Chiến lược giao dịch tích hợp đa chiều dựa trên Nadaraya-Watson

Tổng quan

Chiến lược này là một hệ thống giao dịch đa chiều dựa trên hồi quy hạt nhân Nadaraya-Watson, tích hợp thông tin thị trường từ bốn chiều: kỹ thuật, tâm lý, siêu cảm và ý định, để hình thành tín hiệu tổng hợp nhằm đưa ra quyết định giao dịch. Chiến lược áp dụng phương pháp tối ưu hóa trọng số, xử lý có trọng số các tín hiệu từ các chiều khác nhau, đồng thời kết hợp các bộ lọc xu hướng và động lượng để nâng cao chất lượng tín hiệu. Hệ thống còn bao gồm mô-đun quản lý rủi ro hoàn chỉnh, bảo vệ vốn thông qua cắt lỗ và chốt lời.

Nguyên lý chiến lược

Cốt lõi của chiến lược là sử dụng phương pháp hồi quy hạt nhân Nadaraya-Watson để làm mịn dữ liệu thị trường từ nhiều chiều. Cụ thể:

- Chiều kỹ thuật sử dụng giá đóng cửa

- Chiều tâm lý sử dụng chỉ báo RSI

- Chiều siêu cảm sử dụng độ biến động ATR

- Chiều ý định sử dụng độ lệch giá so với đường trung bình

Các chiều này sau khi được làm mịn bằng hồi quy hạt nhân, sẽ được tích hợp có trọng số thông qua trọng số định trước (kỹ thuật 0.4, tâm lý 0.2, siêu cảm 0.2, ý định 0.2) để tạo thành tín hiệu giao dịch cuối cùng. Khi tín hiệu tổng hợp cắt đường trung bình động của nó, kết hợp với xác nhận từ bộ lọc xu hướng và động lượng, lệnh giao dịch sẽ được phát ra.

Ưu điểm của chiến lược

- Phân tích đa chiều mang lại góc nhìn thị trường toàn diện hơn, tránh hạn chế của các chỉ báo đơn lẻ

- Hồi quy hạt nhân Nadaraya-Watson giúp giảm nhiễu thị trường hiệu quả, cung cấp tín hiệu mượt mà hơn

- Cơ chế tối ưu hóa trọng số cho phép điều chỉnh tầm quan trọng của từng chiều dựa trên đặc điểm thị trường

- Việc bổ sung bộ lọc xu hướng và động lượng cải thiện đáng kể chất lượng tín hiệu

- Hệ thống quản lý rủi ro hoàn chỉnh đảm bảo an toàn vốn

Rủi ro của chiến lược

- Tối ưu hóa tham số quá mức có thể dẫn đến overfitting

- Nhiều điều kiện lọc có thể bỏ lỡ một phần tín hiệu hiệu quả

- Độ phức tạp tính toán của hồi quy hạt nhân cao, có thể ảnh hưởng đến hiệu suất thời gian thực

- Phân bổ trọng số không phù hợp có thể làm suy yếu một số tín hiệu thị trường quan trọng

Các biện pháp giảm thiểu bao gồm: sử dụng kiểm tra ngoài mẫu để xác thực tham số, điều chỉnh động điều kiện lọc, tối ưu hóa hiệu quả tính toán, định kỳ đánh giá và điều chỉnh phân bổ trọng số.

Hướng tối ưu hóa chiến lược

- Giới thiệu hệ thống trọng số thích ứng, điều chỉnh động trọng số các chiều theo trạng thái thị trường

- Phát triển cơ chế lọc thông minh hơn, cân bằng giữa chất lượng và số lượng tín hiệu

- Tối ưu hóa thuật toán Nadaraya-Watson, nâng cao hiệu quả tính toán

- Thêm mô-đun nhận diện chu kỳ thị trường, sử dụng các thiết lập tham số khác nhau ở các giai đoạn thị trường khác nhau

- Mở rộng hệ thống quản lý rủi ro, bổ sung chức năng cắt lỗ động và quản lý vị thế

Tổng kết

Đây là một chiến lược sáng tạo kết hợp phương pháp toán học với trí tuệ giao dịch. Thông qua phân tích đa chiều và các công cụ toán học tiên tiến, chiến lược có thể nắm bắt nhiều khía cạnh của thị trường, cung cấp các tín hiệu giao dịch tương đối đáng tin cậy. Mặc dù còn một số không gian tối ưu, nhưng khung tổng thể của chiến lược là vững chắc và có giá trị ứng dụng thực tế.

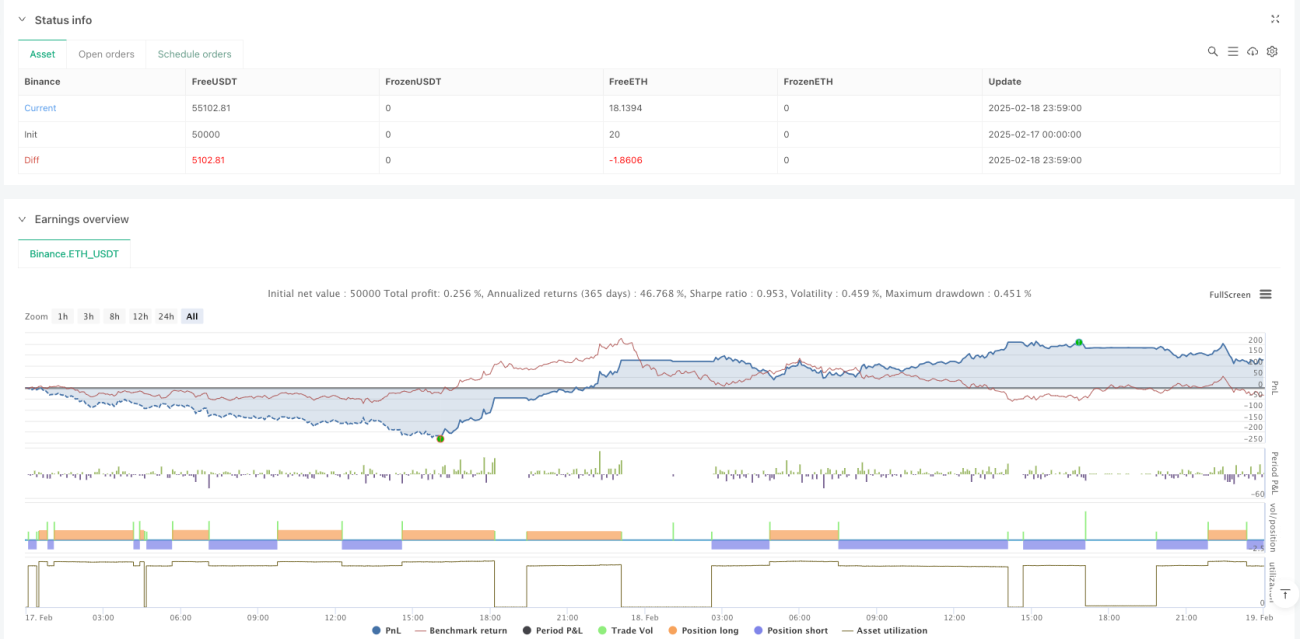

/*backtest

start: 2025-02-17 00:00:00

end: 2025-02-19 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced Multidimensional Integration Strategy with Nadaraya", overlay=true, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

//────────────────────────────────────────────────────────────────────────────- 1