Tổng quan

Đây là một chiến lược giao dịch dựa trên phân tích nhiều dải thống kê và xu hướng. Chiến lược kết hợp sử dụng Dải Bollinger, Dải phân vị và Dải luật lũy thừa để xác định các vùng hỗ trợ/kháng cự chính, đồng thời sử dụng đường độ lệch chuẩn dưới của dải phân vị trên làm tín hiệu kích hoạt để xác định thời điểm vào và thoát lệnh. Chiến lược được thiết kế có tính đến biến động thị trường, nâng cao độ tin cậy của tín hiệu thông qua sự chồng lấp của nhiều phương pháp thống kê.

Nguyên lý chiến lược

Nguyên lý cốt lõi của chiến lược là nắm bắt xu hướng thị trường thông qua sự giao nhau của nhiều dải thống kê. Bao gồm các thành phần chính sau:

- Hệ thống Dải Bollinger – Dùng để đánh giá phạm vi biến động giá; khi giá phá vỡ dải trên sẽ chuyển sang cảnh báo màu vàng.

- Hệ thống Dải phân vị – Tính toán phân vị trên và dưới của giá, dùng để đánh giá xác suất giá ở mức cực trị.

- Hệ thống Dải luật lũy thừa – Tính mức ý nghĩa dựa trên lợi nhuận lịch sử, dùng để đo lường tình trạng quá mua/quá bán.

- Hệ thống kích hoạt – Sử dụng đường độ lệch chuẩn dưới của dải phân vị trên làm tín hiệu kích hoạt chính; giá duy trì trên đường này được coi là tín hiệu tăng giá.

- Hệ thống xác nhận – Thiết lập số nến xác nhận liên tiếp để lọc tín hiệu nhiễu.

Ưu điểm của chiến lược

- Độ ổn định tín hiệu cao – Việc sử dụng chồng lấp nhiều dải thống kê giúp giảm hiệu quả các tín hiệu nhiễu.

- Khả năng thích ứng tốt – Chiến lược có thể thích ứng với các khung thời gian và điều kiện thị trường khác nhau.

- Kiểm soát rủi ro hoàn thiện – Phân chia vùng rủi ro thông qua nhiều dải thống kê, đồng thời có cơ chế cắt lỗ.

- Linh hoạt về tham số – Cung cấp nhiều tùy chọn tham số, có thể tối ưu hóa theo đặc điểm thị trường khác nhau.

- Trực quan hóa rõ ràng – Màu sắc các đường chỉ báo khác biệt rõ rệt, tín hiệu giao dịch trực quan.

Rủi ro của chiến lược

- Rủi ro độ trễ – Các chỉ báo thống kê đều có độ trễ nhất định, có thể bỏ lỡ điểm vào tối ưu.

- Bất lợi trong thị trường đi ngang – Có thể tạo ra quá nhiều tín hiệu giao dịch trong thị trường dao động ngang.

- Nhạy cảm với tham số – Hiệu quả của các tổ hợp tham số khác nhau chênh lệch lớn, cần tối ưu hóa nhiều lần.

- Tải tính toán lớn – Việc tính toán thời gian thực nhiều chỉ báo thống kê đòi hỏi tài nguyên tính toán đáng kể.

- Phụ thuộc vào môi trường thị trường – Trong điều kiện thị trường cực đoan, quy luật thống kê có thể mất hiệu lực.

Hướng tối ưu hóa chiến lược

- Áp dụng tham số động – Tự động điều chỉnh các tham số theo biến động thị trường.

- Bổ sung đánh giá môi trường thị trường – Thêm chỉ báo cường độ xu hướng để lọc tín hiệu trong thị trường đi ngang.

- Tối ưu hiệu suất tính toán – Đơn giản hóa một số quy trình tính toán, giảm mức sử dụng tài nguyên.

- Hoàn thiện kiểm soát rủi ro – Thêm nhiều điều kiện cắt lỗ và chiến lược quản lý vị thế.

- Tăng cường khả năng thích ứng – Phát triển hệ thống tối ưu hóa tham số thích ứng.

Tổng kết

Đây là một chiến lược theo dõi xu hướng tổng hợp kết hợp nhiều phương pháp thống kê. Nhờ sự phối hợp của Dải Bollinger, Dải phân vị và Dải luật lũy thừa, chiến lược có thể nắm bắt tốt xu hướng thị trường, đồng thời có khả năng kiểm soát rủi ro tốt. Mặc dù tồn tại một số độ trễ và khó khăn trong việc tối ưu hóa tham số, nhưng thông qua cải tiến và tối ưu hóa liên tục, chiến lược này có giá trị thực tiễn và triển vọng phát triển tốt.

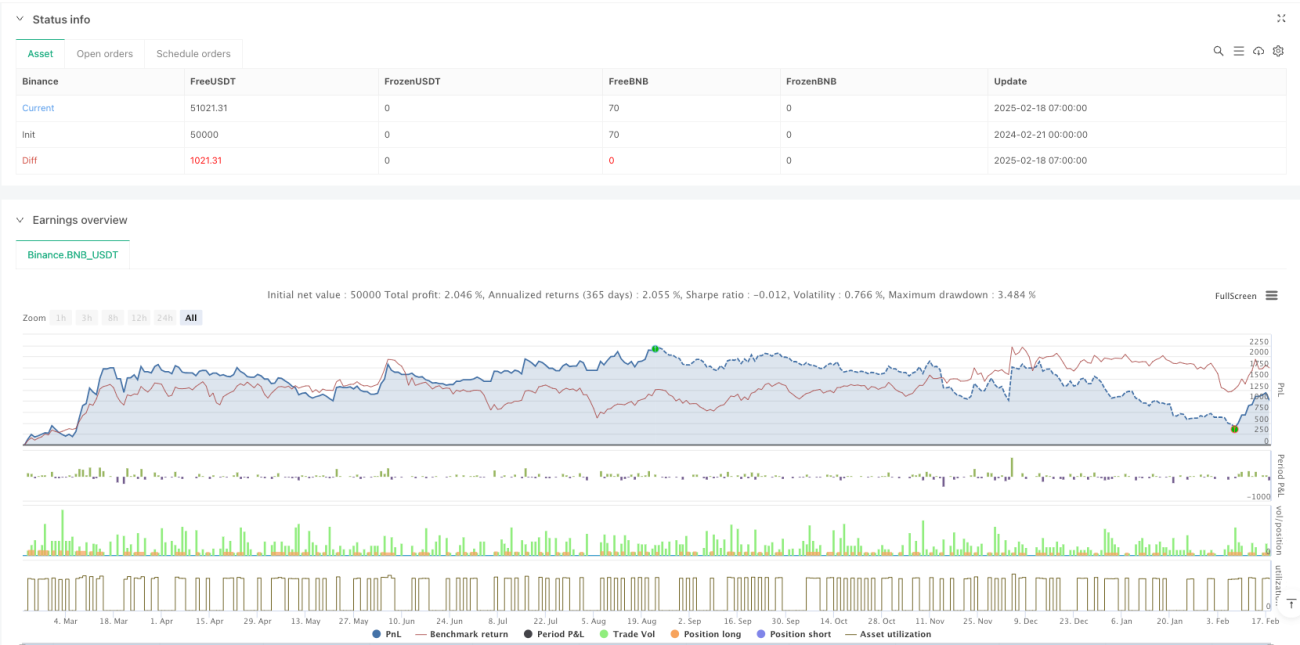

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=6

strategy("Multi-Band Comparison Strategy with Separate Entry/Exit Confirmation", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

initial_capital=5000, currency=currency.USD)- 1