Chiến lược chốt lời đa cấp EMA-ADX theo dõi xu hướng động

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng kết hợp chỉ báo EMA và ADX, sử dụng chốt lời nhiều mức và cắt lỗ động để tối ưu hóa quản lý vốn. Chiến lược dùng đường trung bình EMA để xác định hướng xu hướng, chỉ báo ADX để lọc độ mạnh của xu hướng, đồng thời thiết kế cơ chế chốt lời ba lớp để chốt lời theo từng phần, kết hợp ATR điều chỉnh vị trí cắt lỗ động nhằm kiểm soát rủi ro.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm các phần chính sau:

- Sử dụng đường EMA chu kỳ 50 để xác định hướng xu hướng: giá vượt lên trên EMA thì mở lệnh mua (long), vượt xuống dưới thì mở lệnh bán (short).

- Lọc xu hướng yếu bằng chỉ báo ADX chu kỳ 14: khi ADX > 20 xác nhận xu hướng có hiệu lực.

- Dựa trên ATR chu kỳ 14 để tính vị trí cắt lỗ động: lệnh mua lấy giá thấp nhất trừ đi 1 ATR, lệnh bán lấy giá cao nhất cộng thêm 1 ATR.

- Áp dụng cơ chế chốt lời ba lớp:

- Lớp 1: Chốt lời 30% vị thế tại mức 1 lần ATR.

- Lớp 2: Chốt lời 50% vị thế tại mức 2 lần ATR.

- Lớp 3: Chốt lời động 20% vị thế tại mức 3 lần ATR.

- Khi giá đạt đến vị trí chốt lời lớp 2, tự động đóng toàn bộ vị thế còn lại.

Ưu điểm của chiến lược

- Thiết kế chốt lời nhiều lớp vừa kịp thời chốt lợi nhuận, vừa không bỏ lỡ xu hướng lớn.

- Cơ chế cắt lỗ động có thể thích ứng với biến động thị trường, cung cấp kiểm soát rủi ro linh hoạt.

- Bộ lọc ADX giúp tránh hiệu quả các tín hiệu giả trong thị trường đi ngang.

- Sự giao nhau giữa EMA và giá cung cấp tín hiệu vào lệnh rõ ràng.

- Chốt lời theo từng phần giảm thiểu biến động cảm xúc, có lợi cho việc thực thi chiến lược dài hạn.

Rủi ro của chiến lược

- Trong thị trường đi ngang, có thể vào lệnh thường xuyên dẫn đến tăng chi phí giao dịch.

- EMA là chỉ báo trễ, có thể phản ứng không kịp khi thị trường đảo chiều nhanh.

- Ngưỡng ADX cố định có thể cần điều chỉnh trong các môi trường thị trường khác nhau.

- Chốt lời nhiều lớp có thể giảm vị thế quá sớm trong xu hướng một chiều.

Biện pháp giảm thiểu:

- Có thể điều chỉnh động ngưỡng ADX theo chu kỳ thị trường khác nhau.

- Cân nhắc thêm chỉ báo xác nhận xu hướng.

- Tối ưu hóa tỷ lệ phân bổ vị thế chốt lời chi tiết hơn.

Hướng tối ưu hóa chiến lược

- Đưa chỉ báo khối lượng vào để tăng cường xác nhận xu hướng.

- Điều chỉnh động ngưỡng ADX dựa trên biến động thị trường.

- Tối ưu hóa tỷ lệ phân bổ vị thế cho các lớp chốt lời.

- Thêm phân cấp độ mạnh xu hướng, tương ứng với các chiến lược chốt lời khác nhau.

- Xem xét bổ sung yếu tố mùa vụ và đánh giá chu kỳ thị trường.

Tổng kết

Đây là một chiến lược theo xu hướng có cấu trúc hoàn chỉnh, logic rõ ràng, cân bằng lợi nhuận và rủi ro thông qua chốt lời nhiều lớp và cắt lỗ động. Thiết kế tổng thể phù hợp với các nguyên tắc cơ bản của giao dịch định lượng, có khả năng mở rộng và không gian tối ưu tốt. Với điều chỉnh tham số hợp lý và nâng cấp tối ưu, chiến lược này có khả năng duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau.

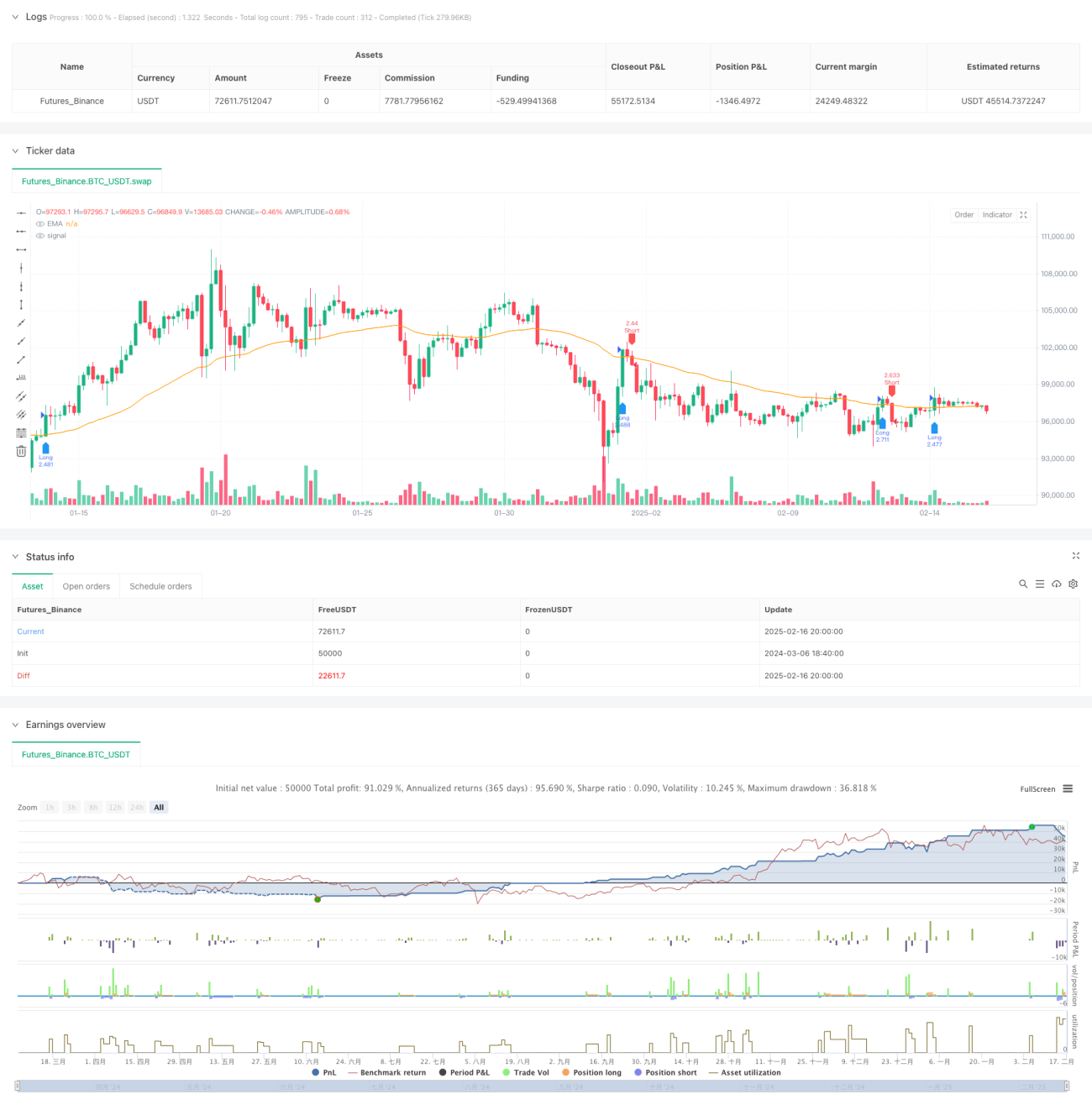

/*backtest

start: 2024-03-06 18:40:00

end: 2025-02-17 00:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("BTC Optimized Strategy v6", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// === 參數設定 ===- 1