Tổng quan

Chiến lược này là một hệ thống giao dịch kết hợp độ chính xác lượng tử và nhiều chỉ báo kỹ thuật, đạt được giao dịch ổn định thông qua xác nhận xu hướng đa tầng và quản lý rủi ro. Chiến lược tích hợp phân tích đa chiều như chỉ báo động lượng, phân tích biến động, sức mạnh xu hướng và tâm lý thị trường, tạo thành một hệ thống ra quyết định giao dịch toàn diện.

Nguyên lý chiến lược

Chiến lược áp dụng cơ chế xác nhận tín hiệu giao dịch đa tầng:

- Sử dụng ATR (Dải biến động trung bình thực) để thiết lập cắt lỗ và chốt lời động

- Xác nhận tín hiệu thông qua ba lớp xác nhận: chỉ báo động lượng, biến động và sức mạnh xu hướng

- Giao dịch tại điểm giao cắt của EMA 10 và 30 chu kỳ

- Theo dõi xu hướng kết hợp đường xu hướng thích ứng thần kinh và chỉ báo tâm lý thị trường AI

- Tối ưu quản lý vốn thông qua tỷ lệ lợi nhuận/rủi ro 3:1

Lợi thế của chiến lược

- Hệ thống xác nhận tín hiệu đa chiều giảm đáng kể rủi ro phá vỡ giả

- Thiết lập cắt lỗ động thích ứng với các điều kiện thị trường khác nhau

- Đường xu hướng thích ứng thần kinh cung cấp hướng xu hướng chính xác hơn

- Chỉ báo tâm lý thị trường AI tăng cường khả năng nhìn nhận thị trường

- Hệ thống quản lý rủi ro hoàn chỉnh đảm bảo an toàn vốn

- Logic chiến lược rõ ràng, dễ bảo trì và tối ưu hóa

Rủi ro của chiến lược

- Cơ chế xác nhận đa tầng có thể dẫn đến tín hiệu vào lệnh chậm trễ

- Có thể kích hoạt cắt lỗ thường xuyên trong thị trường biến động cao

- Cắt lỗ động có thể không đủ nhanh khi thị trường thay đổi đột ngột

- Cần lượng dữ liệu mẫu lớn để tối ưu hóa tham số

- Độ phức tạp tính toán cao, có thể ảnh hưởng đến hiệu suất thực thi

Hướng tối ưu hóa chiến lược

- Giới thiệu hệ thống tối ưu hóa tham số thích ứng, điều chỉnh động các tham số chỉ báo theo trạng thái thị trường

- Thêm bộ lọc biến động thị trường, tự động điều chỉnh vị thế trong điều kiện thị trường cực đoan

- Tối ưu hóa logic tạo tín hiệu xác nhận, giảm độ trễ tín hiệu

- Đưa thuật toán học máy vào để tối ưu hóa chỉ báo tâm lý thị trường

- Xem xét chi phí giao dịch, tối ưu hóa tần suất giao dịch

Tổng kết

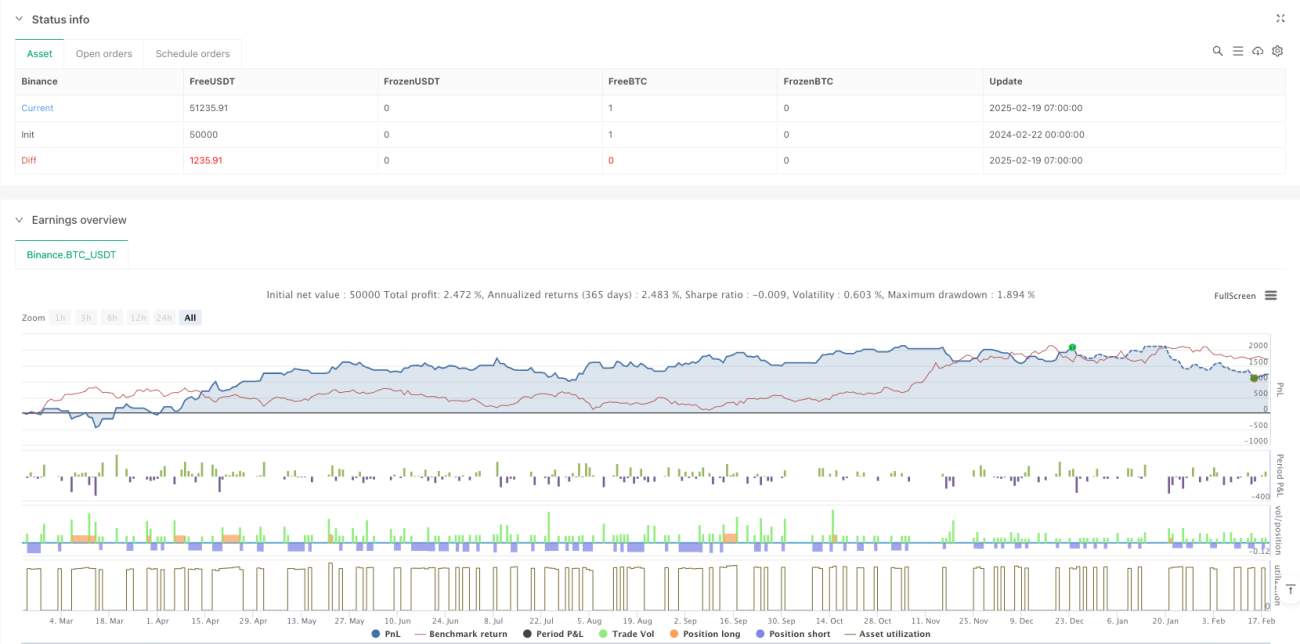

Đây là một hệ thống giao dịch hoàn chỉnh kết hợp phân tích kỹ thuật truyền thống và phương pháp định lượng hiện đại. Thông qua xác nhận tín hiệu đa tầng và quản lý rủi ro, chiến lược vừa đảm bảo tính ổn định vừa có khả năng thích ứng tốt. Mặc dù còn một số không gian tối ưu hóa, nhưng khung tổng thể hợp lý, phù hợp cho vận hành thực tế dài hạn. Bằng cách liên tục tối ưu và hoàn thiện, chiến lược này có tiềm năng duy trì hiệu suất ổn định trong nhiều điều kiện thị trường khác nhau.

/*backtest

start: 2024-02-22 00:00:00

end: 2025-02-19 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Quantum Precision Forex Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input parameters- 1