Tổng quan

Đây là một hệ thống chiến lược giao dịch tần suất cao kết hợp Bollinger Bands, MACD (Đường trung bình động phân kỳ hội tụ) và phân tích khối lượng giao dịch. Chiến lược này xác định các cơ hội đảo chiều của thị trường thông qua việc phát hiện sự phá vỡ và quay trở lại của giá tại các dải trên/dưới của Bollinger Bands, kết hợp với chỉ báo động lượng MACD và xác nhận khối lượng giao dịch. Hệ thống thiết lập giới hạn số lần giao dịch tối đa mỗi ngày và được trang bị cơ chế quản lý rủi ro hoàn chỉnh.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa trên sự kết hợp của ba chỉ báo cốt lõi sau:

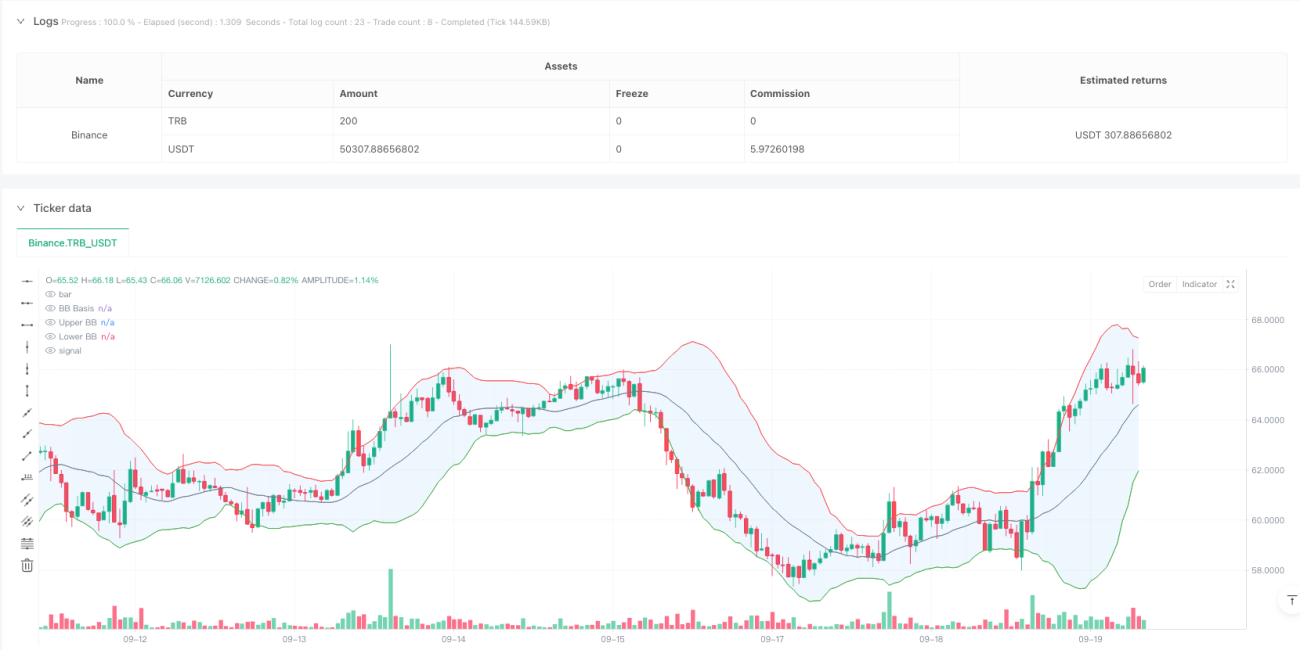

- Chỉ báo Bollinger Bands: Sử dụng đường trung bình động đơn giản (SMA) 20 kỳ làm dải giữa, với hệ số nhân độ lệch chuẩn là 2.0 để tính dải trên và dải dưới. Khi giá phá vỡ Bollinger Bands rồi quay trở lại, hệ thống sẽ đưa ra tín hiệu giao dịch tiềm năng.

- Chỉ báo MACD: Sử dụng cài đặt tham số tiêu chuẩn (12, 26, 9) để xác nhận động lượng xu hướng giá. Khi đường MACD nằm trên đường tín hiệu, xác nhận tín hiệu mua; khi nằm dưới đường tín hiệu, xác nhận tín hiệu bán.

- Phân tích khối lượng: Sử dụng đường trung bình động 20 kỳ để xác nhận khối lượng giao dịch, yêu cầu khối lượng khi xuất hiện tín hiệu phải ít nhất bằng mức trung bình để đảm bảo mức độ tham gia thị trường.

Lợi thế của chiến lược

- Xác nhận tín hiệu đa lớp: Thông qua ba lớp xác nhận là Bollinger Bands, MACD và khối lượng giao dịch, độ tin cậy của tín hiệu giao dịch được tăng cường đáng kể.

- Thiết kế trực quan: Hệ thống cung cấp các chỉ thị biểu đồ phong phú, bao gồm tô màu dải Bollinger, đánh dấu tín hiệu và thay đổi màu nền, giúp nhà giao dịch dễ dàng nhận diện nhanh các cơ hội giao dịch.

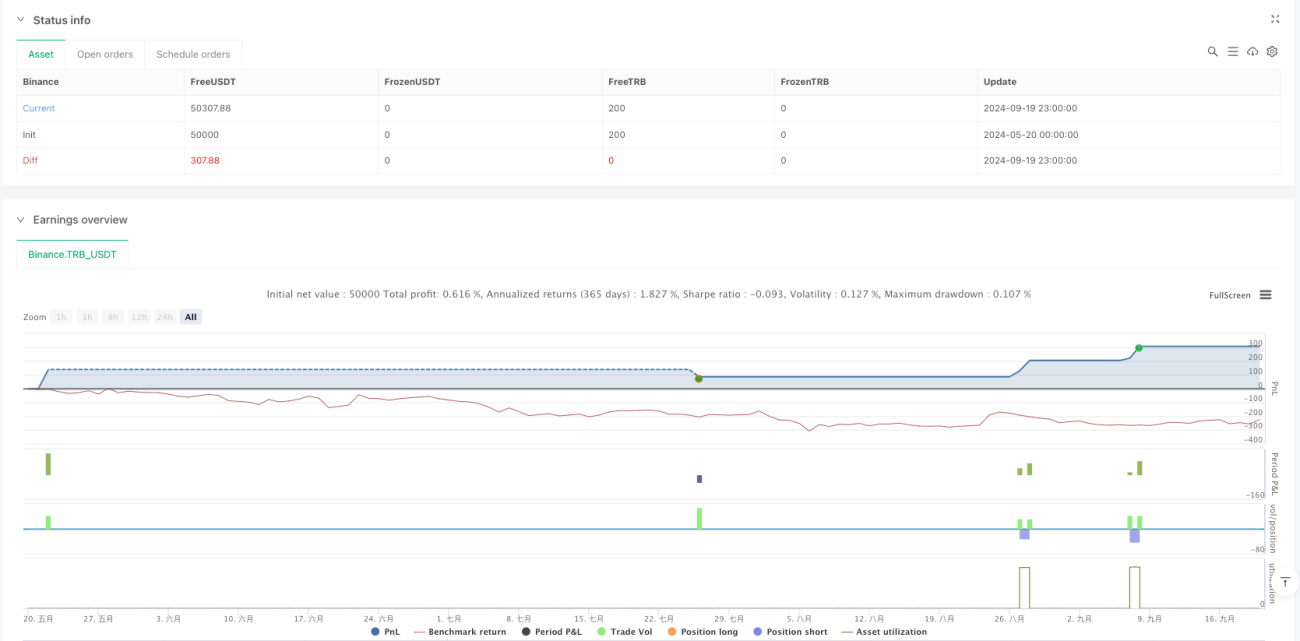

- Kiểm soát rủi ro hoàn chỉnh: Thực hiện cắt lỗ cố định và mục tiêu chốt lời, đồng thời giới hạn số lần giao dịch tối đa mỗi ngày, kiểm soát hiệu quả mức độ rủi ro.

- Vận hành có hệ thống: Chiến lược cung cấp các điều kiện vào và ra lệnh rõ ràng, giảm thiểu sự không chắc chắn do đánh giá chủ quan.

Rủi ro của chiến lược

- Rủi ro biến động thị trường: Trong thị trường có biến động cao, có thể xuất hiện các tín hiệu phá vỡ giả, dẫn đến thua lỗ giao dịch.

- Rủi ro trượt giá: Trong môi trường giao dịch tần suất cao, có thể đối mặt với chi phí trượt giá lớn, ảnh hưởng đến lợi nhuận thực tế.

- Rủi ro thanh khoản: Điều kiện về khối lượng giao dịch có thể hạn chế cơ hội giao dịch khi thị trường thiếu thanh khoản.

- Rủi ro hệ thống: Các cài đặt tham số cố định có thể không thích ứng được với những thay đổi mạnh mẽ của điều kiện thị trường.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số động: Có thể đưa vào cơ chế điều chỉnh tham số thích ứng, cho phép các tham số của Bollinger Bands và MACD tự động điều chỉnh theo điều kiện thị trường.

- Nhận diện chu kỳ thị trường: Bổ sung mô-đun đánh giá chu kỳ thị trường, áp dụng các chiến lược giao dịch khác nhau trong các chu kỳ thị trường khác nhau.

- Tối ưu hóa quản lý rủi ro: Có thể xem xét đưa vào cơ chế cắt lỗ động, điều chỉnh vị trí cắt lỗ dựa trên biến động của thị trường.

- Tăng cường lọc tín hiệu: Thêm bộ lọc cường độ xu hướng, tránh tạo ra quá nhiều tín hiệu giao dịch trong thị trường đi ngang.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh thông qua sự kết hợp giữa tín hiệu đảo chiều của Bollinger Bands, xác nhận xu hướng của MACD và xác nhận khối lượng giao dịch. Thiết kế trực quan và kiểm soát rủi ro chặt chẽ của hệ thống khiến nó đặc biệt phù hợp cho giao dịch trong ngày. Mặc dù tồn tại một số rủi ro thị trường nhất định, nhưng thông qua việc tối ưu hóa liên tục và điều chỉnh tham số, chiến lược này có tiềm năng duy trì hiệu suất ổn định trong các điều kiện thị trường khác nhau.

- 1