Chiến lược dự báo xu hướng đa chu kỳ động kết hợp lọc đường trung bình động

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng kết hợp giữa phân tích kỹ thuật truyền thống và phương pháp trí tuệ nhân tạo hiện đại. Nó chủ yếu sử dụng Đường trung bình động hàm mũ (EMA) và Đường trung bình động đơn giản (SMA) làm bộ lọc xu hướng, đồng thời đưa vào mô hình dự báo để tối ưu hóa thời điểm vào lệnh. Chiến lược được tối ưu hóa riêng cho khung thời gian ngày, nhằm mục đích nắm bắt các xu hướng thị trường trung và dài hạn.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm ba phần chính:

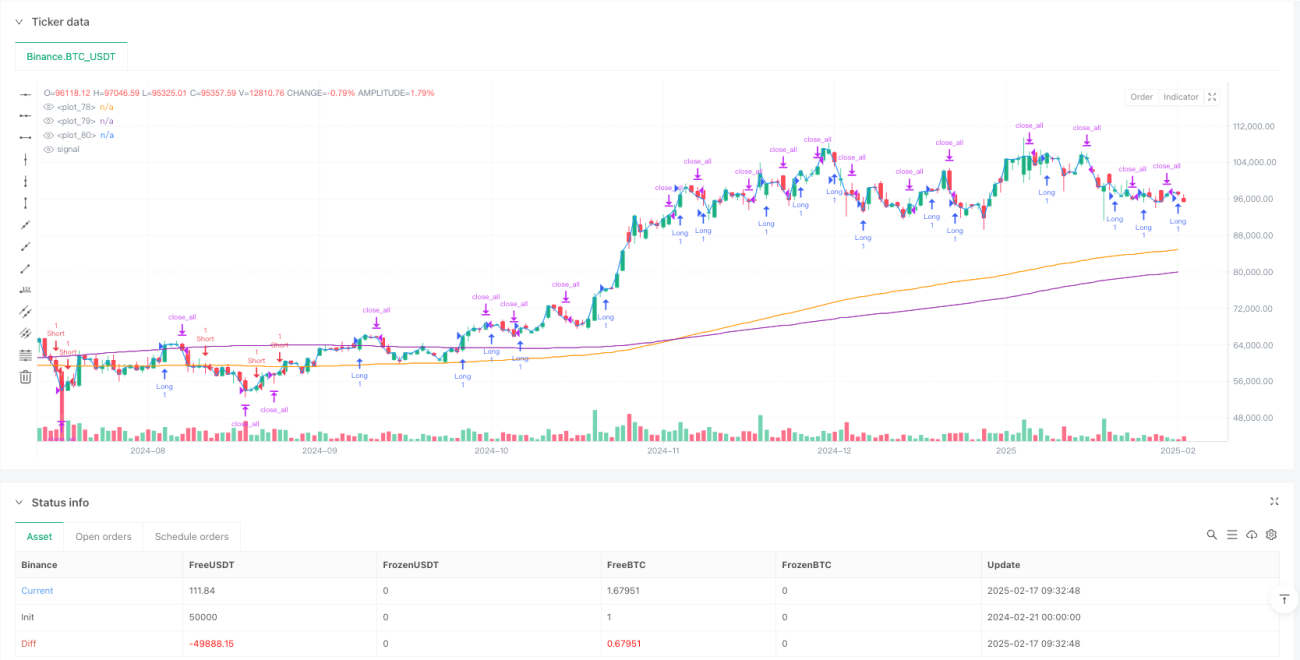

- Hệ thống xác định xu hướng - Sử dụng EMA 200 chu kỳ và SMA 200 chu kỳ làm bộ lọc xu hướng chính, xác định hướng xu hướng hiện tại dựa trên mối quan hệ vị trí giữa giá và đường trung bình.

- Mô-đun dự báo - Sử dụng thành phần dự báo có thể mở rộng, hiện tại sử dụng dự báo mô phỏng, sau này có thể thay thế bằng mô hình học máy.

- Quản lý vị thế - Đặt chu kỳ nắm giữ cố định là 4 nến, dùng để kiểm soát thời gian nắm giữ và rủi ro.

Tín hiệu giao dịch được tạo ra khi có sự đồng nhất giữa hướng xu hướng và tín hiệu dự báo, cụ thể:

- Tín hiệu mua: Giá nằm trên EMA và SMA, đồng thời giá trị dự báo là dương.

- Tín hiệu bán: Giá nằm dưới EMA và SMA, đồng thời giá trị dự báo là âm.

Ưu điểm của chiến lược

- Cấu trúc rõ ràng - Logic chiến lược đơn giản, trực quan, dễ hiểu và dễ bảo trì.

- Rủi ro có thể kiểm soát - Kiểm soát rủi ro hiệu quả thông qua chu kỳ nắm giữ cố định và bộ lọc đường trung bình kép.

- Khả năng mở rộng cao - Mô-đun dự báo được thiết kế linh hoạt, có thể kết nối các mô hình dự báo khác nhau tùy theo nhu cầu.

- Khả năng thích ứng tốt - Các tham số có thể điều chỉnh, thích ứng với các điều kiện thị trường khác nhau.

- Tần suất giao dịch hợp lý - Giao dịch trên khung thời gian ngày giúp giảm chi phí giao dịch và áp lực tâm lý.

Rủi ro của chiến lược

- Rủi ro đảo chiều xu hướng - Có thể xảy ra thua lỗ liên tiếp tại các điểm xoay chiều của xu hướng.

- Độ nhạy tham số - Việc lựa chọn chu kỳ đường trung bình và chu kỳ nắm giữ ảnh hưởng lớn đến hiệu suất chiến lược.

- Phụ thuộc vào mô hình - Độ chính xác của mô-đun dự báo ảnh hưởng trực tiếp đến hiệu quả của chiến lược.

- Ảnh hưởng của trượt giá - Giao dịch trên khung thời gian ngày có thể phải đối mặt với mức trượt giá lớn.

- Phụ thuộc vào điều kiện thị trường - Có thể hoạt động kém hiệu quả trong thị trường đi ngang.

Hướng tối ưu hóa chiến lược

- Nâng cấp mô hình dự báo - Đưa vào mô hình học máy để thay thế dự báo ngẫu nhiên hiện tại.

- Chu kỳ nắm giữ linh hoạt - Điều chỉnh thời gian nắm giữ một cách linh hoạt dựa trên biến động thị trường.

- Tối ưu hóa cắt lỗ - Thêm cơ chế cắt lỗ động để nâng cao khả năng kiểm soát rủi ro.

- Quản lý vị thế - Đưa vào hệ thống quản lý vị thế dựa trên biến động.

- Bộ lọc đa chiều - Thêm các chỉ báo phụ trợ như khối lượng giao dịch, biến động, v.v.

Tổng kết

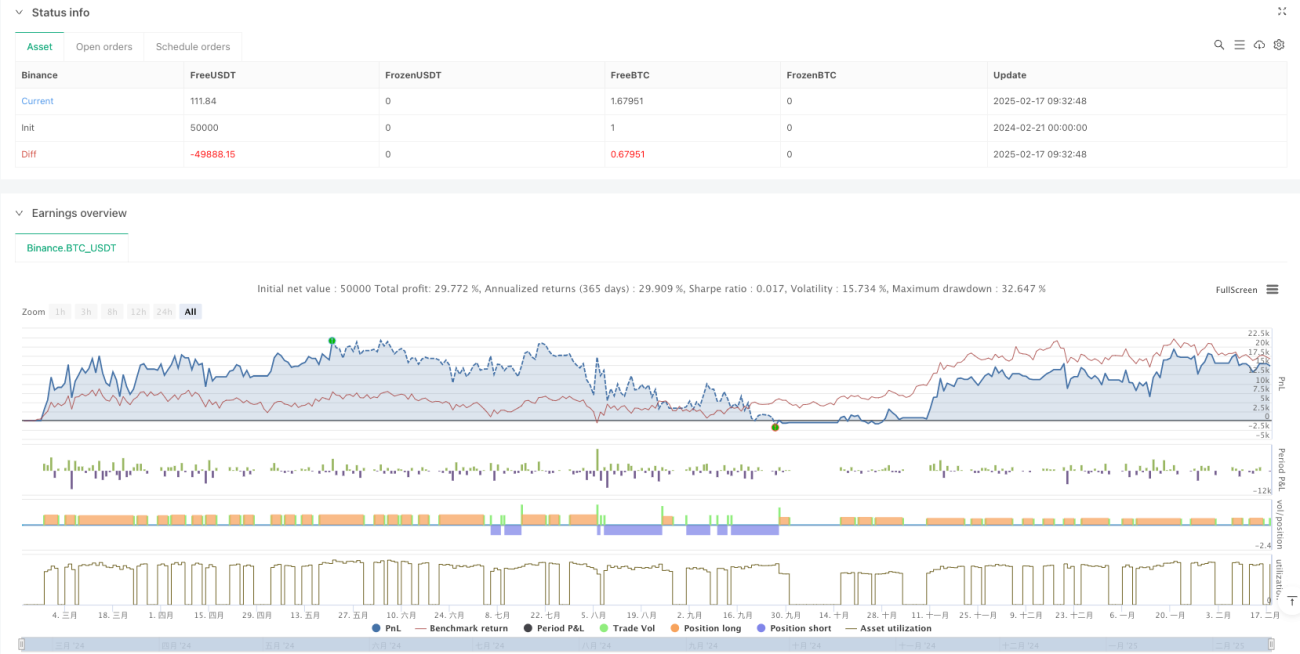

Chiến lược này xây dựng một hệ thống giao dịch theo xu hướng vững chắc bằng cách kết hợp giữa phân tích kỹ thuật truyền thống và phương pháp dự báo hiện đại. Ưu điểm chính của nó là logic rõ ràng, rủi ro có thể kiểm soát và khả năng mở rộng mạnh mẽ. Thông qua việc tối ưu hóa chiến lược, đặc biệt là cải tiến về mô hình dự báo và kiểm soát rủi ro, có thể kỳ vọng nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược. Chiến lược phù hợp cho các nhà đầu tư theo đuổi lợi nhuận ổn định trong trung và dài hạn.

- 1