Hệ thống giao dịch xu hướng thích ứng đa chiều thông minh

Tổng quan

Chiến lược này là một hệ thống giao dịch thông minh kết hợp nhiều chỉ báo kỹ thuật, xác định cơ hội thị trường thông qua phân tích tổng hợp Fair Value Gap (FVG), tín hiệu xu hướng và hành vi giá. Hệ thống áp dụng cơ chế chiến lược kép, kết hợp đặc điểm giao dịch theo xu hướng và giao dịch swing, tối ưu hóa hiệu suất giao dịch thông qua quản lý vị thế động và cơ chế thoát lệnh đa chiều. Chiến lược này đặc biệt chú trọng kiểm soát rủi ro, nâng cao chất lượng tín hiệu thông qua bộ lọc biến động và xác nhận khối lượng giao dịch.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên các khía cạnh sau:

- Xác định khoảng trống FVG – Tính toán kích thước khoảng trống giá để tìm kiếm cơ hội giao dịch tiềm năng.

- Hệ thống xác nhận xu hướng – Kết hợp đường trung bình động 200 kỳ, chỉ báo SuperTrend và MACD để xác nhận xu hướng thị trường.

- Xác nhận dòng tiền thông minh – Sử dụng tín hiệu quá mua/quá bán RSI, khối lượng bất thường và mô hình hành vi giá làm điều kiện kích hoạt giao dịch.

- Quản lý vị thế động – Điều chỉnh kích thước vị thế dựa trên biến động (ATR), đảm bảo mức độ rủi ro nhất quán.

- Cơ chế thoát lệnh đa tầng – Kết hợp trailing stop và chốt lời mục tiêu để quản lý thoát lệnh.

Ưu điểm chiến lược

- Khả năng thích ứng cao – Chiến lược tự động điều chỉnh tham số và vị thế dựa trên biến động thị trường.

- Kiểm soát rủi ro hoàn thiện – Kiểm soát rủi ro thông qua nhiều bộ lọc và quản lý vị thế chặt chẽ.

- Tín hiệu đáng tin cậy – Nâng cao độ chính xác của tín hiệu giao dịch thông qua xác nhận đa chiều.

- Phương thức giao dịch linh hoạt – Có thể đồng thời nắm bắt cơ hội từ xu hướng và thị trường đi ngang.

- Quản lý vốn khoa học – Áp dụng quản lý rủi ro theo tỷ lệ phần trăm, đảm bảo sử dụng vốn hợp lý.

Rủi ro chiến lược

- Nhạy cảm với tham số – Việc thiết lập nhiều tham số có thể ảnh hưởng đến hiệu suất, cần tối ưu hóa liên tục.

- Phụ thuộc vào môi trường thị trường – Trong một số điều kiện thị trường, có thể xuất hiện tín hiệu phá vỡ giả.

- Ảnh hưởng của trượt giá – Có thể đối mặt với trượt giá lớn ở thị trường có tính thanh khoản thấp.

- Độ phức tạp tính toán – Việc tính toán nhiều chỉ báo có thể gây chậm trễ tín hiệu.

- Yêu cầu vốn cao – Để triển khai đầy đủ chiến lược cần quy mô vốn ban đầu lớn.

Hướng tối ưu hóa chiến lược

- Tối ưu trọng số chỉ báo – Có thể áp dụng phương pháp học máy để điều chỉnh trọng số các chỉ báo một cách động.

- Tăng cường thích ứng thị trường – Bổ sung cơ chế tự thích ứng với biến động thị trường.

- Cải thiện bộ lọc tín hiệu – Đưa thêm nhiều chỉ báo vi mô thị trường hơn.

- Tối ưu cơ chế thực thi – Bổ sung cơ chế chia nhỏ lệnh thông minh để giảm chi phí tác động.

- Nâng cấp kiểm soát rủi ro – Bổ sung hệ thống quản lý ngân sách rủi ro động.

Tổng kết

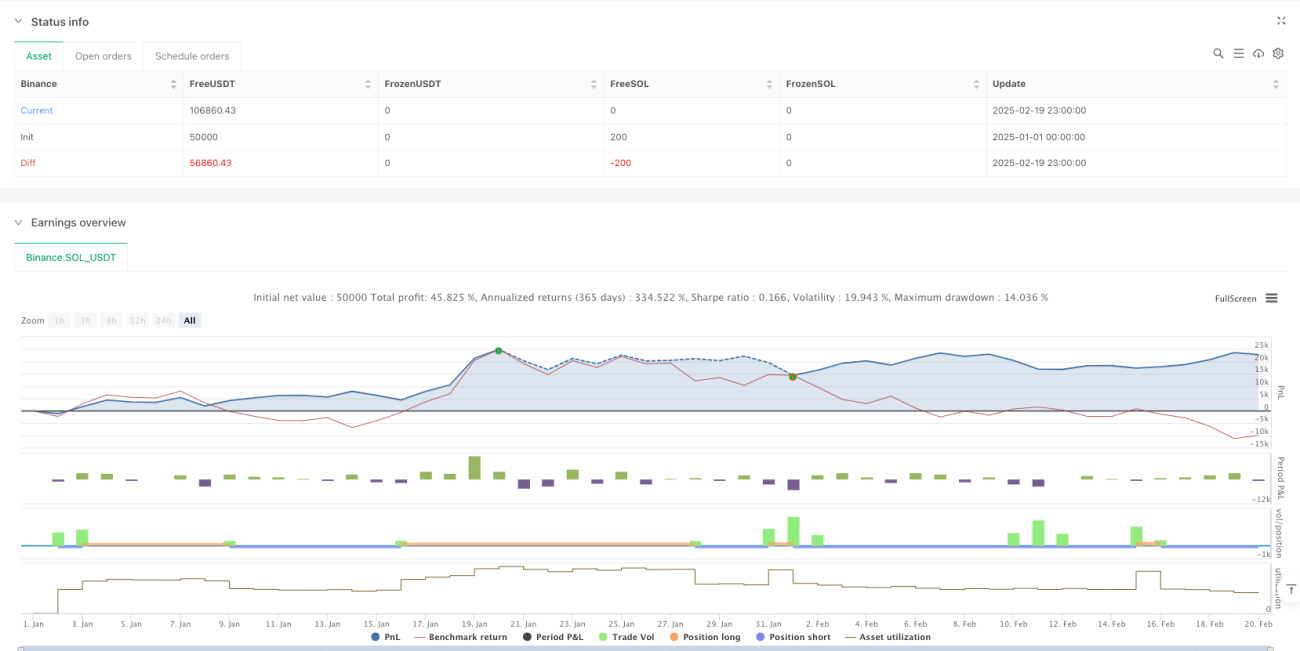

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh thông qua việc kết hợp tổng hợp nhiều chỉ báo kỹ thuật và kỹ thuật giao dịch. Ưu điểm của nó nằm ở khả năng thích ứng với biến động thị trường, đồng thời duy trì kiểm soát rủi ro chặt chẽ. Mặc dù còn một số không gian tối ưu hóa, nhưng nhìn chung đây là một chiến lược giao dịch định lượng được thiết kế hợp lý.

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1