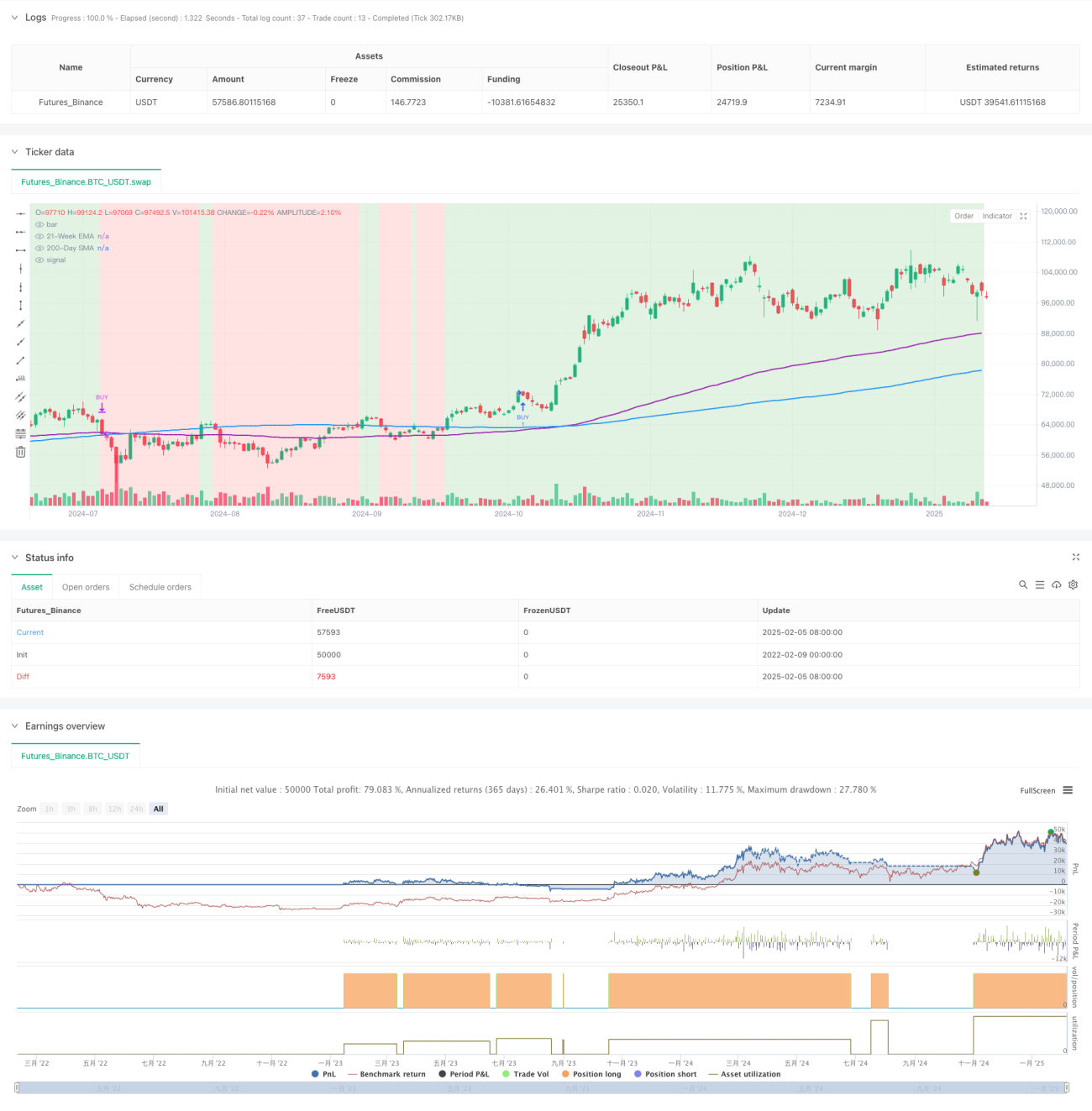

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng động dựa trên phân tích kỹ thuật, chủ yếu sử dụng đường trung bình động kép (Đường trung bình động đơn giản 200 ngày và Đường trung bình động hàm mũ 21 tuần) để nhận diện xu hướng thị trường. Chiến lược kết hợp Chỉ số sức mạnh tương đối (RSI) và Chỉ số hướng trung bình (ADX) làm bộ lọc động lượng, cùng với Phạm vi thực trung bình (ATR) để quản lý rủi ro động, giúp nắm bắt chính xác xu hướng tăng và kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược được xây dựng trên các yếu tố chính sau:

- Sử dụng sự xác nhận kép từ Đường trung bình động đơn giản 200 ngày (SMA) và Đường trung bình động hàm mũ 21 tuần (EMA) để xác định điều kiện thị trường tăng giá

- Đảm bảo động lượng tiếp tục đi lên thông qua điều kiện RSI > 50

- Kiểm tra cường độ xu hướng bằng điều kiện ADX > 25

- Cài đặt cắt lỗ động dựa trên ATR, cung cấp khả năng kiểm soát rủi ro thích ứng với biến động thị trường

- Áp dụng cơ chế chốt lời theo phần trăm, đảm bảo thu lợi kịp thời khi đạt lợi nhuận kỳ vọng

Lợi thế của chiến lược

- Hệ thống có khả năng thích ứng tốt, có thể điều chỉnh vị trí cắt lỗ động dựa trên biến động thị trường

- Sự giao nhau của hai đường trung bình động cung cấp tín hiệu xác nhận xu hướng đáng tin cậy, giảm hiệu quả rủi ro đột phá giả

- Kết hợp RSI và ADX giúp nâng cao đáng kể chất lượng tín hiệu vào lệnh

- Các tham số chiến lược có thể tùy chỉnh cao, dễ dàng tối ưu hóa theo các môi trường thị trường khác nhau

- Giao dịch theo khung ngày giúp giảm chi phí giao dịch và tác động từ biến động ngắn hạn

Rủi ro của chiến lược

- Trong thị trường dao động, có thể xuất hiện tín hiệu giả thường xuyên, làm tăng chi phí giao dịch

- Chiến lược đường trung bình vốn có độ trễ, có thể bỏ lỡ một phần lợi nhuận ở giai đoạn đầu xu hướng

- Nhiều điều kiện lọc có thể dẫn đến bỏ lỡ một số cơ hội giao dịch tiềm năng

- Trong thị trường biến động mạnh, cắt lỗ dựa trên ATR có thể quá lỏng lẻo

- Chốt lời theo tỷ lệ phần trăm cố định có thể kết thúc vị thế có lợi quá sớm trong xu hướng mạnh

Hướng tối ưu hóa chiến lược

- Có thể thêm chỉ báo khối lượng làm xác nhận phụ trợ, nâng cao độ tin cậy tín hiệu

- Cân nhắc thêm cơ chế chốt lời động để thích ứng tốt hơn với các giai đoạn thị trường khác nhau

- Tối ưu hóa cài đặt tham số RSI và ADX, cải thiện tính kịp thời của tín hiệu

- Thêm đánh giá phân cấp cường độ xu hướng, thực hiện quản lý vị thế động

- Đưa chỉ báo biến động thị trường, điều chỉnh tần suất giao dịch phù hợp trong thời kỳ biến động cao

Kết luận

Đây là một chiến lược giao dịch theo xu hướng được thiết kế hợp lý, logic rõ ràng, thông qua việc kết hợp sử dụng nhiều chỉ báo kỹ thuật, cân bằng tốt giữa lợi nhuận và rủi ro. Chiến lược có khả năng tùy chỉnh cao, phù hợp để duy trì hiệu quả thông qua tối ưu hóa tham số trong các môi trường thị trường khác nhau. Mặc dù có rủi ro độ trễ nhất định, nhưng nhờ cơ chế kiểm soát rủi ro hoàn thiện, chiến lược nhìn chung thể hiện sự ổn định và độ tin cậy tốt.

/*backtest

start: 2022-02-09 00:00:00

end: 2025-02-06 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("BTCUSDT Daily - Enhanced Bitcoin Bull Market Support [CYRANO]", shorttitle="BTCUSDT Daily BULL MARKET", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// Inputs- 1