Hệ thống tối ưu hóa chiến lược giao dịch định lượng dựa trên kênh Gaussian và Stochastic RSI

Tổng quan

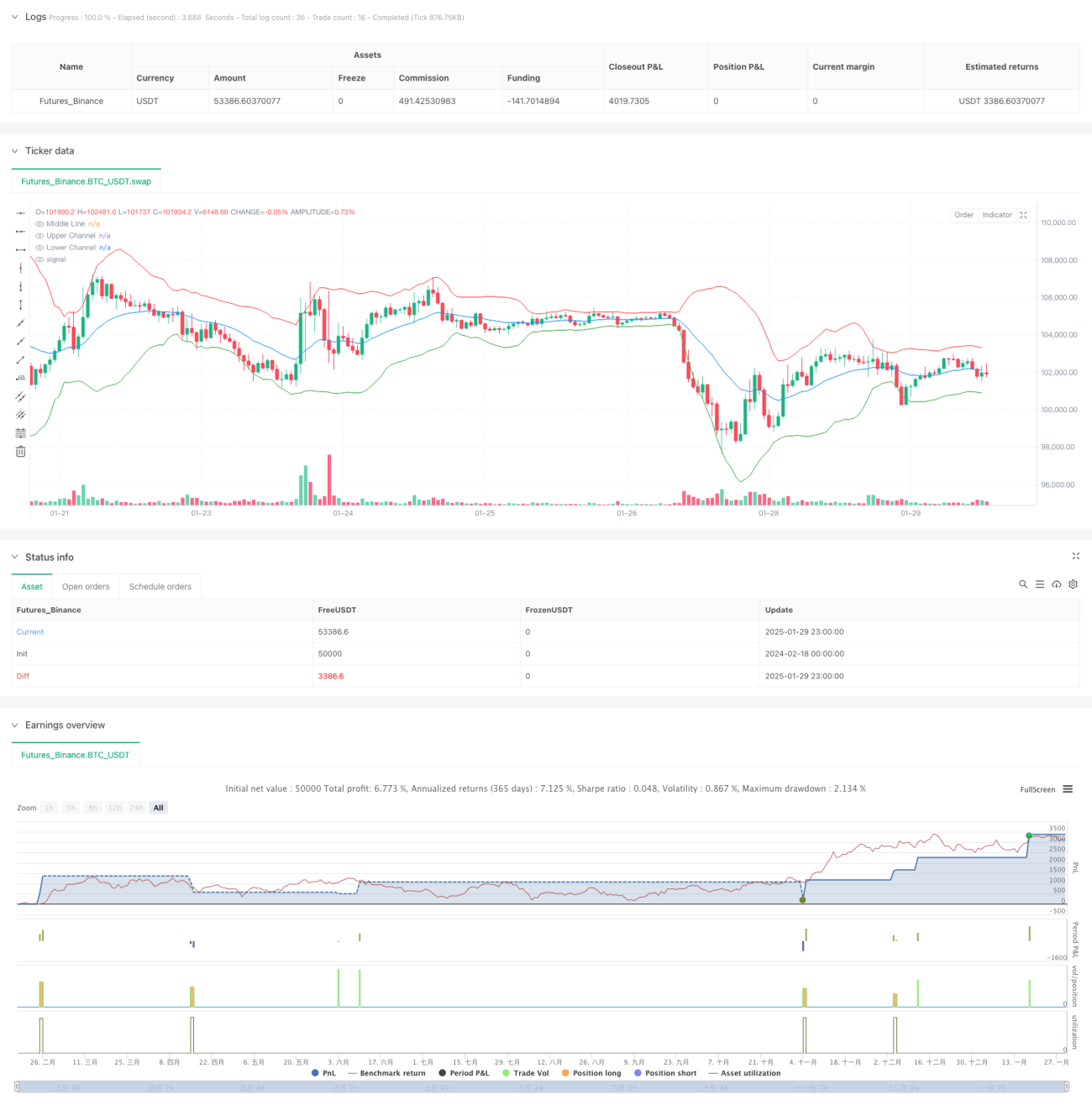

Chiến lược này là một hệ thống giao dịch định lượng dựa trên Kênh Gaussian (Gaussian Channel) và chỉ báo Stochastic RSI. Chiến lược kết hợp các nguyên lý hồi quy trung bình và động lượng trong phân tích kỹ thuật, vào lệnh mua khi giá chạm dưới đáy kênh và Stochastic RSI hiển thị tín hiệu quá bán, đồng thời thoát lệnh khi giá chạm đỉnh kênh hoặc Stochastic RSI hiển thị tín hiệu quá mua. Chiến lược này chỉ dùng để giao dịch mua, không thực hiện bán khống.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các tính toán chính sau:

- Xây dựng kênh Gaussian: Sử dụng EMA làm dây giữa, với độ rộng kênh bằng 2 lần độ lệch chuẩn để tính dây trên và dây dưới.

- Tính toán Stochastic RSI: Đầu tiên tính RSI 14 chu kỳ, sau đó tính giá trị cao nhất và thấp nhất của RSI trong 14 chu kỳ, cuối cùng xác định vị trí tương đối của RSI hiện tại trong phạm vi này.

- Tín hiệu vào lệnh: Giá phá vỡ dưới đáy kênh đồng thời Stochastic RSI vượt lên từ dưới mức 20.

- Tín hiệu thoát lệnh: Giá phá vỡ đỉnh kênh hoặc Stochastic RSI phá vỡ xuống từ trên mức 80.

Lợi thế của chiến lược

- Cơ chế xác nhận kép: Kết hợp kênh giá và chỉ báo động lượng giúp giảm thiểu tác động của tín hiệu nhiễu.

- Kiểm soát rủi ro hoàn thiện: Sử dụng quản lý vốn theo tỷ lệ phần trăm, tính đến chi phí giao dịch và trượt giá.

- Đặc tính hồi quy trung bình: Kênh Gaussian có thể nắm bắt hiệu quả phạm vi biến động của giá, nâng cao độ chính xác của giao dịch.

- Khả năng thích ứng động: Các tham số của chiến lược có thể được tối ưu điều chỉnh theo các điều kiện thị trường khác nhau.

Rủi ro của chiến lược

- Rủi ro thị trường xu hướng: Trong thị trường xu hướng mạnh, có thể đóng lệnh quá sớm, bỏ lỡ các biến động lớn.

- Nhạy cảm với tham số: Việc thiết lập hệ số kênh và tham số RSI có ảnh hưởng lớn đến hiệu suất chiến lược.

- Phụ thuộc vào môi trường thị trường: Chiến lược hoạt động tốt trong thị trường đi ngang, nhưng có thể kém hiệu quả trong thị trường một chiều.

- Rủi ro chậm tính toán: Việc tính toán các chỉ báo kỹ thuật có độ trễ nhất định, có thể ảnh hưởng đến thời điểm giao dịch.

Hướng tối ưu hóa chiến lược

- Giới thiệu tham số thích ứng: Có thể điều chỉnh động hệ số kênh dựa trên biến động thị trường.

- Bổ sung nhận dạng môi trường thị trường: Thêm chỉ báo cường độ xu hướng, sử dụng các thiết lập tham số khác nhau trong các môi trường thị trường khác nhau.

- Tối ưu hóa quản lý vốn: Có thể điều chỉnh động tỷ lệ nắm giữ dựa trên cường độ tín hiệu.

- Hoàn thiện cơ chế dừng lỗ: Thêm chức năng trailing stop, bảo vệ lợi nhuận tốt hơn.

Tổng kết

Chiến lược này kết hợp kênh Gaussian và chỉ báo Stochastic RSI để xây dựng một hệ thống giao dịch tương đối ổn định. Lợi thế của chiến lược nằm ở cơ chế xác nhận kép và kiểm soát rủi ro hoàn thiện, nhưng cũng cần chú ý đến vấn đề khả năng thích ứng với các môi trường thị trường khác nhau. Bằng cách giới thiệu các hướng tối ưu hóa như tham số thích ứng và nhận dạng môi trường thị trường, có thể nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược.

/*backtest

start: 2024-02-18 00:00:00

end: 2025-01-30 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Gaussian Channel with Stochastic RSI", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=200, commission_type=strategy.commission.percent, commission_value=0.1, slippage=0)

// Gaussian Channel Parameters- 1