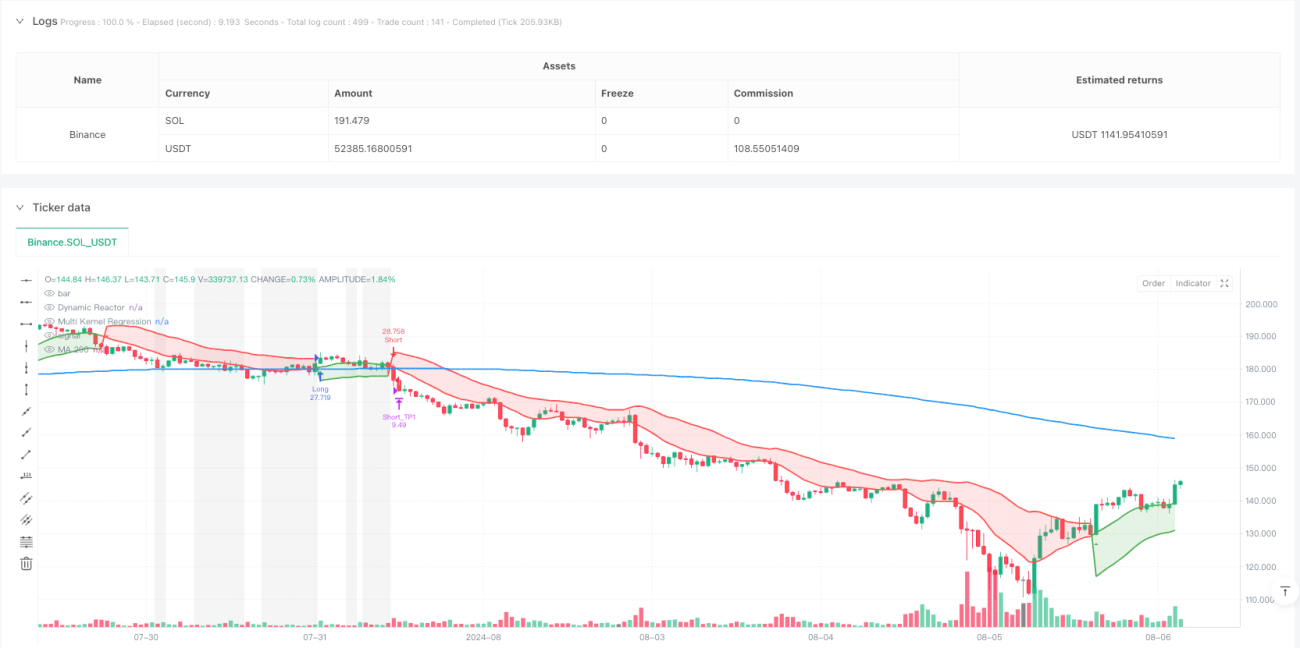

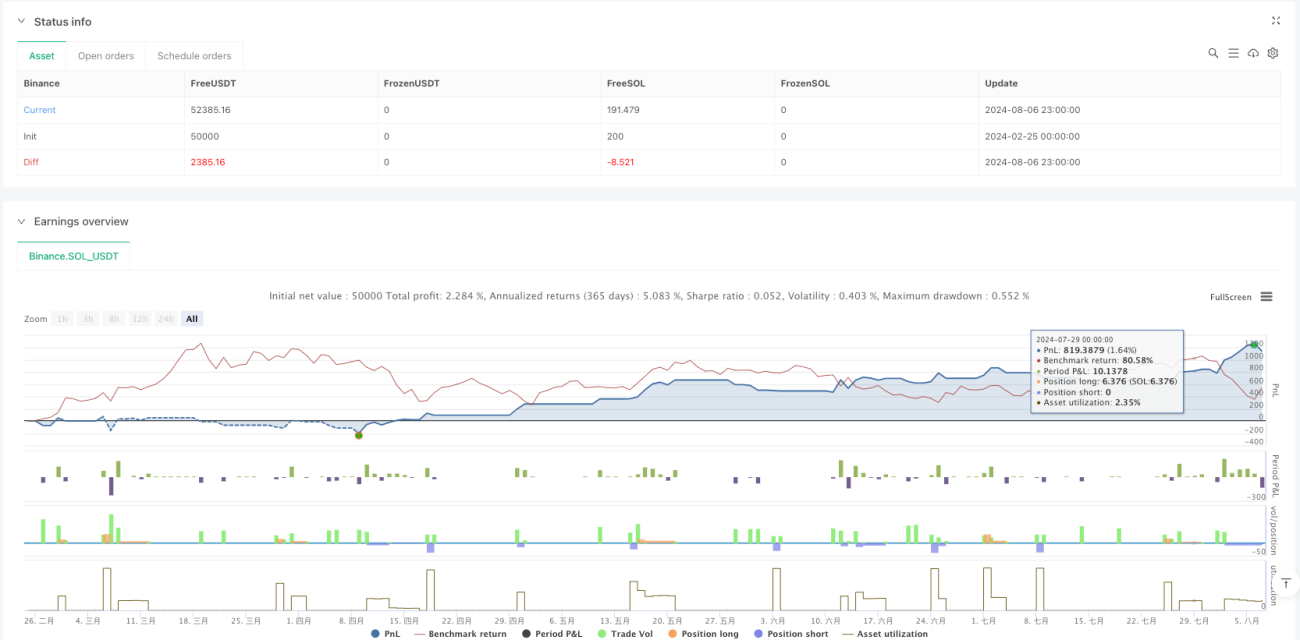

Tổng quan

Đây là một chiến lược giao dịch theo xu hướng kết hợp Bộ phản ứng xu hướng động (Dynamic Reactor) và Hồi quy đa nhân (Multi-Kernel Regression). Chiến lược này tính toán các đường hỗ trợ/kháng cự động thông qua ATR và SMA, đồng thời sử dụng hồi quy kết hợp giữa nhân Gaussian và nhân Epanechnikov để nhận diện xu hướng thị trường. Ngoài ra, chiến lược còn kết hợp đường trung bình động MA200 làm bộ lọc xu hướng dài hạn và thiết lập cơ chế chốt lời ba cấp cùng cắt lỗ.

Nguyên lý chiến lược

Chiến lược chủ yếu bao gồm bốn phần cốt lõi:

-

Bộ phản ứng xu hướng động (DR): Sử dụng ATR và SMA để xây dựng dải hỗ trợ/kháng cự động, xác định hướng xu hướng dựa trên vị trí giá. Trong xu hướng tăng, sử dụng dải dưới làm hỗ trợ; trong xu hướng giảm, sử dụng dải trên làm kháng cự.

-

Hồi quy đa nhân (MKR): Kết hợp nhân Gaussian và nhân Epanechnikov để hồi quy giá, tối ưu hóa sự kết hợp của hai hàm nhân thông qua tham số trọng số có thể điều chỉnh. Phương pháp này có thể nắm bắt tốt hơn các đặc điểm động của biến động giá.

-

Bộ lọc xu hướng MA200: Sử dụng đường trung bình động 200 ngày làm chỉ báo xu hướng dài hạn, chỉ cho phép giao dịch khi giá hình thành xu hướng rõ ràng với MA200, đồng thời nhận diện giai đoạn tích lũy thông qua tham số consolidationRange.

-

Hệ thống quản lý vốn: Áp dụng ba mức chốt lời (1,5%, 3,0%, 4,5%) và cắt lỗ 1%, phân bổ vị thế theo tỷ lệ 33%-33%-34%, nhằm tối đa hóa lợi nhuận đồng thời kiểm soát rủi ro.

Ưu điểm của chiến lược

- Độ tin cậy trong nhận diện xu hướng: Nhờ sự xác nhận kép từ DR và MKR, độ chính xác trong phán đoán xu hướng được nâng cao.

- Tính toàn vẹn trong quản lý rủi ro: Kết hợp chốt lời theo từng phần và cắt lỗ thống nhất, vừa bảo vệ lợi nhuận vừa hạn chế thua lỗ.

- Khả năng thích ứng cao: Phương pháp hồi quy đa nhân có thể thích ứng tốt hơn với các điều kiện thị trường khác nhau.

- Tín hiệu giao dịch rõ ràng: Các điểm chuyển đổi xu hướng có chỉ báo đồ họa rõ nét.

- Cơ chế lọc hoàn thiện: Thông qua MA200 và nhận diện giai đoạn tích lũy, loại bỏ các môi trường thị trường bất lợi.

Rủi ro của chiến lược

- Rủi ro tối ưu hóa tham số: Tối ưu hóa quá mức có thể dẫn đến quá khớp (overfitting), làm giảm hiệu suất thực tế của chiến lược.

- Rủi ro độ trễ: Các chỉ báo trung bình động và hồi quy đều có độ trễ nhất định, có thể bỏ lỡ các điểm ngoặt quan trọng.

- Phụ thuộc vào môi trường thị trường: Hiệu suất có thể kém trong thị trường biến động mạnh hoặc đi ngang.

- Rủi ro thực thi: Các lệnh chốt lời và cắt lỗ nhiều mức có thể không được thực thi đầy đủ do vấn đề thanh khoản.

Hướng tối ưu hóa chiến lược

- Điều chỉnh tham số động: Có thể tự động điều chỉnh hệ số nhân ATR và chu kỳ hồi quy dựa trên độ biến động của thị trường.

- Tăng cường xác nhận tín hiệu: Có thể thêm các chỉ báo phụ trợ như khối lượng giao dịch, độ biến động để nâng cao độ tin cậy của tín hiệu.

- Tối ưu hóa quản lý vị thế: Có thể thực hiện quản lý vị thế động dựa trên độ biến động.

- Phân loại môi trường thị trường: Thêm mô-đun nhận diện trạng thái thị trường, sử dụng các bộ tham số khác nhau trong các môi trường thị trường khác nhau.

Kết luận

Chiến lược này xây dựng một hệ thống giao dịch hoàn chỉnh bằng cách kết hợp nhiều chỉ báo kỹ thuật và phương pháp thống kê tiên tiến. Ưu điểm của chiến lược nằm ở khả năng nắm bắt xu hướng chính xác và hệ thống quản lý rủi ro hoàn thiện, nhưng cũng cần chú ý đến vấn đề tối ưu hóa tham số và khả năng thích ứng với thị trường. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược còn có dư địa để cải thiện thêm.

/*backtest

start: 2024-02-25 00:00:00

end: 2024-08-07 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("DR + Multi Kernel Regression + Signals + MA200 with TP/SL (Optimized)", overlay=true, shorttitle="DR+MKR+Signals+MA200_TP_SL_Opt", pyramiding=0, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// =====================================================================- 1