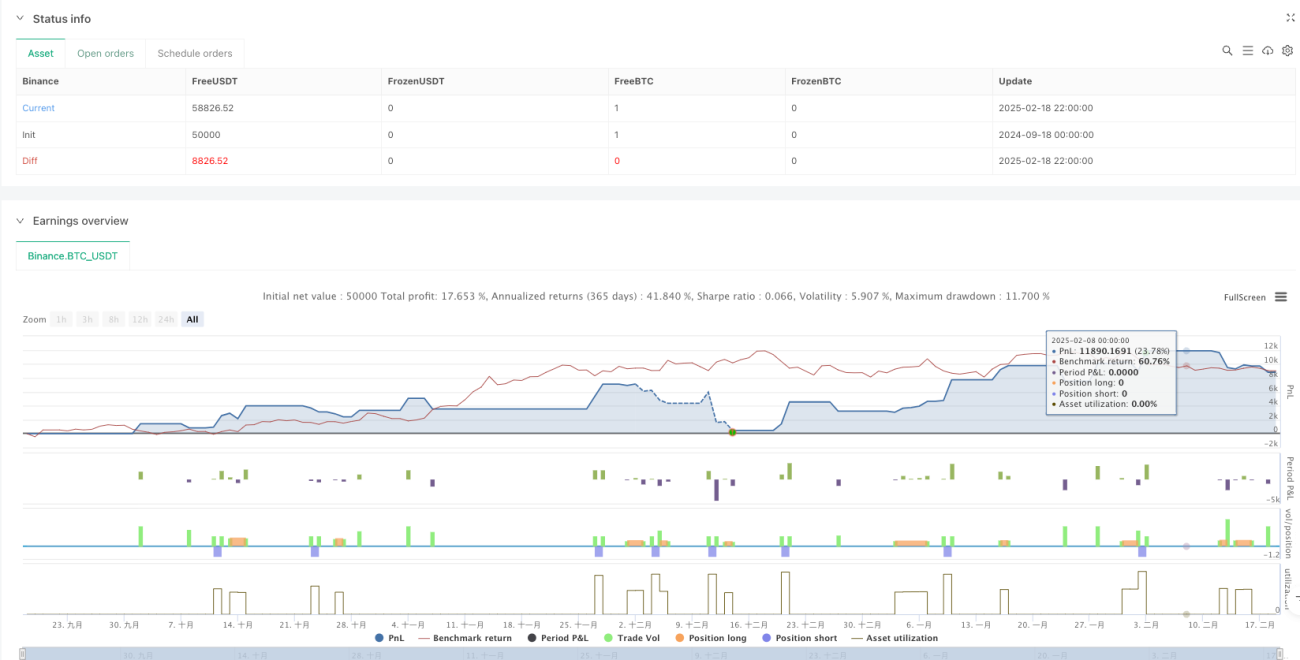

Tổng quan

Chiến lược này là một hệ thống giao dịch kết hợp tín hiệu giao cắt đường trung bình động kép và quản lý rủi ro động. Tín hiệu giao dịch được tạo ra từ sự giao cắt giữa đường trung bình động ngắn hạn và dài hạn, đồng thời sử dụng chỉ báo ATR để điều chỉnh linh hoạt điểm dừng lỗ và chốt lời, kết hợp bộ lọc thời gian và giai đoạn làm mát nhằm tối ưu chất lượng giao dịch. Chiến lược cũng bao gồm cơ chế quản lý tỷ lệ rủi ro/lợi nhuận và phần trăm rủi ro trên mỗi giao dịch.

Nguyên lý chiến lược

Chiến lược dựa trên các thành phần cốt lõi sau:

- Hệ thống tạo tín hiệu sử dụng sự giao cắt của đường trung bình động đơn giản ngắn hạn (10 kỳ) và dài hạn (100 kỳ) để kích hoạt giao dịch. Khi đường trung bình ngắn hạn cắt lên trên đường dài hạn, phát tín hiệu mua; ngược lại phát tín hiệu bán.

- Hệ thống quản lý rủi ro sử dụng ATR 14 kỳ nhân với hệ số 1,5 để thiết lập khoảng cách dừng lỗ động. Mục tiêu lợi nhuận bằng 2 lần khoảng cách dừng lỗ (tỷ lệ rủi ro/lợi nhuận có thể điều chỉnh).

- Bộ lọc thời gian cho phép người dùng thiết lập khung giờ giao dịch cụ thể, chỉ thực hiện giao dịch trong khoảng thời gian đã định.

- Cơ chế thời gian làm mát đặt thời gian chờ 10 kỳ, ngăn chặn giao dịch quá mức.

- Rủi ro mỗi giao dịch được kiểm soát ở mức 1% tài khoản (có thể điều chỉnh).

Ưu điểm chiến lược

- Quản lý rủi ro động: Sử dụng chỉ báo ATR để thích ứng với biến động thị trường, tự động điều chỉnh khoảng cách dừng lỗ và chốt lời trong các môi trường thị trường khác nhau.

- Kiểm soát rủi ro hoàn chỉnh: Thông qua việc thiết lập tỷ lệ rủi ro/lợi nhuận và phần trăm rủi ro mỗi giao dịch, thực hiện quản lý vốn có hệ thống.

- Quản lý thời gian linh hoạt: Có thể điều chỉnh thời gian giao dịch phù hợp với đặc điểm phiên giao dịch của từng thị trường.

- Chống giao dịch quá mức: Cơ chế làm mát giúp tránh tạo quá nhiều tín hiệu giao dịch trong giai đoạn biến động mạnh.

- Hiệu quả trực quan: Hiển thị rõ ràng tín hiệu giao dịch và đường trung bình động trên biểu đồ, thuận tiện cho việc phân tích và tối ưu.

Rủi ro chiến lược

- Rủi ro đảo chiều xu hướng: Trong thị trường đi ngang có thể phát sinh tín hiệu phá vỡ giả, dẫn đến chuỗi dừng lỗ liên tiếp.

- Nhạy cảm với tham số: Việc lựa chọn chu kỳ đường trung bình động, bội số ATR,... ảnh hưởng đáng kể đến hiệu suất chiến lược.

- Thiết lập bộ lọc thời gian không phù hợp có thể bỏ lỡ các cơ hội giao dịch quan trọng.

- Tỷ lệ rủi ro/lợi nhuận cố định có thể không đủ linh hoạt trong các môi trường thị trường khác nhau.

Hướng tối ưu hóa chiến lược

- Thêm bộ lọc cường độ xu hướng: Có thể bổ sung ADX hoặc chỉ báo tương tự để đánh giá cường độ xu hướng, chỉ giao dịch trong xu hướng mạnh.

- Điều chỉnh tỷ lệ rủi ro/lợi nhuận động: Tự động điều chỉnh tỷ lệ rủi ro/lợi nhuận dựa trên biến động thị trường hoặc cường độ xu hướng.

- Tăng cường phân tích khối lượng: Sử dụng khối lượng giao dịch làm chỉ báo xác nhận tín hiệu bổ sung.

- Tối ưu cơ chế làm mát: Điều chỉnh độ dài thời gian làm mát một cách linh hoạt dựa trên biến động thị trường.

- Thêm phân loại môi trường thị trường: Sử dụng các bộ tham số khác nhau trong các điều kiện thị trường khác nhau.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách kết hợp các phương pháp phân tích kỹ thuật cổ điển với khái niệm quản lý rủi ro hiện đại. Ưu điểm cốt lõi nằm ở quản lý rủi ro động và cơ chế lọc đa tầng, tuy nhiên vẫn cần tối ưu tham số dựa trên đặc điểm thị trường cụ thể khi áp dụng thực tế. Sự vận hành thành công của chiến lược đòi hỏi nhà giao dịch phải hiểu sâu vai trò của từng thành phần và điều chỉnh tham số kịp thời theo biến động thị trường. Thông qua các hướng tối ưu được đề xuất, chiến lược có tiềm năng đạt được hiệu suất ổn định hơn trong các môi trường thị trường khác nhau.

/*backtest

start: 2024-09-18 00:00:00

end: 2025-02-19 00:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Profitable Moving Average Crossover Strategy", shorttitle="Profitable MA Crossover", overlay=true)

// Input parameters for the moving averages- 1