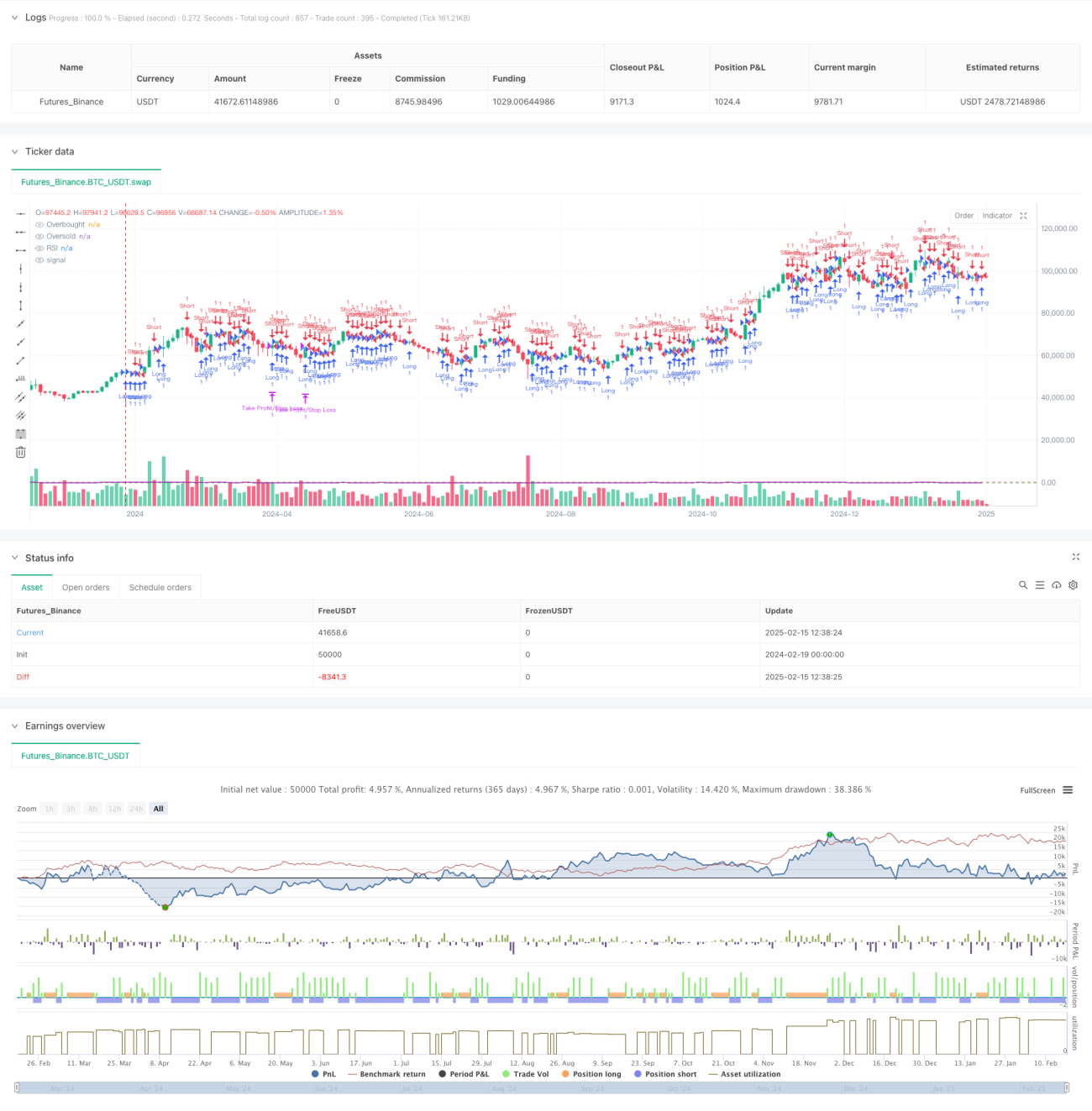

Chiến lược giao dịch theo dõi xu hướng đột phá RSI động kết hợp hệ thống tối ưu hóa tỷ lệ rủi ro-lợi nhuận

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng dựa trên sự phá vỡ RSI (Chỉ số Sức mạnh Tương đối), kết hợp tỷ lệ rủi ro/lợi nhuận 1:4 để tối ưu hóa hiệu suất giao dịch. Chiến lược xác định đường xu hướng hình thành từ các đỉnh và đáy của chỉ báo RSI, vào lệnh khi có sự phá vỡ, đồng thời sử dụng tỷ lệ rủi ro/lợi nhuận cố định để thiết lập vị trí cắt lỗ và chốt lời, qua đó quản lý giao dịch một cách có hệ thống.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Tín hiệu phá vỡ đường xu hướng RSI: Hệ thống theo dõi các đỉnh cục bộ và đáy cục bộ của RSI để hình thành đường xu hướng động. Khi RSI phá vỡ đường xu hướng đỉnh thì mở vị thế Long (mua), phá vỡ đường xu hướng đáy thì mở vị thế Short (bán).

- Xác định thời điểm vào lệnh: Sử dụng so sánh giá trị RSI của ba nến để xác nhận đỉnh cục bộ và đáy cục bộ, nâng cao độ chính xác của đường xu hướng.

- Cơ chế quản lý rủi ro: Sử dụng giá thấp nhất của nến trước đó làm cắt lỗ cho vị thế Long và giá cao nhất làm cắt lỗ cho vị thế Short, đảm bảo kiểm soát rủi ro rõ ràng.

- Thiết kế tối ưu lợi nhuận: Sử dụng tỷ lệ rủi ro/lợi nhuận 1:4 để thiết lập vị trí chốt lời, theo đuổi không gian lợi nhuận lớn hơn trong khi kiểm soát rủi ro.

Ưu điểm chiến lược

- Ra quyết định có hệ thống: Thông qua việc nhận dạng đường xu hướng RSI và xác định phá vỡ theo chương trình, tránh được sự thiên kiến chủ quan.

- Kiểm soát rủi ro chặt chẽ: Sử dụng biến động giá gần đây để thiết lập cắt lỗ, kiểm soát rủi ro tối đa mỗi giao dịch.

- Tối ưu tỷ lệ lợi nhuận/rủi ro: Thiết lập tỷ lệ rủi ro/lợi nhuận cố định 1:4, nâng cao kỳ vọng lợi nhuận của chiến lược.

- Đặc tính theo xu hướng: Có thể nắm bắt hiệu quả các xu hướng trung và dài hạn, tăng cơ hội sinh lời.

- Khả năng thích ứng cao: Có thể áp dụng cho các thị trường và khung thời gian khác nhau.

Rủi ro chiến lược

- Rủi ro phá vỡ giả: Sau khi RSI phá vỡ có thể xảy ra phá vỡ giả, dẫn đến thoát lệnh do cắt lỗ.

- Khoảng cách chốt lời quá xa: Tỷ lệ rủi ro/lợi nhuận 1:4 có thể khiến vị trí chốt lời khó đạt được.

- Hiệu suất trong thị trường đi ngang: Trong thị trường dao động ngang (sideway) có thể kích hoạt thường xuyên các tín hiệu giả.

- Ảnh hưởng của trượt giá: Trong thị trường có thanh khoản kém, giá cắt lỗ thực tế có thể chênh lệch so với kỳ vọng.

Hướng tối ưu hóa chiến lược

- Tỷ lệ rủi ro/lợi nhuận động: Có thể điều chỉnh tỷ lệ rủi ro/lợi nhuận linh hoạt dựa trên biến động thị trường.

- Xác nhận xu hướng: Thêm các chỉ báo xác nhận xu hướng, như đường trung bình động hoặc chỉ báo ATR.

- Quản lý vị thế: Giới thiệu hệ thống quản lý vị thế dựa trên biến động.

- Tối ưu hóa thoát lệnh: Thêm cơ chế cắt lỗ di động hoặc chốt lời theo từng phần.

- Bộ lọc thời gian: Thêm bộ lọc khung giờ giao dịch, tránh các khoảng thời gian có thanh khoản thấp.

Tổng kết

Chiến lược này kết hợp phá vỡ RSI và tỷ lệ rủi ro/lợi nhuận cố định để xây dựng một hệ thống giao dịch theo xu hướng hoàn chỉnh. Ưu điểm của chiến lược nằm ở quy trình ra quyết định có hệ thống và kiểm soát rủi ro chặt chẽ, nhưng trong ứng dụng thực tế cần chú ý đến phá vỡ giả và tác động của môi trường thị trường. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược có thể đạt được hiệu suất ổn định hơn trong các điều kiện thị trường khác nhau.

- 1