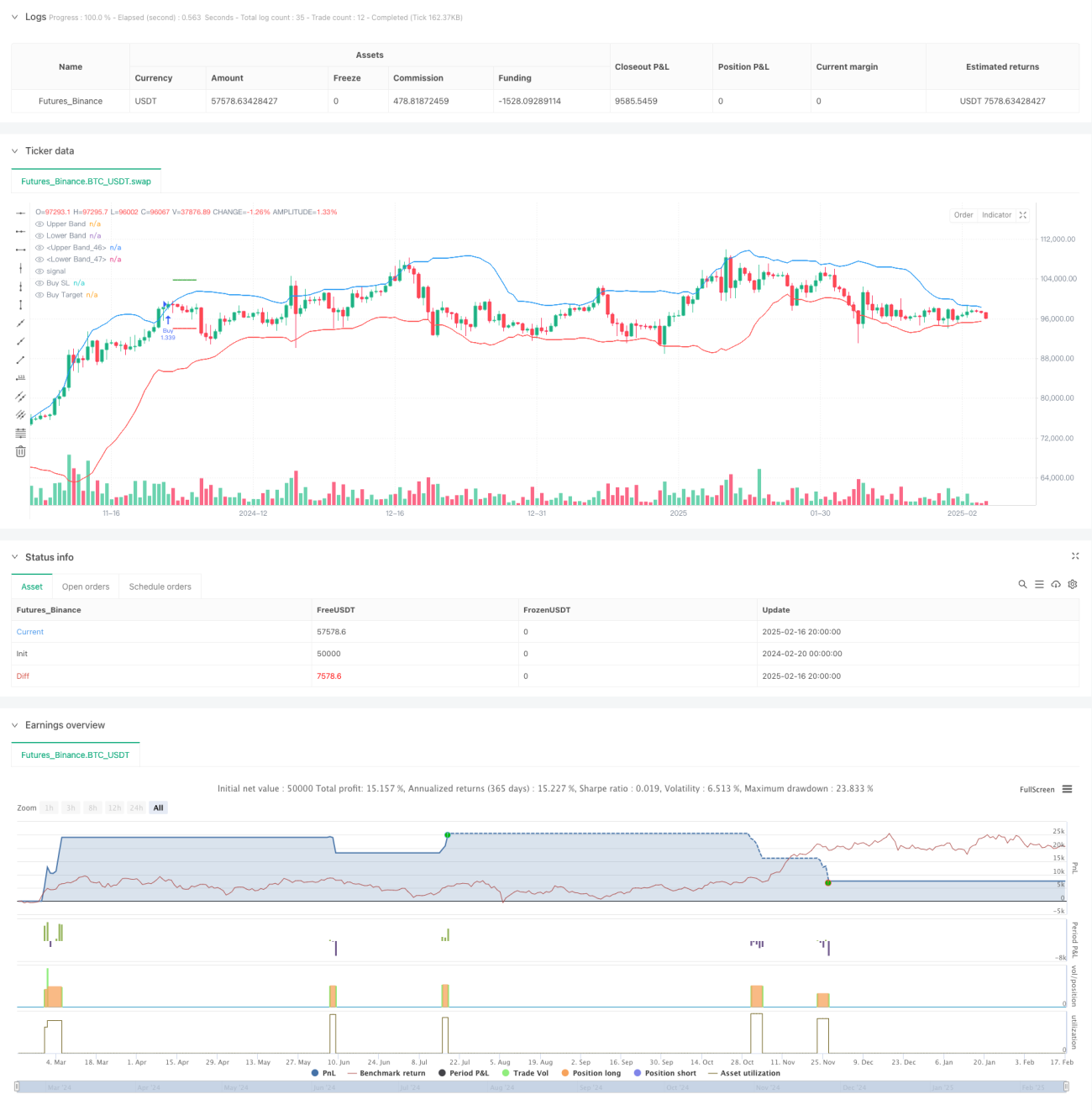

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng dựa trên sự phá vỡ dải Bollinger và mô hình nến. Chiến lược xác định tín hiệu giao dịch bằng cách nhận diện ba nến liên tiếp phá vỡ dải Bollinger, kết hợp với vị trí giá đóng cửa trong thân nến. Hệ thống sử dụng tỷ lệ rủi ro/lợi nhuận cố định 1:1 để quản lý cắt lỗ và chốt lời cho mỗi giao dịch.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Sử dụng dải Bollinger chu kỳ 20 làm chỉ báo chính, với độ lệch chuẩn là 2.0

- Điều kiện vào lệnh mua: Ba nến liên tiếp có giá đóng cửa phá vỡ dải trên, cả ba nến đều là nến tăng, giá đóng cửa đều nằm ở nửa trên của thân nến

- Điều kiện vào lệnh bán: Ba nến liên tiếp có giá đóng cửa phá vỡ dải dưới, cả ba nến đều là nến giảm, giá đóng cửa đều nằm ở nửa dưới của thân nến

- Cắt lỗ được đặt tại điểm cực trị của nến tín hiệu đầu tiên

- Đặt vị trí chốt lời dựa trên tỷ lệ rủi ro/lợi nhuận 1:1

Ưu điểm của chiến lược

- Sử dụng cơ chế xác nhận đa lớp, thông qua yêu cầu về hình thái của ba nến phá vỡ liên tiếp, giúp giảm hiệu quả rủi ro phá vỡ giả

- Kết hợp đánh giá vị trí giá đóng cửa trong thân nến, tăng cường độ tin cậy của xác nhận xu hướng

- Sử dụng tỷ lệ rủi ro/lợi nhuận cố định để quản lý vị thế, dễ dàng kiểm soát rủi ro

- Logic chiến lược rõ ràng, dễ hiểu và dễ thực hiện

- Hiển thị trực quan tín hiệu giao dịch thông qua chức năng đánh dấu, thuận tiện cho phân tích backtest

Rủi ro của chiến lược

- Trong thị trường dao động có thể tạo ra nhiều tín hiệu giả

- Tỷ lệ rủi ro/lợi nhuận cố định có thể không tận dụng được hết các xu hướng mạnh

- Yêu cầu nghiêm ngặt về ba nến liên tiếp có thể bỏ lỡ một số cơ hội tiềm năng

- Cắt lỗ đặt tại điểm cực trị của nến tín hiệu, khi biến động lớn vị trí cắt lỗ có thể quá xa

Khuyến nghị quản lý rủi ro bằng các cách sau:

- Kết hợp chu kỳ biến động thị trường để điều chỉnh tham số dải Bollinger

- Điều chỉnh linh hoạt tỷ lệ rủi ro/lợi nhuận dựa trên đặc điểm thị trường

- Thêm chỉ báo xác nhận xu hướng

- Tối ưu hóa phương pháp đặt vị trí cắt lỗ

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số:

- Có thể điều chỉnh linh hoạt chu kỳ dải Bollinger và bội số độ lệch chuẩn dựa trên đặc điểm thị trường khác nhau

- Cân nhắc thay đổi yêu cầu ba nến thành đánh giá động

- Tối ưu hóa tín hiệu:

- Thêm chỉ báo xác nhận xu hướng như ADX hoặc đường xu hướng

- Đưa cơ chế xác nhận khối lượng giao dịch

- Cân nhắc thêm chỉ báo dao động làm hỗ trợ

- Tối ưu hóa quản lý vị thế:

- Thực hiện thiết lập tỷ lệ rủi ro/lợi nhuận động

- Thêm mô-đun quản lý vốn

- Cân nhắc cơ chế vào và thoát lệnh theo từng phần

- Tối ưu hóa cắt lỗ:

- Đưa cơ chế trailing stop

- Đặt khoảng cách cắt lỗ dựa trên ATR

- Cân nhắc cắt lỗ theo thời gian

Tổng kết

Đây là một chiến lược theo xu hướng có cấu trúc hoàn chỉnh, logic rõ ràng. Thông qua cơ chế xác nhận đa lớp từ phá vỡ dải Bollinger và hình thái nến, đã giảm hiệu quả rủi ro tín hiệu giả. Tỷ lệ rủi ro/lợi nhuận cố định đơn giản hóa việc quản lý giao dịch, nhưng cũng hạn chế tính linh hoạt của chiến lược. Bằng cách tối ưu hóa tham số, thêm chỉ báo xác nhận, cải thiện quản lý vị thế, chiến lược vẫn còn nhiều không gian cải thiện. Nhìn chung, đây là một khung chiến lược cơ bản có giá trị thực tiễn, có thể được hoàn thiện thêm dựa trên nhu cầu cụ thể.

/*backtest

start: 2024-02-20 00:00:00

end: 2025-02-17 08:00:00

period: 12h

basePeriod: 12h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Bollinger Band Strategy (Close Near High/Low Relative to Half Range)", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=200, pyramiding=0)

// Bollinger Bands- 1