Chiến lược tăng vị thế hồi quy giao cắt RSI đa cấp độ

Tổng quan

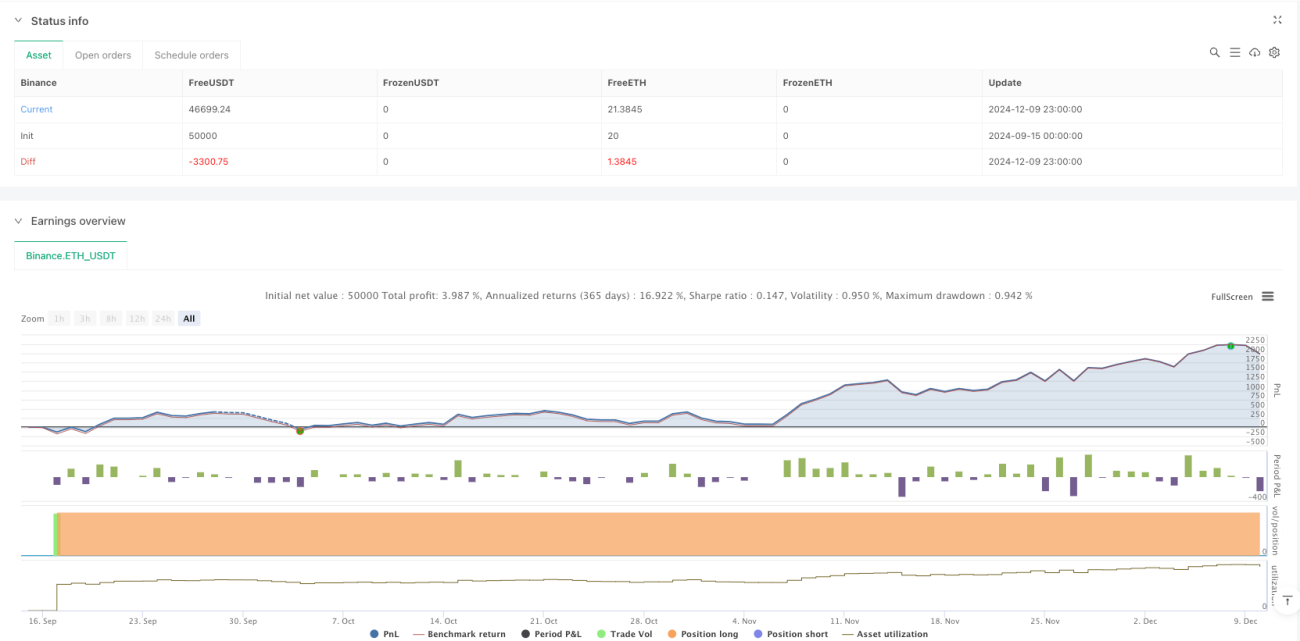

Chiến lược này là một hệ thống giao dịch tự động dựa trên Chỉ số sức mạnh tương đối (RSI), chủ yếu nhận diện các cơ hội phục hồi tiềm năng thông qua việc xác định điều kiện quá bán của thị trường. Chiến lược sử dụng phương pháp xây dựng vị thế theo cấp độ, thiết lập dần nhiều vị thế khi RSI cắt xuống dưới mức thấp và kiểm soát rủi ro thông qua việc đặt mục tiêu lợi nhuận. Hệ thống được thiết kế với cơ chế quản lý vốn linh hoạt, mỗi lần giao dịch sử dụng 6,6% tổng tài khoản, cho phép tối đa 15 lần tích lũy theo kiểu kim tự tháp.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Tín hiệu vào lệnh: Kích hoạt tín hiệu mua khi chỉ báo RSI chu kỳ 14 cắt xuống dưới mức quá bán 28,5

- Quản lý vị thế: Mỗi lần mở vị thế sử dụng 6,6% vốn tài khoản, tối đa cho phép 15 lần xây dựng vị thế theo cấp độ

- Chốt lời: Khi giá đạt mức tăng 900% so với giá trung bình của vị thế, đóng 50% vị thế đang nắm giữ

- Hiển thị trực quan: Đánh dấu tín hiệu mua bán, đường RSI, giá vào lệnh và giá mục tiêu trên biểu đồ

Chiến lược đánh giá xu hướng thị trường bằng cách quan sát biểu hiện của chỉ báo RSI trong vùng quá bán, khi xuất hiện tín hiệu quá bán sẽ xây dựng vị thế dần dần nhằm giảm chi phí xây dựng vị thế.

Ưu điểm của chiến lược

- Xây dựng vị thế có hệ thống: Tự động nhận diện cơ hội giao dịch thông qua các tham số RSI đã định sẵn, tránh sai lệch chủ quan do phán đoán của con người

- Phân tán rủi ro: Sử dụng phương pháp xây dựng vị thế theo cấp độ, thiết lập nhiều vị thế ở các mức giá khác nhau, phân tán rủi ro hiệu quả

- Linh hoạt thích ứng: Các tham số chiến lược có thể điều chỉnh theo các môi trường thị trường khác nhau và mức độ chấp nhận rủi ro cá nhân

- Bảo vệ lợi nhuận: Thiết lập mục tiêu lợi nhuận rõ ràng, tự động giảm vị thế khi đạt mục tiêu, khóa một phần lợi nhuận

- Hiệu quả vốn: Nâng cao hiệu quả sử dụng vốn thông qua kiểm soát vị thế hợp lý và cơ chế tích lũy

Rủi ro của chiến lược

- Rủi ro xu hướng: Trong xu hướng giảm mạnh, tín hiệu xây dựng vị thế có thể kích hoạt thường xuyên, dẫn đến thua lỗ vốn

- Nhạy cảm với tham số: Cài đặt tham số RSI, tỷ lệ xây dựng vị thế không phù hợp có thể ảnh hưởng đến hiệu suất chiến lược

- Thanh khoản thị trường: Trong thị trường thiếu thanh khoản, khó hoàn thành giao dịch ở mức giá mục tiêu

- Quản lý vốn: Tích lũy quá mức có thể dẫn đến mức độ rủi ro quá lớn

Giải pháp:

- Bổ sung bộ lọc xu hướng, tạm dừng xây dựng vị thế trong xu hướng giảm rõ ràng

- Tối ưu hóa cài đặt tham số thông qua backtest

- Thiết lập giới hạn drawdown tối đa

- Điều chỉnh linh hoạt ngưỡng tích lũy

Hướng tối ưu hóa chiến lược

- Tham số động: Tự động điều chỉnh tham số RSI và điều kiện xây dựng vị thế dựa trên biến động thị trường

- Cơ chế dừng lỗ: Bổ sung chức năng trailing stop, kiểm soát rủi ro tốt hơn

- Bộ lọc thị trường: Thêm các điều kiện lọc như khối lượng, xu hướng, nâng cao chất lượng tín hiệu

- Tối ưu hóa thoát lệnh: Thiết kế cơ chế chốt lời linh hoạt hơn, như giảm vị thế theo từng phần

- Kiểm soát rủi ro: Tăng giới hạn drawdown tối đa và kiểm soát mức độ rủi ro

Tổng kết

Chiến lược này nhận diện cơ hội quá bán thông qua chỉ báo RSI, kết hợp tích lũy kiểu kim tự tháp và chốt lời theo tỷ lệ cố định để xây dựng một hệ thống giao dịch hoàn chỉnh. Ưu điểm của chiến lược nằm ở vận hành có hệ thống và phân tán rủi ro, nhưng cần chú ý đến ảnh hưởng của xu hướng thị trường và cài đặt tham số đến hiệu suất. Bằng cách bổ sung các biện pháp tối ưu hóa như điều chỉnh tham số động, cơ chế dừng lỗ và bộ lọc thị trường, có thể nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược.

/*backtest

start: 2024-09-15 00:00:00

end: 2024-12-10 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("RSI Cross Under Strategy", overlay=true, initial_capital=1500, default_qty_type=strategy.percent_of_equity, default_qty_value=6.6)

// Input parameters- 1