Tổng quan

Đây là chiến lược giao dịch định lượng dựa trên sự giao nhau của nhiều đường trung bình động kết hợp với bộ lọc khối lượng. Chiến lược sử dụng ba đường trung bình động với chu kỳ khác nhau (EMA nhanh, EMA chậm và SMA xu hướng) làm chỉ số cốt lõi, kết hợp với bộ lọc khối lượng để xác nhận hiệu lực của tín hiệu giao dịch. Chiến lược cũng tích hợp các chức năng dừng lỗ và chốt lời, giúp kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa trên các yếu tố cốt lõi sau:

- Sử dụng đường trung bình động hàm mũ (EMA) chu kỳ 9 và 21 để xác định giao nhau, tạo tín hiệu giao dịch ban đầu

- Đưa vào đường trung bình động đơn giản (SMA) chu kỳ 50 làm bộ lọc xu hướng, đảm bảo hướng giao dịch phù hợp với xu hướng chính

- Sử dụng 1,5 lần khối lượng trung bình 20 chu kỳ làm điều kiện lọc khối lượng, đảm bảo tính thanh khoản của giao dịch

- Kết hợp xác nhận hiệu lực tín hiệu khi giá phá vỡ với khối lượng gia tăng

- Thiết lập dừng lỗ 1% và chốt lời 400% để kiểm soát tỷ lệ lợi nhuận/rủi ro

Lợi thế của chiến lược

- Cơ chế xác nhận nhiều lớp: Thông qua ba cơ chế là giao nhau của đường trung bình nhanh/chậm, lọc đường xu hướng và xác nhận khối lượng, độ tin cậy của tín hiệu được cải thiện đáng kể

- Kiểm soát rủi ro hoàn thiện: Thiết lập tỷ lệ dừng lỗ và chốt lời hợp lý, có thể kiểm soát drawdown hiệu quả

- Khả năng bám xu hướng mạnh: Thông qua lọc đường trung bình dài hạn, đảm bảo hướng giao dịch phù hợp với xu hướng chính

- Chất lượng tín hiệu cao: Bộ lọc khối lượng có thể tránh hiệu quả các phá vỡ giả

- Tham số linh hoạt có thể điều chỉnh: Các tham số chỉ số đều có thể được tối ưu hóa theo đặc điểm thị trường khác nhau

Rủi ro của chiến lược

- Rủi ro thị trường dao động: Trong thị trường đi ngang có thể phát sinh tín hiệu giao dịch thường xuyên, làm tăng chi phí giao dịch

- Rủi ro trượt giá: Khi thanh khoản kém có thể đối mặt với trượt giá lớn

- Rủi ro phá vỡ giả: Mặc dù có bộ lọc khối lượng, vẫn có thể gặp phá vỡ giả

- Rủi ro tối ưu hóa tham số: Quá tối ưu hóa có thể dẫn đến overfitting

- Phụ thuộc vào môi trường thị trường: Chiến lược hoạt động tốt hơn trong thị trường có xu hướng rõ ràng, nhưng có thể kém hiệu quả trong các môi trường thị trường khác

Hướng tối ưu hóa chiến lược

- Đưa chỉ số biến động: Có thể xem xét thêm chỉ số ATR để điều chỉnh vị trí dừng lỗ động

- Tối ưu hóa bộ lọc khối lượng: Có thể xem xét sử dụng khối lượng tương đối thay vì khối lượng tuyệt đối làm điều kiện lọc

- Thêm xác nhận độ mạnh xu hướng: Có thể đưa các chỉ số như ADX để xác nhận độ mạnh xu hướng

- Hoàn thiện cơ chế chốt lời: Có thể thiết kế chốt lời động để khóa lợi nhuận tốt hơn

- Thêm bộ lọc thời gian: Tránh giao dịch trong các khung thời gian thanh khoản thấp

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch tương đối hoàn chỉnh thông qua sự kết hợp của nhiều chỉ số kỹ thuật. Lợi thế cốt lõi của chiến lược nằm ở cơ chế xác nhận nhiều lớp và kiểm soát rủi ro hoàn thiện, nhưng vẫn cần tối ưu hóa tham số và cải tiến chiến lược dựa trên điều kiện thị trường thực tế. Với sự tối ưu hóa và kiểm soát rủi ro hợp lý, chiến lược này có tiềm năng đạt được lợi nhuận ổn định trong thị trường có xu hướng.

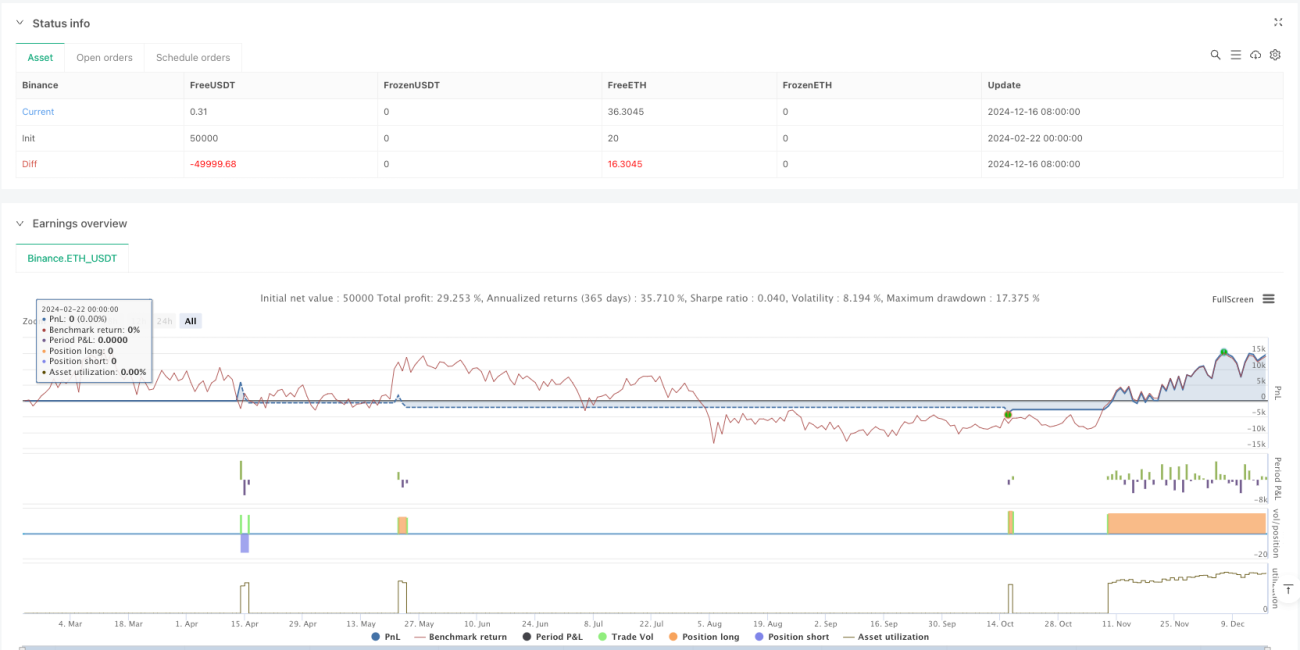

/*backtest

start: 2024-02-22 00:00:00

end: 2024-12-17 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Optimized Moving Average Crossover Strategy with Volume Filter", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Inputs for Moving Averages- 1