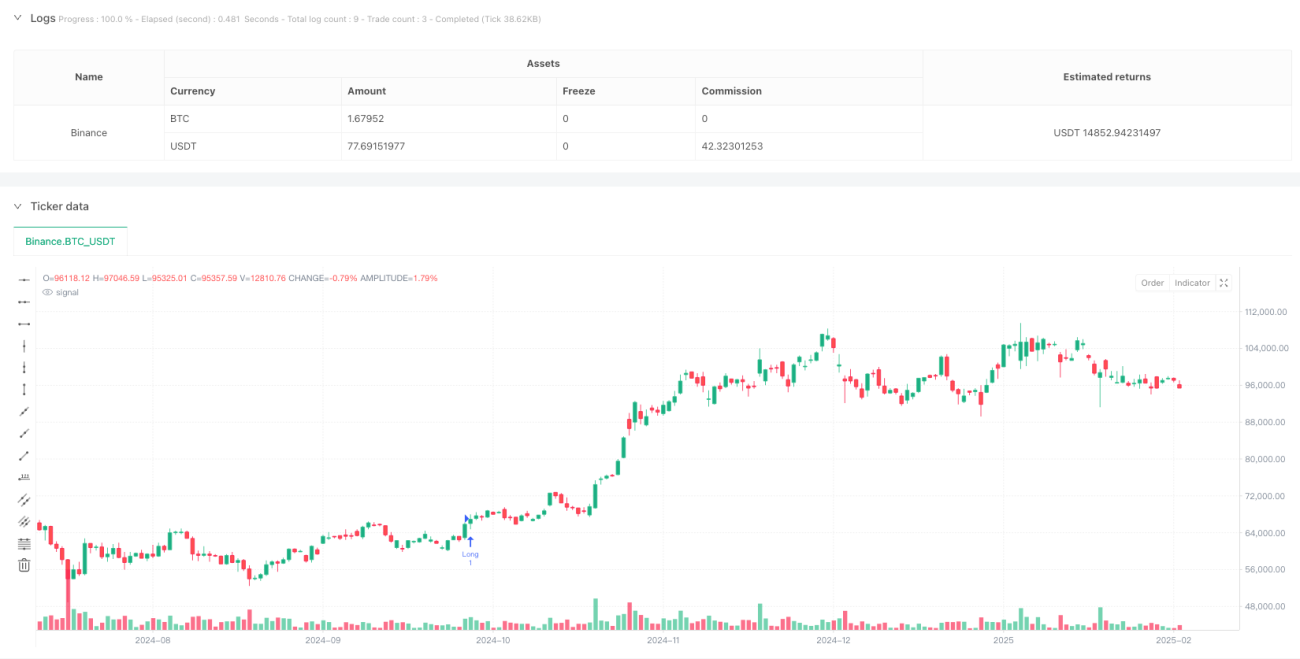

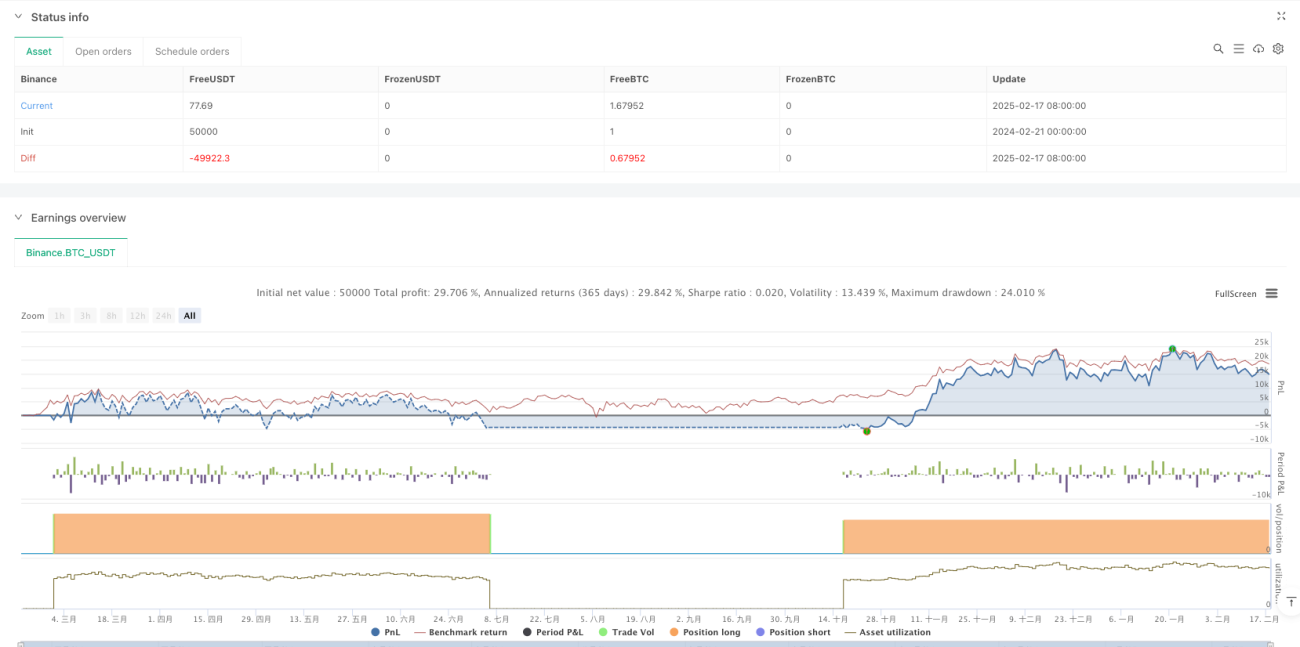

Chiến lược giao dịch động lượng phá vỡ đa xu hướng

Tổng quan

Chiến lược này là một hệ thống theo dõi xu hướng kết hợp nhiều chỉ báo, chủ yếu nắm bắt các cơ hội xu hướng thị trường thông qua việc xác nhận phá vỡ giá, xác nhận khối lượng giao dịch và sự phối hợp của hệ thống đường trung bình động. Chiến lược xác định tín hiệu giao dịch bằng cách theo dõi sự phá vỡ các mức đỉnh/đáy gần đây của giá, sự gia tăng đáng kể của khối lượng giao dịch và sự sắp xếp của nhiều đường trung bình động hàm mũ (EMA). Đồng thời, chiến lược cũng bao gồm một cơ chế nhận diện tích lũy phạm vi hẹp mang tính sáng tạo, được sử dụng để nắm bắt các cơ hội bán khống tiềm năng.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Hệ thống phá vỡ giá: Theo dõi sự phá vỡ của giá so với mức đỉnh/đáy của 20 chu kỳ trước đó.

- Xác nhận khối lượng: Yêu cầu khối lượng giao dịch tại thời điểm phá vỡ ít nhất phải gấp đôi khối lượng giao dịch trung bình của 20 chu kỳ trước đó.

- Hệ thống đường trung bình: Sử dụng các đường EMA chu kỳ 30/50/200 để xây dựng hệ thống xác nhận xu hướng.

- Điều kiện mua (Long): Giá phá vỡ đỉnh mới, khối lượng gia tăng, giá đứng trên đường EMA 200, đường trung bình ngắn hạn nằm trên đường trung bình trung hạn và đường trung bình trung hạn nằm trên đường trung bình dài hạn.

- Điều kiện bán (Short): Bao gồm hai cơ chế vào lệnh:

- Bán khống phá vỡ truyền thống: Giá phá vỡ đáy mới, khối lượng gia tăng, các đường trung bình sắp xếp theo hướng giảm (bearish) và đường EMA 200 dốc xuống.

- Bán khống tích lũy phạm vi hẹp: Giá hình thành tích lũy phạm vi hẹp bên dưới đường trung bình trung hạn, với biên độ tích lũy nhỏ hơn 0.5 lần ATR.

Ưu điểm của chiến lược

- Cơ chế xác nhận đa lớp: Xác nhận ba lớp thông qua phá vỡ giá, khối lượng và đường trung bình, giúp tăng độ tin cậy của tín hiệu.

- Cơ chế bán khống linh hoạt: Cung cấp hai cách vào lệnh bán khống độc lập, gia tăng cơ hội giao dịch.

- Khả năng thích ứng cao: Sử dụng ATR để xác định tích lũy phạm vi hẹp, giúp chiến lược thích ứng với các môi trường biến động thị trường khác nhau.

- Kiểm soát rủi ro hoàn thiện: Sử dụng EMA 200 làm tham chiếu cắt lỗ, cung cấp cơ chế thoát lệnh rõ ràng.

- Tham số có thể điều chỉnh: Các tham số chính đều có thể được tối ưu hóa dựa trên các đặc điểm thị trường khác nhau.

Rủi ro của chiến lược

- Rủi ro phá vỡ giả: Thị trường có thể xảy ra các đợt phá vỡ giả, dẫn đến tín hiệu sai.

- Rủi ro trượt giá: Tại thời điểm phá vỡ với khối lượng giao dịch tăng đột biến, có thể đối mặt với mức trượt giá lớn.

- Rủi ro đảo chiều xu hướng: Trong thị trường có xu hướng mạnh, việc sử dụng cắt lỗ theo đường trung bình có thể dẫn đến thoát lệnh quá sớm.

- Độ nhạy với tham số: Hiệu suất của chiến lược khá nhạy cảm với việc cài đặt tham số, cần tối ưu hóa cẩn thận.

- Phụ thuộc vào môi trường thị trường: Trong thị trường đi ngang (sideways), có thể tạo ra nhiều tín hiệu sai.

Hướng tối ưu hóa chiến lược

- Thêm bộ lọc cường độ xu hướng: Có thể thêm các chỉ báo cường độ xu hướng như ADX để lọc tín hiệu trong môi trường xu hướng yếu.

- Tối ưu hóa cơ chế cắt lỗ: Có thể áp dụng cắt lỗ động dựa trên ATR, tăng tính linh hoạt cho việc cắt lỗ.

- Hoàn thiện quản lý vị thế: Điều chỉnh quy mô vị thế một cách linh hoạt dựa trên cường độ phá vỡ và biến động thị trường.

- Thêm bộ lọc thời gian: Thêm bộ lọc thời gian trong ngày để tránh giao dịch vào các phiên mở cửa và đóng cửa có biến động lớn.

- Phân loại môi trường thị trường: Điều chỉnh linh hoạt các tham số chiến lược dựa trên các môi trường thị trường khác nhau (xu hướng/đi ngang).

Tổng kết

Chiến lược giao dịch động lượng phá vỡ đa xu hướng là một hệ thống theo dõi xu hướng toàn diện. Thông qua việc phối hợp sử dụng nhiều chỉ báo kỹ thuật, nó cung cấp các cơ hội giao dịch linh hoạt đồng thời đảm bảo độ tin cậy của tín hiệu. Điểm sáng tạo của chiến lược nằm ở việc kết hợp các phương pháp giao dịch phá vỡ truyền thống với cơ chế nhận diện tích lũy phạm vi hẹp mới, cho phép nó thích ứng với các môi trường thị trường khác nhau. Mặc dù tồn tại một số rủi ro nhất định, nhưng thông qua việc tối ưu hóa tham số hợp lý và các biện pháp quản lý rủi ro, chiến lược này có tiềm năng đạt được hiệu suất ổn định trong các thị trường có xu hướng.

- 1