Chiến lược giao dịch định lượng tiền điện tử dựa trên DCA động

Tổng quan

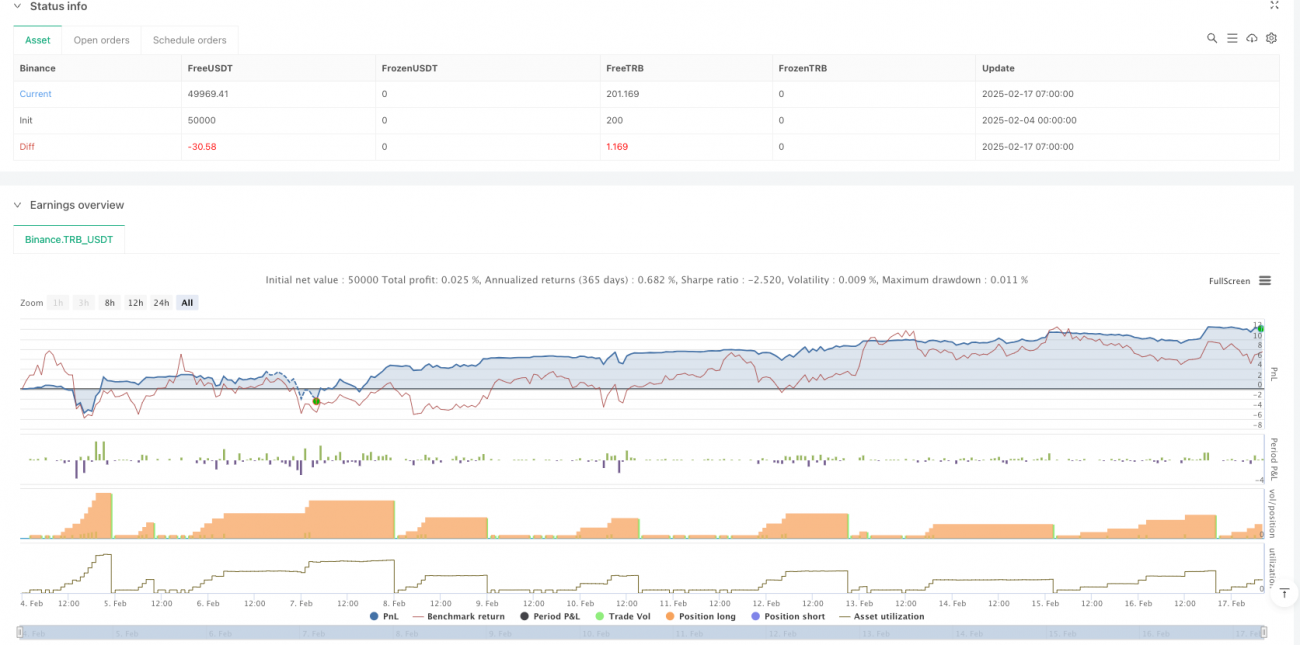

Đây là một chiến lược giao dịch định lượng được thiết kế dành riêng cho thị trường tiền điện tử, tận dụng triệt để đặc điểm biến động cao của thị trường này. Thông qua phương pháp trung bình chi phí thông minh (DCA), chiến lược sẽ gia tăng vị thế một cách linh hoạt khi giá điều chỉnh. Chiến lược hoạt động trên khung thời gian 15 phút, có thể ứng phó hiệu quả với các biến động nhanh của thị trường tiền điện tử, đồng thời tránh rủi ro từ giao dịch quá mức.

Nguyên lý chiến lược

Chiến lược bao gồm bốn mô-đun cốt lõi:

- Hệ thống vào lệnh thông minh: Xây dựng vị thế ban đầu dựa trên giá trung bình gia quyền OHLC4, thích ứng với đặc tính biến động cao của thị trường tiền điện tử.

- Cơ chế bổ sung vị thế động: Kích hoạt lệnh an toàn khi giá điều chỉnh, khối lượng bổ sung tăng dần theo độ sâu của biến động, tận dụng tối đa biến động thị trường.

- Hệ thống quản lý rủi ro: Tối ưu tỷ lệ rủi ro-lợi nhuận thông qua cơ chế gia tăng vị thế hình tháp và điều chỉnh đòn bẩy linh hoạt.

- Kiểm soát chốt lời nhanh: Cơ chế chốt lời được thiết kế cho biến động nhanh của thị trường tiền điện tử, bao gồm tối ưu hóa phí giao dịch.

Lợi thế chiến lược

- Thích ứng thị trường: Được tối ưu hóa dành riêng cho đặc tính biến động cao của thị trường tiền điện tử.

- Phân tán rủi ro: Giảm thiểu rủi ro đột ngột của thị trường tiền điện tử thông qua việc xây dựng vị thế theo từng đợt linh hoạt.

- Hiệu quả chênh lệch giá: Tận dụng biến động giá của thị trường tiền điện tử để thu lợi nhuận.

- Tự động hóa thực thi: Hỗ trợ kết nối API của nhiều sàn giao dịch tiền điện tử lớn.

- Hiệu quả vốn: Nâng cao hiệu quả sử dụng vốn trong giao dịch tiền điện tử thông qua quản lý đòn bẩy thông minh.

Rủi ro chiến lược

- Rủi ro thị trường: Biến động cực đoan của thị trường tiền điện tử có thể dẫn đến sụt giảm lớn.

- Rủi ro thanh khoản: Một số loại tiền điện tử vốn hóa nhỏ có thể gặp vấn đề thanh khoản.

- Rủi ro đòn bẩy: Biến động cao của thị trường tiền điện tử làm tăng rủi ro khi sử dụng đòn bẩy.

- Rủi ro kỹ thuật: Phụ thuộc vào độ ổn định của API sàn giao dịch và chất lượng kết nối mạng.

- Rủi ro pháp lý: Các thay đổi chính sách đối với thị trường tiền điện tử có thể ảnh hưởng đến việc thực thi chiến lược.

Hướng tối ưu hóa chiến lược

- Tự thích ứng với độ biến động: Đưa vào các chỉ báo biến động đặc thù của thị trường tiền điện tử để điều chỉnh tham số linh hoạt.

- Phối hợp đa đồng tiền: Phát triển logic giao dịch liên kết nhiều đồng tiền, phân tán rủi ro từ một đồng tiền duy nhất.

- Lọc tâm lý thị trường: Tích hợp các chỉ báo tâm lý thị trường tiền điện tử, tối ưu hóa thời điểm vào lệnh.

- Tối ưu hóa chi phí giao dịch: Giảm chi phí thông qua định tuyến thông minh và lựa chọn sàn giao dịch.

- Cơ chế cảnh báo rủi ro: Xây dựng hệ thống cảnh báo dựa trên biến động bất thường của thị trường.

Tổng kết

Chiến lược này cung cấp một giải pháp tự động hóa toàn diện cho giao dịch tiền điện tử thông qua phương pháp DCA sáng tạo và quản lý rủi ro linh hoạt. Mặc dù thị trường tiền điện tử có rủi ro cao, nhưng nhờ cơ chế kiểm soát rủi ro được thiết kế kỹ lưỡng và tối ưu hóa thích ứng thị trường, chiến lược có thể duy trì sự ổn định trong hầu hết các điều kiện thị trường. Các cải tiến trong tương lai sẽ tập trung vào việc nâng cao khả năng thích ứng của chiến lược với các đặc thù của thị trường tiền điện tử.

/*backtest

start: 2020-08-29 15:00:00

end: 2025-02-18 17:22:45

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"TRB_USDT"}]

*/

//@version=5

strategy('Autotrade.it DCA', overlay=true, pyramiding=999, default_qty_type=strategy.cash, initial_capital=10000, commission_value=0.02)

// Date Ranges- 1