Chiến lược tối ưu hóa theo dõi xu hướng giao cắt EMA và dừng lỗ động ATR

Tổng quan

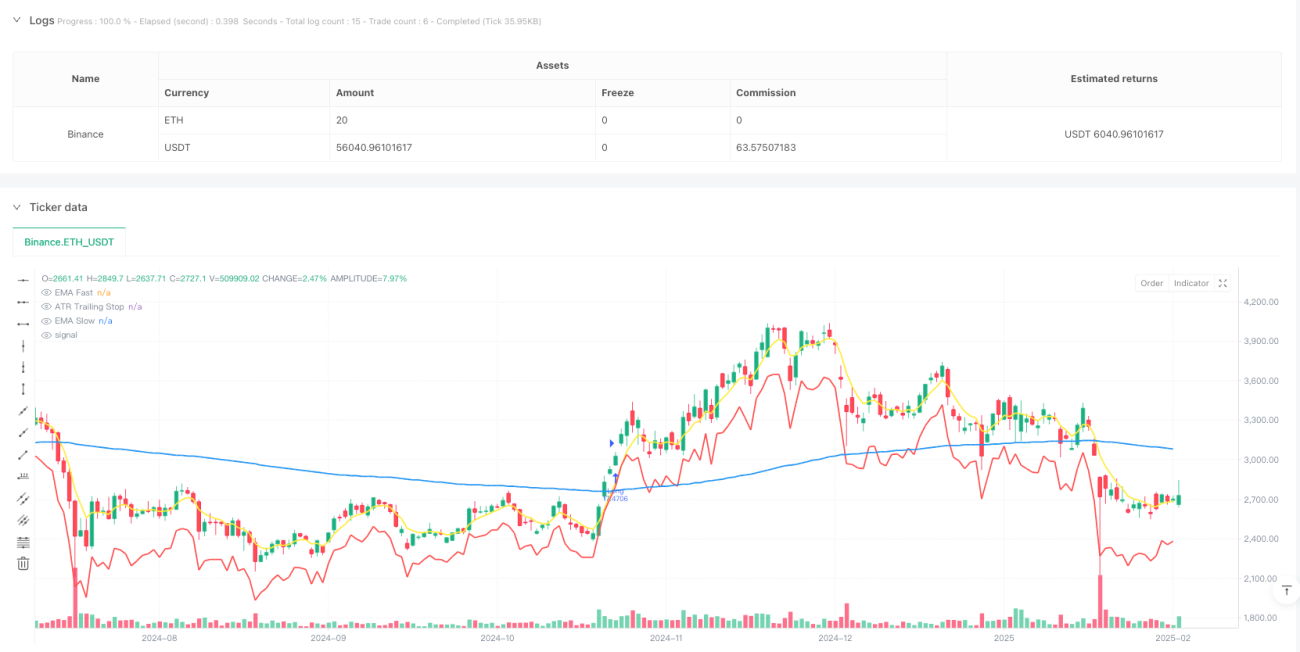

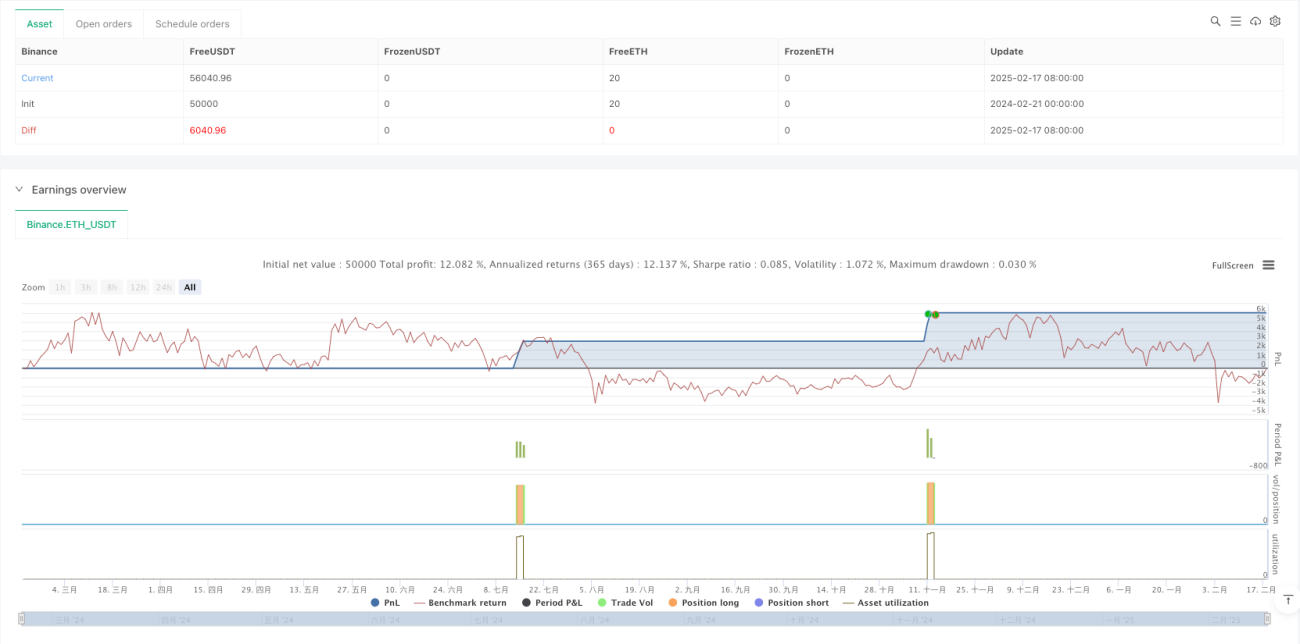

Chiến lược này là một hệ thống theo dõi xu hướng dựa trên sự giao cắt của đường trung bình động và cắt lỗ động. Logic cốt lõi là sử dụng điểm giao cắt vàng của đường trung bình động nhanh (EMA5) và đường trung bình động chậm (EMA200) để nắm bắt điểm khởi đầu của xu hướng tăng, kết hợp với cắt lỗ động dựa trên ATR để bảo vệ lợi nhuận. Chiến lược cũng thiết lập mục tiêu chốt lời theo tỷ lệ phần trăm cố định nhằm đạt được sự cân bằng giữa rủi ro và lợi nhuận.

Nguyên lý chiến lược

Chiến lược hoạt động dựa trên các cơ chế cốt lõi sau:

- Tín hiệu vào lệnh được kích hoạt khi EMA5 vượt lên trên EMA200, cho thấy động lượng ngắn hạn đã phá vỡ xu hướng dài hạn.

- Cắt lỗ động được tính toán dựa trên chỉ báo ATR, giá cắt lỗ được đặt bằng giá đóng cửa trừ đi giá trị ATR nhân với hệ số.

- Mục tiêu chốt lời được đặt ở mức phần trăm cố định của giá vào lệnh (mặc định 5%).

- Trong thời gian nắm giữ, giá cắt lỗ ATR sẽ được dịch chuyển lên theo giá tăng, tạo thành một lệnh cắt lỗ bám đuổi (trailing stop).

- Khi giá chạm mức cắt lỗ hoặc đạt mục tiêu chốt lời, chiến lược tự động đóng vị thế.

Ưu điểm của chiến lược

- Khả năng bắt xu hướng mạnh - Hệ thống giao cắt EMA có thể nhận diện hiệu quả giai đoạn đầu của xu hướng.

- Quản lý rủi ro linh hoạt - Cắt lỗ động ATR có thể tự động điều chỉnh theo biến động thị trường.

- Tính thực thi ổn định - Các quy tắc vào và ra lệnh mang tính hệ thống, tránh sự can thiệp của cảm xúc con người.

- Khả năng điều chỉnh tham số cao - Chu kỳ đường trung bình, hệ số ATR và tỷ lệ chốt lời đều có thể tối ưu theo nhu cầu.

- Logic vận hành rõ ràng - Các quy tắc chiến lược đơn giản và minh bạch, dễ hiểu và dễ thực hiện.

Rủi ro của chiến lược

- Rủi ro phá vỡ giả - Thị trường đi ngang có thể tạo ra nhiều tín hiệu giao cắt không hiệu quả.

- Rủi ro sụt giảm - Khi xu hướng đảo chiều đột ngột, có thể chịu mức sụt giảm lớn.

- Rủi ro trượt giá - Trong thị trường biến động nhanh, lệnh cắt lỗ hoặc chốt lời có thể đối mặt với trượt giá.

- Độ nhạy tham số - Các tham số tối ưu có thể khác biệt đáng kể trong các môi trường thị trường khác nhau.

- Rủi ro quản lý vốn - Tỷ lệ vị thế cố định có thể gây rủi ro quá lớn trong một số trường hợp.

Hướng tối ưu hóa chiến lược

- Thêm bộ lọc xu hướng - Có thể đưa vào các chỉ báo cường độ xu hướng như ADX để lọc các thị trường yếu.

- Tối ưu cơ chế cắt lỗ - Có thể kết hợp các mức hỗ trợ hoặc tỷ lệ phần trăm biến động để đặt cắt lỗ.

- Điều chỉnh chốt lời động - Điều chỉnh mục tiêu chốt lời linh hoạt theo biến động thị trường hoặc cường độ xu hướng.

- Thêm bộ lọc thời gian - Tránh các khung thời gian có biến động lớn.

- Hoàn thiện quản lý vị thế - Đưa vào cơ chế quản lý vị thế động, điều chỉnh theo mức độ rủi ro thị trường.

Tổng kết

Đây là một chiến lược theo dõi xu hướng kết hợp các chỉ báo kỹ thuật cổ điển với quản lý rủi ro hiện đại. Bằng cách bắt xu hướng thông qua giao cắt đường trung bình động và sử dụng cắt lỗ động ATR để bảo vệ lợi nhuận, chiến lược này hoạt động xuất sắc trong các thị trường có xu hướng. Mặc dù tồn tại rủi ro về tín hiệu giả, nhưng thông qua tối ưu hóa tham số và thêm bộ lọc, có thể cải thiện đáng kể tính ổn định của chiến lược. Ưu điểm cốt lõi của chiến lược nằm ở logic vận hành mang tính hệ thống và cơ chế quản lý rủi ro linh hoạt, phù hợp làm khung chiến lược cơ bản cho giao dịch xu hướng trung và dài hạn.

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// -----------------------------------------------------------

// Title: EMA5 Cross-Up EMA200 with ATR Trailing Stop & Take-Profit

// Author: ChatGPT

// Version: 1.1 (Pine Script v6)- 1