Tổng quan

Chiến lược này là một hệ thống giao dịch theo xu hướng kết hợp đa chỉ báo, tích hợp phân tích từ ba khía cạnh: xu hướng thị trường, động lượng và biến động. Logic cốt lõi là sử dụng đám mây Ichimoku (Ichimoku Cloud) để xác định xu hướng thị trường, biểu đồ histogram MACD để xác nhận động lượng, độ rộng Bollinger Band (Bollinger Band Width) để lọc trạng thái biến động của thị trường, đồng thời đưa vào cơ chế xác nhận xu hướng ở khung thời gian tuần, và cuối cùng quản lý rủi ro bằng lệnh dừng lỗ động dựa trên ATR.

Nguyên lý chiến lược

Chiến lược áp dụng cơ chế lọc tín hiệu nhiều lớp: Đầu tiên, sử dụng đường Leading Span A và B của đám mây Ichimoku để xác định xem giá có nằm trên hay dưới đám mây, từ đó xác định xu hướng lớn của thị trường; Thứ hai, sử dụng biểu đồ histogram MACD để đánh giá cường độ động lượng, yêu cầu khi ở vị thế mua thì histogram lớn hơn -0.05, khi ở vị thế bán thì nhỏ hơn 0; Thứ ba, đưa vào đường trung bình động 50 chu kỳ của khung thời gian tuần để xác nhận hướng xu hướng ở khung thời gian lớn hơn; Thứ tư, sử dụng chỉ báo độ rộng Bollinger Band để lọc các phiên giao dịch có biến động thấp, chỉ mở lệnh khi độ rộng lớn hơn 0.02. Về cài đặt dừng lỗ, chiến lược tự động điều chỉnh dựa trên trạng thái biến động của thị trường: khi biến động thấp, sử dụng mức cao/thấp trước đó; khi biến động cao, sử dụng bội số của ATR.

Ưu điểm của chiến lược

- Lọc tín hiệu đa chiều: Sự kết hợp các chỉ báo từ ba khía cạnh xu hướng, động lượng và biến động giúp giảm hiệu quả các tín hiệu nhiễu.

- Phân tích đa khung thời gian: Đưa vào xác nhận xu hướng khung tuần, nâng cao độ chính xác của hướng giao dịch.

- Quản lý rủi ro động: Cơ chế dừng lỗ tự động thích ứng dựa trên ATR và độ rộng Bollinger Band, vừa bảo vệ lợi nhuận vừa tạo không gian cho xu hướng phát triển.

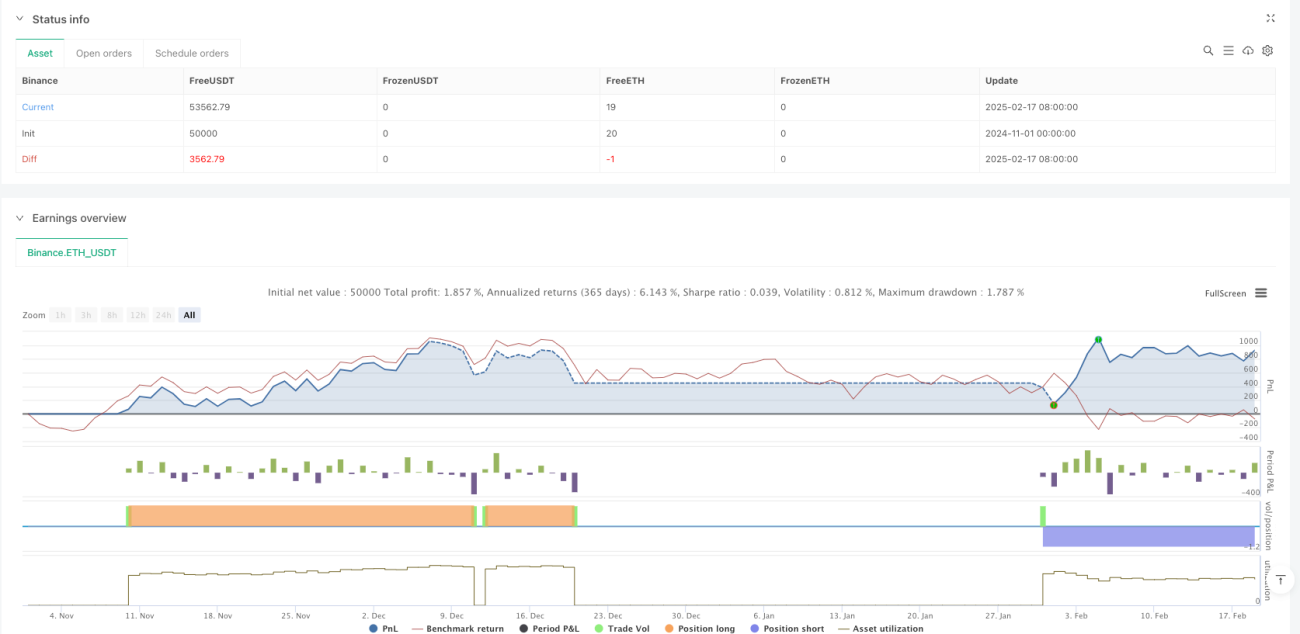

- Kết quả backtest xuất sắc: Lợi nhuận ròng 10,80%, tỷ lệ lợi nhuận/rủi ro 2,593, tỷ lệ thắng 50,70%, drawdown tối đa chỉ 1,47%.

Rủi ro của chiến lược

- Phụ thuộc vào xu hướng: Chiến lược có thể tạo ra nhiều tín hiệu nhiễu trong thị trường đi ngang.

- Nhạy cảm với tham số: Các tham số của nhiều chỉ báo cần được tối ưu hóa cho các điều kiện thị trường khác nhau.

- Rủi ro độ trễ: Việc lọc tín hiệu nhiều lớp có thể khiến thời điểm vào lệnh bị trễ, bỏ lỡ một phần biến động giá.

- Hạn chế của backtest: Kết quả lịch sử không đảm bảo cho hiệu suất tương lai; khi giao dịch thực tế cần xem xét thêm trượt giá và phí giao dịch.

Hướng tối ưu hóa chiến lược

- Tối ưu hệ thống tín hiệu: Có thể đưa vào các chỉ báo động lượng khác như RSI để tăng độ tin cậy của tín hiệu.

- Tối ưu quản lý vị thế: Có thể điều chỉnh linh hoạt quy mô vị thế dựa trên biến động.

- Tối ưu cơ chế chốt lời: Có thể thêm dừng lỗ trượt hoặc điều kiện chốt lời dựa trên chỉ báo kỹ thuật.

- Tối ưu khả năng thích ứng thị trường: Điều chỉnh tham số động theo các trạng thái thị trường khác nhau.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch theo xu hướng hoàn chỉnh thông qua việc kết hợp đa chỉ báo và phân tích đa khung thời gian, đồng thời trang bị cơ chế quản lý rủi ro động. Mặc dù kết quả backtest xuất sắc, nhưng vẫn cần chú ý đến rủi ro do thay đổi môi trường thị trường; khuyến nghị kiểm tra kỹ lưỡng và liên tục tối ưu hóa khi giao dịch thực tế.

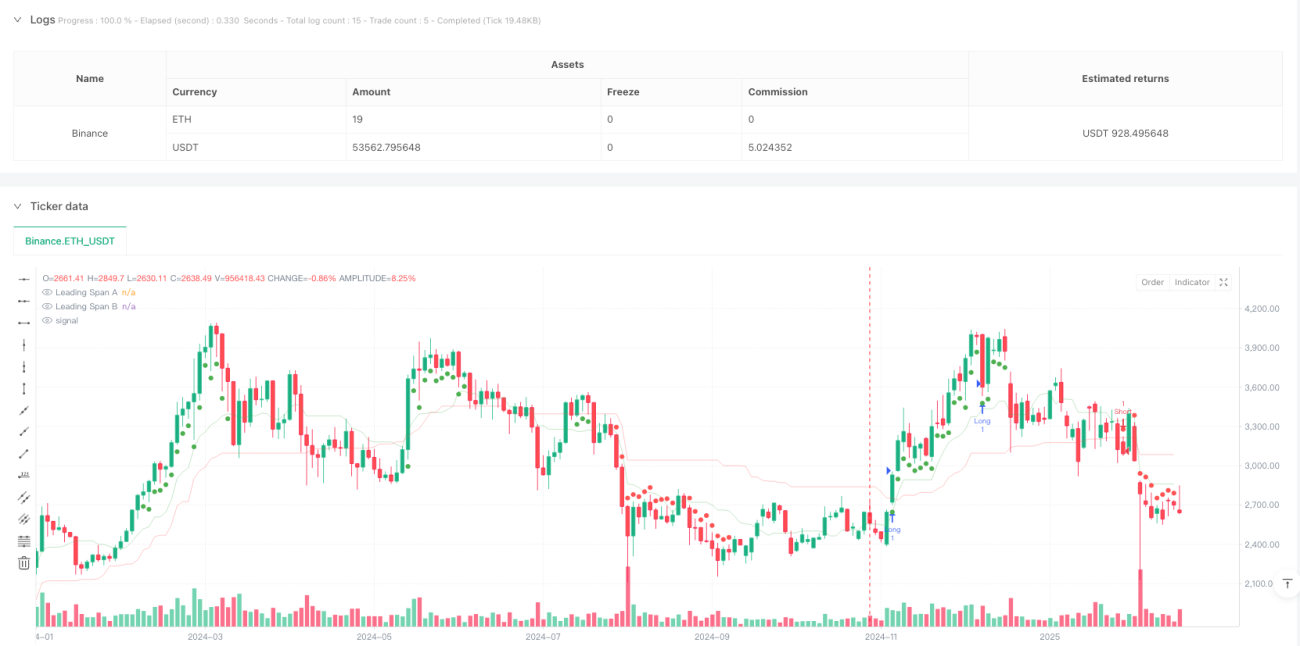

/*backtest

start: 2024-11-01 00:00:00

end: 2025-02-19 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FIWB

//@version=6

strategy("Momentum Edge Strategy - 1D BTC Optimized", overlay=true)- 1