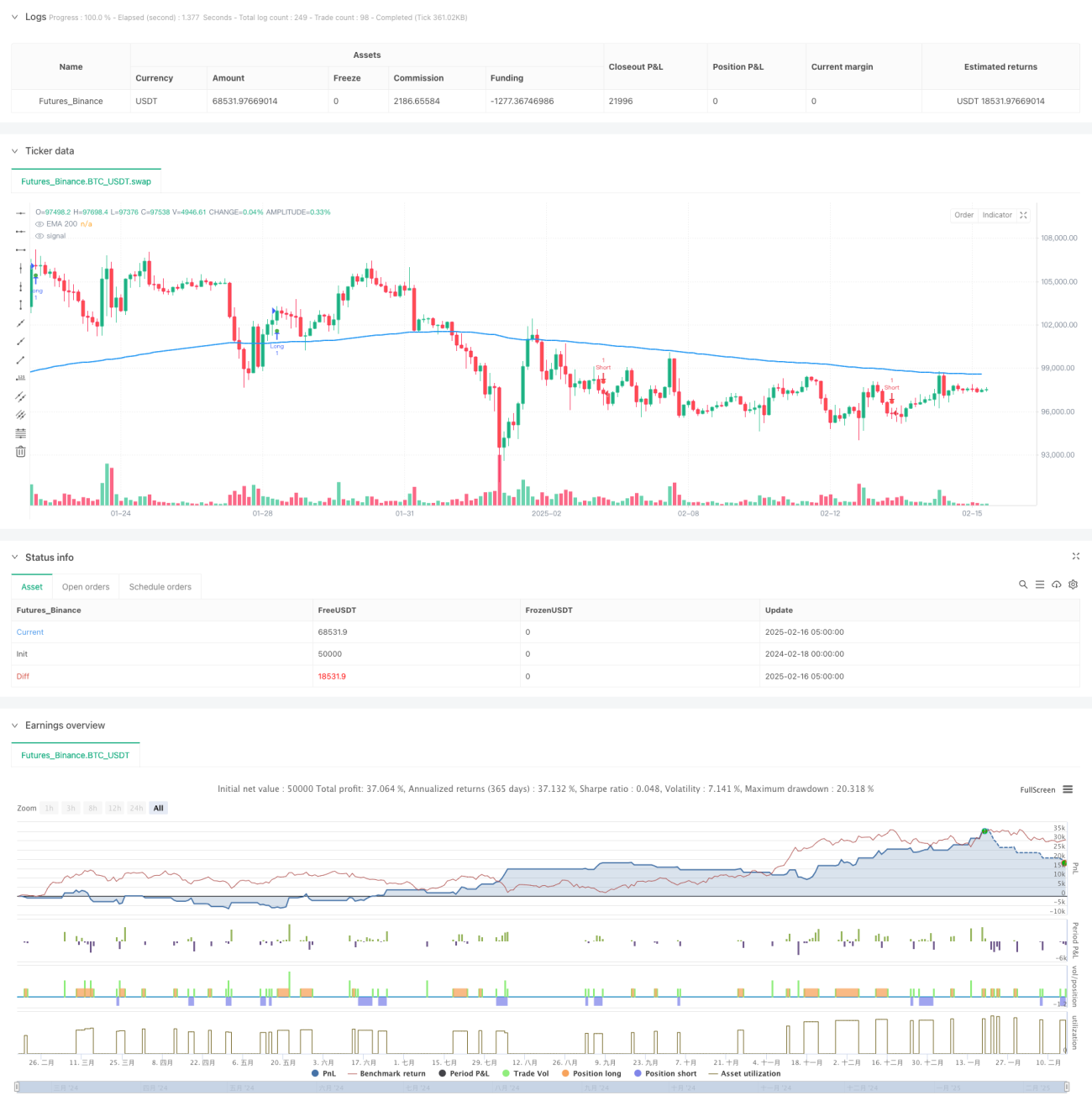

Tổng quan

Chiến lược này là một hệ thống giao dịch tổng hợp dựa trên nhiều chỉ báo kỹ thuật, kết hợp các chỉ báo động lượng, chỉ báo xu hướng và chỉ báo biến động để nắm bắt các cơ hội biến động ngắn hạn trên thị trường. Chiến lược xác định cơ hội giao dịch thông qua tín hiệu giao cắt MACD, xác nhận xu hướng bằng EMA, điều kiện RSI quá mua/quá bán và bộ lọc sức mạnh xu hướng ADX, đồng thời sử dụng mức cắt lỗ/chốt lời động dựa trên ATR để quản lý rủi ro.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các thành phần chính sau:

- Chỉ báo MACD dùng để nắm bắt sự thay đổi động lượng, xác định thời điểm vào lệnh thông qua giao cắt giữa đường nhanh và đường chậm

- Đường EMA chu kỳ 200 dùng để xác nhận hướng xu hướng tổng thể: giá nằm trên đường trung bình biểu thị xu hướng tăng, ngược lại là xu hướng giảm

- Chỉ báo RSI dùng để xác nhận động lượng giá: RSI > 50 hỗ trợ mua lên, RSI < 50 hỗ trợ bán xuống

- Chỉ báo ADX dùng để lọc các xu hướng yếu, chỉ vào lệnh khi ADX lớn hơn ngưỡng đã đặt

- Chỉ báo ATR dùng để tính toán vị trí cắt lỗ và chốt lời một cách động, tự động điều chỉnh theo biến động thị trường

Ưu điểm chiến lược

- Xác nhận chéo nhiều chỉ báo, tăng độ tin cậy của tín hiệu

- Hệ thống quản lý rủi ro động, tự động điều chỉnh cắt lỗ/chốt lời theo biến động thị trường

- Tính thích ứng cao, có thể điều chỉnh tham số theo các điều kiện thị trường khác nhau

- Cơ chế xác nhận xu hướng hoàn chỉnh, giảm rủi ro phá vỡ giả

- Logic vào lệnh và thoát lệnh có hệ thống, giảm thiểu phán đoán chủ quan

Rủi ro chiến lược

- Nhiều chỉ báo có thể dẫn đến độ trễ tín hiệu

- Khung thời gian ngắn dễ bị ảnh hưởng bởi nhiễu thị trường

- Tối ưu hóa tham số có thể dẫn đến quá khớp (overfitting)

- Giao dịch tần suất cao có thể dẫn đến chi phí giao dịch lớn

- Khi thị trường biến động mạnh có thể kích hoạt cắt lỗ thường xuyên

Hướng tối ưu hóa chiến lược

- Đưa chỉ báo khối lượng giao dịch vào làm xác nhận hỗ trợ

- Tối ưu hóa ngưỡng ADX, nâng cao hiệu quả lọc xu hướng

- Thêm bộ lọc thời gian, tránh các phiên giao dịch thanh khoản thấp

- Phát triển hệ thống tham số tự thích ứng, tăng độ ổn định của chiến lược

- Thêm bộ lọc biến động thị trường để đối phó với các môi trường thị trường khác nhau

Kết luận

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách kết hợp nhiều chỉ báo kỹ thuật. Mặc dù tồn tại một số hạn chế về độ trễ và thách thức tối ưu hóa tham số, nhưng với quản lý rủi ro hợp lý và cải tiến liên tục, chiến lược thể hiện tính thích ứng và độ tin cậy khá tốt. Khuyến nghị nhà giao dịch thực hiện backtest đầy đủ và tối ưu hóa tham số trước khi sử dụng trên tài khoản thực.

- 1