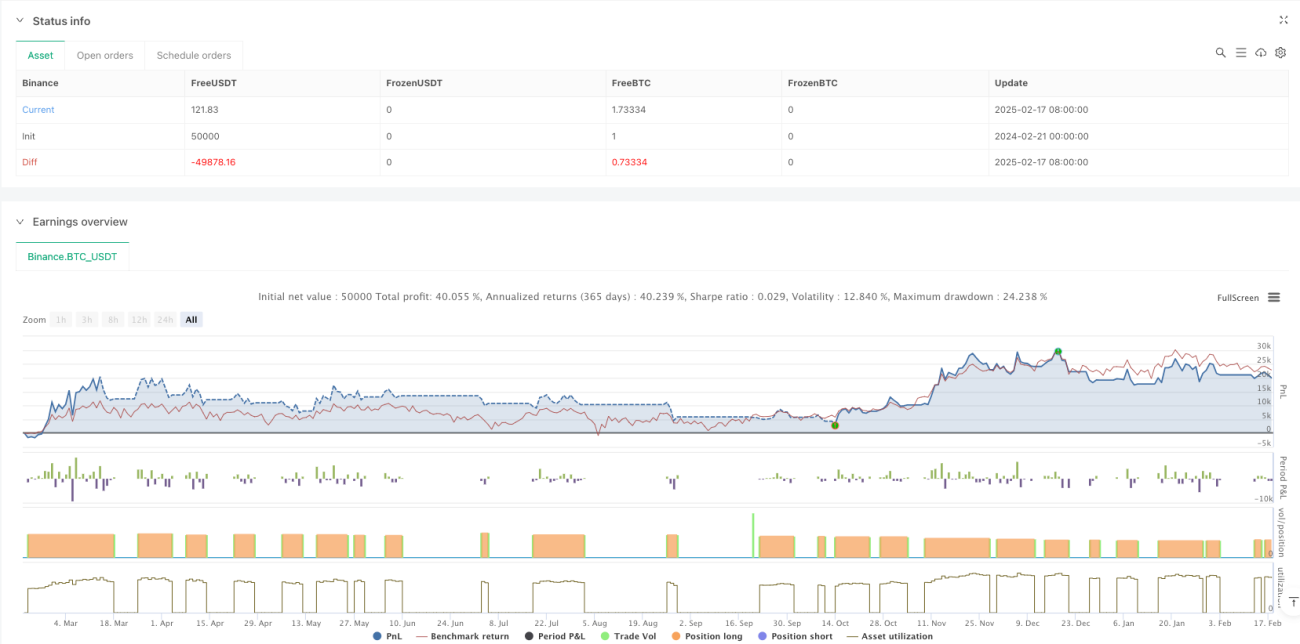

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng dựa trên phân tích đa khung thời gian, kết hợp đường EMA trên khung tuần và ngày cùng với chỉ báo RSI để nhận diện xu hướng thị trường và động lượng. Chiến lược xác định cơ hội giao dịch dựa trên sự đồng nhất xu hướng giữa các khung thời gian và sử dụng lệnh dừng lỗ động dựa trên ATR để quản lý rủi ro. Hệ thống áp dụng mô hình quản lý vốn, sử dụng 100% tài khoản cho mỗi giao dịch và tính phí giao dịch 0,1%.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Sử dụng EMA khung tuần làm bộ lọc xu hướng chính, kết hợp giá đóng cửa khung ngày với EMA khung tuần để xác định trạng thái thị trường

- Điều chỉnh ngưỡng xác định xu hướng một cách linh hoạt thông qua chỉ báo ATR, tăng khả năng thích ứng của chiến lược

- Tích hợp chỉ báo động lượng RSI làm điều kiện lọc giao dịch bổ sung

- Sử dụng hệ thống trailing stop dựa trên mức giá thấp nhất 7 ngày và ATR

- Khi xuất hiện tín hiệu cảnh báo tăng giá quá mức, chiến lược sẽ tạm dừng mở vị thế để tránh rủi ro

Lợi thế của chiến lược

- Phân tích đa khung thời gian cung cấp góc nhìn thị trường toàn diện hơn, giúp lọc hiệu quả các tín hiệu phá vỡ giả

- Cơ chế dừng lỗ động tự điều chỉnh theo biến động thị trường, mang lại kiểm soát rủi ro linh hoạt

- Bộ lọc động lượng RSI giúp xác nhận sức mạnh xu hướng, nâng cao chất lượng điểm vào lệnh

- Hệ thống bao gồm cơ chế cảnh báo tăng giá quá mức, giúp giảm thiểu rủi ro sụt giảm

- Các tham số của chiến lược có khả năng điều chỉnh cao, dễ dàng tối ưu hóa theo các điều kiện thị trường khác nhau

Rủi ro của chiến lược

- Trong thị trường đi ngang có thể vào lệnh thường xuyên, làm tăng chi phí giao dịch

- Sử dụng 100% vốn để giao dịch tiềm ẩn rủi ro sụt giảm lớn

- Phụ thuộc vào chỉ báo kỹ thuật có thể phản ứng chậm khi xảy ra sự kiện bất ngờ trên thị trường

- Phân tích đa khung thời gian có thể xuất hiện tín hiệu mâu thuẫn giữa các cấp độ

- Trailing stop có thể bị kích hoạt quá sớm trong điều kiện biến động mạnh

Hướng tối ưu hóa chiến lược

- Đưa vào bộ lọc biến động, giảm tần suất giao dịch trong thời kỳ biến động thấp

- Thêm hệ thống quản lý vị thế, điều chỉnh tỷ lệ nắm giữ linh hoạt theo trạng thái thị trường

- Tích hợp các chỉ báo cơ bản, cung cấp thêm đánh giá môi trường thị trường

- Tối ưu hóa tham số trailing stop để thích ứng tốt hơn với các giai đoạn thị trường khác nhau

- Thêm phân tích khối lượng giao dịch, nâng cao độ chính xác trong nhận định xu hướng

Tổng kết

Đây là một chiến lược theo xu hướng có cấu trúc hoàn chỉnh và logic rõ ràng. Thông qua phân tích đa khung thời gian và các bộ lọc chỉ báo động, chiến lược có thể nắm bắt tốt các xu hướng chính. Mặc dù tồn tại một số rủi ro cố hữu, nhưng thông qua tối ưu hóa tham số và bổ sung các chỉ báo phụ trợ, chiến lược vẫn còn nhiều dư địa cải thiện. Khuyến nghị tiến hành backtest đầy đủ trước khi giao dịch thực tế và điều chỉnh cài đặt tham số theo môi trường thị trường cụ thể.

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

// @version=6

strategy("Bitcoin Regime Filter Strategy", // Strategy name

overlay=true, // The strategy will be drawn directly on the price chart

initial_capital=10000, // Initial capital of 10000 USD- 1