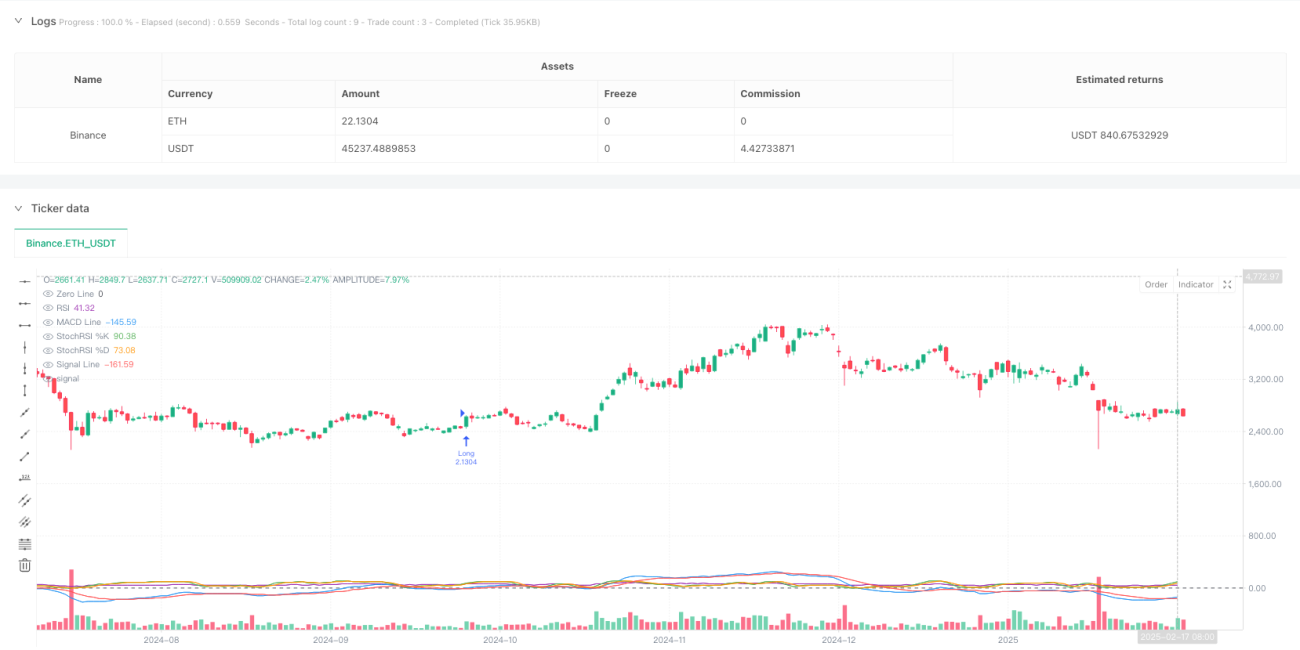

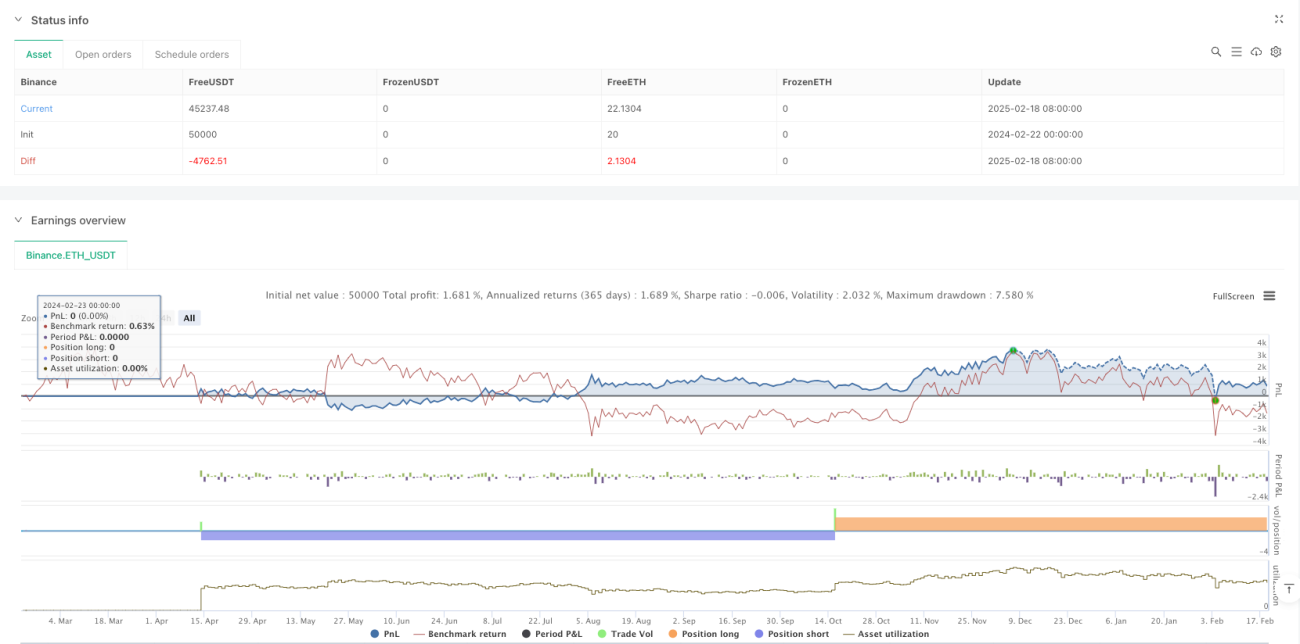

Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng kết hợp nhiều chỉ báo kỹ thuật. Nó sử dụng MACD để nắm bắt động lượng xu hướng, dùng RSI và StochRSI để xác nhận trạng thái quá mua/quá bán, và tận dụng chỉ báo khối lượng để xác thực tính hiệu quả của tín hiệu giao dịch. Chiến lược áp dụng cơ chế ngưỡng khối lượng động, đảm bảo chỉ thực hiện giao dịch khi thị trường có đủ thanh khoản.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các yếu tố chính sau:

- Chỉ báo MACD được sử dụng để nhận diện sự thay đổi xu hướng và động lượng giá, tạo tín hiệu giao dịch ban đầu thông qua sự giao cắt giữa đường nhanh và đường chậm.

- Chỉ báo RSI đóng vai trò công cụ xác nhận xu hướng, giúp đánh giá thị trường đang ở trạng thái mạnh (>50) hay yếu (<50).

- StochRSI cung cấp thông tin động lượng thị trường nhạy hơn thông qua tính toán chỉ báo ngẫu nhiên trên RSI.

- Cơ chế xác thực khối lượng yêu cầu khối lượng giao dịch tại thời điểm phát sinh tín hiệu phải cao hơn 1,5 lần khối lượng trung bình 14 kỳ.

Hệ thống mở vị thế mua khi đáp ứng các điều kiện sau:

- Đường nhanh MACD cắt lên trên đường chậm.

- RSI nằm trên 50.

- Đường K của StochRSI cắt lên trên đường D.

- Khối lượng hiện tại cao hơn ngưỡng.

Hệ thống mở vị thế bán khi đáp ứng các điều kiện sau:

- Đường nhanh MACD cắt xuống dưới đường chậm.

- RSI nằm dưới 50.

- Đường K của StochRSI cắt xuống dưới đường D.

- Khối lượng hiện tại cao hơn ngưỡng.

Ưu điểm chiến lược

- Sự kết hợp của nhiều chỉ báo kỹ thuật cung cấp tín hiệu giao dịch đáng tin cậy hơn, giảm rủi ro tín hiệu giả.

- Cơ chế xác nhận khối lượng lọc hiệu quả các cơ hội giao dịch có thanh khoản thị trường không đủ.

- Các tham số chiến lược có tính điều chỉnh cao, dễ dàng tối ưu hóa theo các môi trường thị trường khác nhau.

- Sự kết hợp giữa chiến lược theo xu hướng và động lượng giúp vừa bắt được xu hướng lớn, vừa không bỏ lỡ cơ hội ngắn hạn.

- Logic vào lệnh rõ ràng, dễ thực hiện và kiểm chứng qua backtest.

Rủi ro chiến lược

- Việc lọc qua nhiều chỉ báo có thể dẫn đến bỏ lỡ một số cơ hội giao dịch tiềm năng.

- Trong thị trường dao động ngang (sideways) có thể tạo ra nhiều tín hiệu phá vỡ giả.

- Không có cơ chế cắt lỗ và chốt lời, làm tăng rủi ro quản lý vốn.

- Phụ thuộc vào khối lượng lịch sử làm tham chiếu, có thể mất hiệu quả trong các điều kiện thị trường bất thường.

- Độ trễ của nhiều chỉ báo kỹ thuật cộng dồn có thể khiến thời điểm vào lệnh bị chậm.

Khuyến nghị kiểm soát rủi ro:

- Thêm cơ chế cắt lỗ và chốt lời.

- Đưa vào bộ lọc xu hướng.

- Tối ưu hóa tổ hợp tham số chỉ báo.

- Đặt giới hạn thời gian nắm giữ tối đa.

- Thực hiện chiến lược xây dựng vị thế theo từng phần.

Hướng tối ưu hóa chiến lược

- Đưa vào cơ chế tối ưu hóa tham số thích ứng, giúp chiến lược tự động điều chỉnh tham số chỉ báo theo trạng thái thị trường.

- Thêm bộ lọc biến động thị trường, áp dụng quy tắc giao dịch khác nhau trong các môi trường biến động khác nhau.

- Hoàn thiện hệ thống quản lý vốn, thêm cơ chế quản lý vị thế động và kiểm soát rủi ro.

- Phát triển thuật toán lọc thông minh, giảm tín hiệu giả trong thị trường dao động ngang.

- Tích hợp chỉ báo tâm lý thị trường, nâng cao độ chính xác của tín hiệu giao dịch.

Kết luận

Chiến lược này xây dựng một hệ thống giao dịch tương đối hoàn chỉnh thông qua sự phối hợp của nhiều chỉ báo kỹ thuật. Việc bổ sung cơ chế xác nhận khối lượng đã cải thiện độ tin cậy của tín hiệu giao dịch, nhưng hệ thống vẫn cần hoàn thiện về kiểm soát rủi ro và tối ưu hóa tham số. Ưu điểm cốt lõi của chiến lược nằm ở logic rõ ràng, khả năng điều chỉnh cao, phù hợp làm khung cơ bản để tiếp tục tối ưu hóa và mở rộng. Khuyến nghị nhà giao dịch trước khi sử dụng thực tế nên tiến hành đầy đủ backtest dữ liệu lịch sử và phân tích độ nhạy tham số, đồng thời điều chỉnh phù hợp theo môi trường thị trường cụ thể và khẩu vị rủi ro cá nhân.

/*backtest

start: 2024-02-22 00:00:00

end: 2025-02-19 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("BTCUSDT Strategy with Volume, MACD, RSI, StochRSI", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input parameters- 1