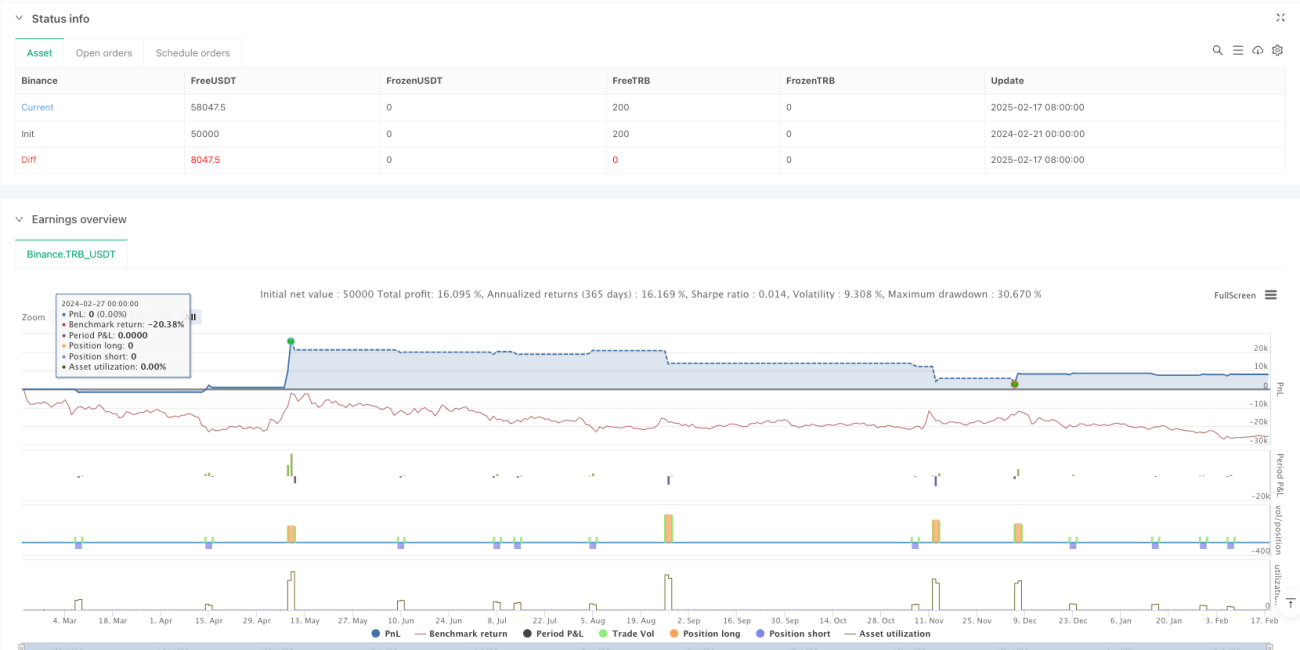

Tổng quan

Chiến lược này là một hệ thống giao dịch dựa trên phá vỡ giá và dừng lỗ động. Bằng cách theo dõi giá cao nhất và giá thấp nhất trong N chu kỳ trước đó, nó thực hiện giao dịch khi giá phá vỡ các mức quan trọng này. Chiến lược sử dụng cơ chế dừng lỗ thông minh, chỉ kích hoạt dừng lỗ động sau khi đạt lợi nhuận 1%, cho phép lợi nhuận phát triển đầy đủ. Đồng thời, thiết lập thời gian nghỉ 1 giờ để tránh giao dịch quá mức, nâng cao chất lượng mỗi giao dịch.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm các phần chính sau:

- Tín hiệu vào lệnh: Tính giá cao nhất và thấp nhất trong N chu kỳ trước, kích hoạt tín hiệu giao dịch khi giá hiện tại phá vỡ các mức này. Vào lệnh mua yêu cầu giá phá vỡ đỉnh trước đó một tỷ lệ phần trăm nhất định, bán khống thì cần phá vỡ đáy trước đó.

- Quản lý giao dịch: Áp dụng thời gian nghỉ giao dịch 1 giờ để tránh giao dịch thường xuyên khi biến động mạnh.

- Kiểm soát rủi ro: Sử dụng dừng lỗ động, chỉ kích hoạt sau khi đạt lợi nhuận 1%, giúp bảo vệ lợi nhuận tốt hơn.

- Tối ưu hóa tham số: Các tham số quan trọng như chu kỳ xem lại, ngưỡng phá vỡ, tỷ lệ dừng lỗ... có thể được điều chỉnh theo các điều kiện thị trường khác nhau.

Lợi thế của chiến lược

- Quản lý rủi ro động: Thông qua cơ chế dừng lỗ động, chiến lược có thể bảo vệ lợi nhuận đồng thời cho phép lợi nhuận tiếp tục tăng trưởng.

- Linh hoạt thích ứng: Chiến lược có thể thích ứng với các điều kiện thị trường khác nhau bằng cách điều chỉnh tham số để tối ưu hóa hiệu suất.

- Cơ chế lọc: Sử dụng thời gian nghỉ giao dịch để tránh giao dịch quá mức, nâng cao chất lượng giao dịch.

- Đơn giản và hiệu quả: Logic chiến lược rõ ràng, dễ hiểu và thực hiện, đồng thời duy trì khả năng mở rộng tốt.

Rủi ro của chiến lược

- Rủi ro phá vỡ giả: Thị trường có thể xuất hiện phá vỡ giả, dẫn đến tín hiệu sai. Khuyến nghị thêm xác nhận khối lượng giao dịch.

- Ảnh hưởng trượt giá: Trong thời gian biến động cao, có thể đối mặt với trượt giá lớn, ảnh hưởng đến hiệu suất chiến lược.

- Nhạy cảm tham số: Hiệu suất chiến lược khá nhạy cảm với cài đặt tham số, cần tối ưu hóa cẩn thận.

- Phụ thuộc môi trường thị trường: Có thể hoạt động kém trong môi trường biến động thấp.

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo khối lượng: Sử dụng xác nhận khối lượng giao dịch để tăng độ tin cậy của tín hiệu phá vỡ.

- Thêm bộ lọc xu hướng: Kết hợp chỉ báo xu hướng dài hạn, chỉ giao dịch theo hướng xu hướng.

- Điều chỉnh tham số động: Tự động điều chỉnh ngưỡng phá vỡ và tham số dừng lỗ theo biến động thị trường.

- Khung thời gian đa dạng: Tích hợp tín hiệu từ nhiều khung thời gian để nâng cao độ chính xác.

Tổng kết

Đây là một chiến lược theo xu hướng được thiết kế hợp lý, kết hợp phá vỡ giá và dừng lỗ động, vừa có thể bắt kịp xu hướng lớn vừa kiểm soát rủi ro hiệu quả. Chiến lược có khả năng tùy chỉnh cao, có thể thích ứng với các môi trường thị trường khác nhau thông qua tối ưu hóa tham số. Khuyến nghị bắt đầu với khối lượng nhỏ trong giao dịch thực tế, từ từ xác minh hiệu suất của chiến lược trong các điều kiện thị trường khác nhau.

- 1