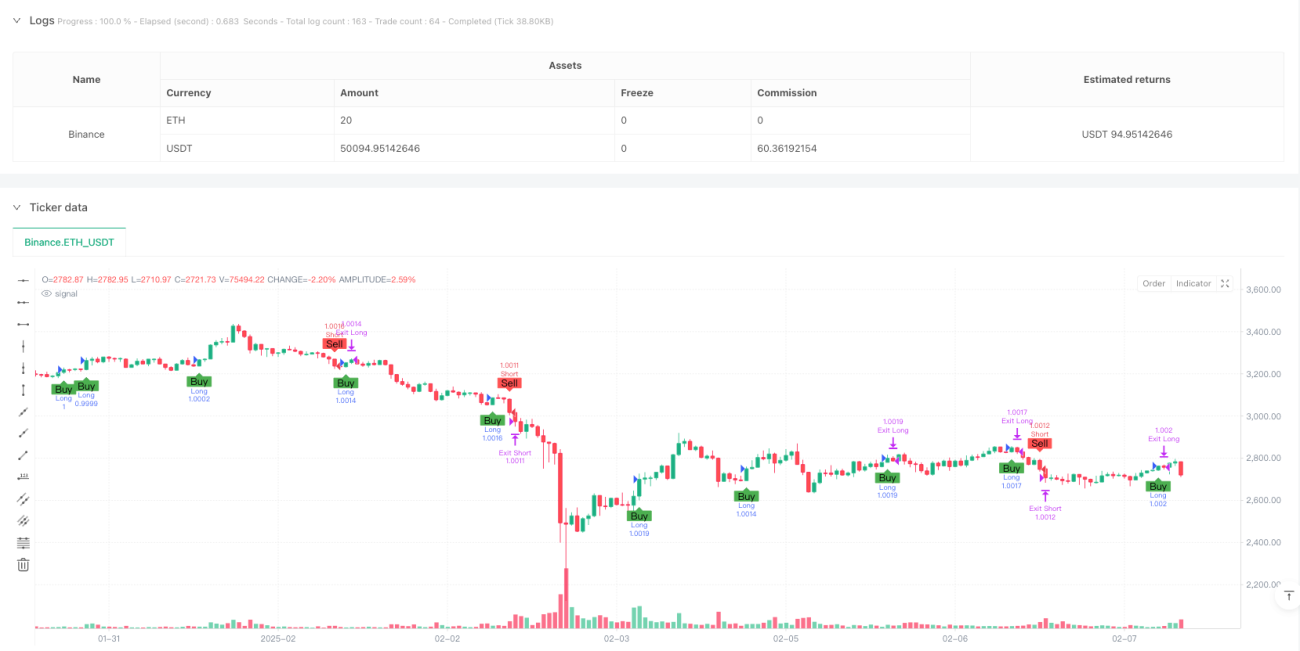

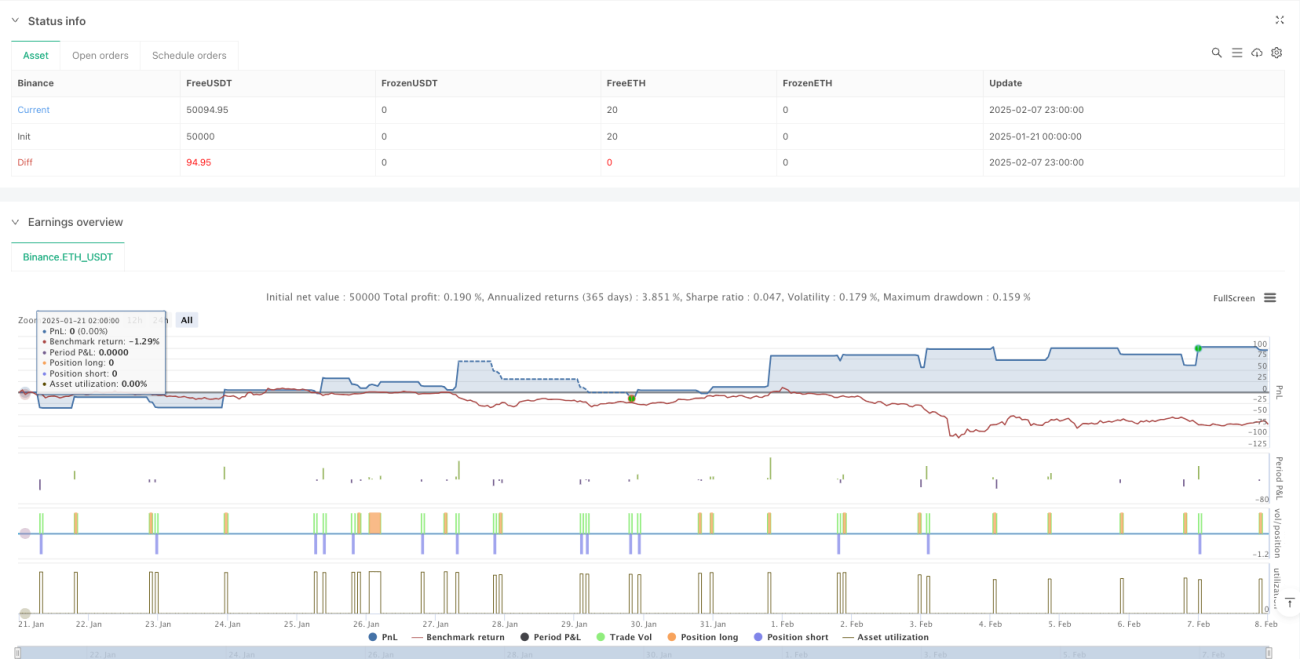

Tổng quan

Đây là một chiến lược giao dịch tự động hoàn toàn dựa trên động lượng trong ngày, kết hợp quản lý rủi ro chặt chẽ và hệ thống quản lý vị thế chính xác. Chiến lược này chủ yếu hoạt động trong phiên giao dịch London, tìm kiếm cơ hội giao dịch bằng cách nhận diện sự thay đổi động lượng thị trường và loại trừ các mô hình Doji, đồng thời áp dụng quy tắc chốt lời hàng ngày để kiểm soát rủi ro. Chiến lược sử dụng phương pháp quản lý vị thế linh hoạt, tự động điều chỉnh quy mô giao dịch dựa trên vốn chủ sở hữu tài khoản, đảm bảo tối ưu hóa việc sử dụng vốn.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược được xây dựng dựa trên nhiều thành phần chính. Đầu tiên, thời gian giao dịch được giới hạn trong phiên London (loại trừ giờ 0 và sau 19h) để đảm bảo thanh khoản thị trường đầy đủ. Tín hiệu vào lệnh dựa trên sự bứt phá động lượng giá, yêu cầu cụ thể đỉnh của nến hiện tại phá vỡ đỉnh của nến trước đó (mua lên) hoặc đáy phá vỡ đáy của nến trước đó (bán xuống), đồng thời cần đáp ứng yêu cầu đồng nhất hướng. Để tránh phá vỡ giả, chiến lược loại trừ rõ ràng các nến Doji. Chiến lược cũng áp dụng quy tắc chốt lời hàng ngày, khi đạt được lợi nhuận mục tiêu, sẽ không mở thêm vị thế mới trong ngày.

Lợi thế của chiến lược

- Quản lý rủi ro toàn diện: Bao gồm cắt lỗ cố định, chốt lời cố định, quy tắc chốt lời hàng ngày và quản lý vị thế linh hoạt

- Tính thích ứng cao: Quy mô giao dịch tự động điều chỉnh theo vốn chủ sở hữu tài khoản, phù hợp với các quy mô vốn khác nhau

- Đảm bảo thanh khoản: Nghiêm ngặt giới hạn giao dịch trong phiên London, tránh rủi ro thanh khoản thấp

- Lọc tín hiệu giả: Bằng cách loại trừ mô hình Doji và tín hiệu liên tiếp, giảm thiểu tổn thất do phá vỡ giả

- Logic thực thi rõ ràng: Điều kiện vào và ra lệnh minh bạch, dễ dàng giám sát và tối ưu hóa

Rủi ro của chiến lược

- Rủi ro biến động thị trường: Trong thời kỳ biến động cao, dừng lỗ cố định có thể không đủ linh hoạt

- Rủi ro trượt giá: Có thể gặp trượt giá lớn khi thị trường biến động nhanh

- Phụ thuộc vào xu hướng: Chiến lược có thể tạo ra nhiều tín hiệu giả trong thị trường đi ngang

- Nhạy cảm với tham số: Cài đặt cắt lỗ, chốt lời có ảnh hưởng lớn đến hiệu suất chiến lược

Giải pháp bao gồm: áp dụng cơ chế dừng lỗ động, thêm bộ lọc biến động thị trường, đưa vào các chỉ báo xác nhận xu hướng, v.v.

Hướng tối ưu hóa chiến lược

- Giới thiệu cơ chế dừng lỗ thích ứng: Điều chỉnh phạm vi dừng lỗ dựa trên ATR hoặc biến động

- Thêm bộ lọc môi trường thị trường: Thêm chỉ báo sức mạnh xu hướng, tăng thời gian nắm giữ khi xu hướng rõ ràng

- Tối ưu hóa cơ chế xác nhận tín hiệu: Kết hợp khối lượng giao dịch và các chỉ báo kỹ thuật khác để nâng cao độ tin cậy

- Hoàn thiện quản lý vốn: Giới thiệu hệ thống quản lý rủi ro tổng hợp, xem xét kiểm soát drawdown

- Tăng cường phân tích vi cấu trúc thị trường: Tích hợp dữ liệu dòng lệnh để nâng cao độ chính xác khi vào lệnh

Tổng kết

Chiến lược này xây dựng một khung giao dịch hoàn chỉnh bằng cách kết hợp động lượng phá vỡ, quản lý rủi ro chặt chẽ và hệ thống thực thi tự động. Lợi thế chính của chiến lược nằm ở hệ thống kiểm soát rủi ro toàn diện và thiết kế thích ứng, tuy nhiên vẫn cần tối ưu hóa trong việc nhận diện môi trường thị trường và lọc tín hiệu. Thông qua cải tiến liên tục và tối ưu hóa tham số, chiến lược này có khả năng duy trì hiệu suất ổn định trong các điều kiện thị trường khác nhau.

/*backtest

start: 2025-01-21 00:00:00

end: 2025-02-08 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Trading Strategy for XAUUSD (Gold) – Automated Execution Plan", overlay=true, initial_capital=10000, currency=currency.USD)

//────────────────────────────- 1