Chiến lược đột phá xu hướng kết hợp đa chiều các chỉ báo kỹ thuật

Tổng quan

Chiến lược này là một hệ thống giao dịch đột phá xu hướng kết hợp nhiều chỉ báo kỹ thuật và mô hình đồ thị. Nó xác định các điểm đảo chiều xu hướng thị trường thông qua việc nhận dạng các mô hình đồ thị chính (như đỉnh/đáy đôi, đầu vai/đáy vai) và sự phá vỡ giá, đồng thời kết hợp các chỉ báo kỹ thuật như EMA, ATR và khối lượng để lọc tín hiệu và quản lý rủi ro, đạt được khả năng bám sát xu hướng và kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược bao gồm ba phần chính:

- Nhận dạng mô hình đồ thị: Sử dụng phương pháp cửa sổ trượt để xác định các mô hình kỹ thuật cổ điển như đỉnh/đáy đôi, mô hình đầu vai, thông qua so sánh các điểm cao/thấp và xác nhận tín hiệu đảo chiều bằng đường EMA giao cắt.

- Hệ thống xác nhận xu hướng: Sử dụng EMA 50 chu kỳ làm bộ lọc xu hướng, kết hợp với phá vỡ giá để xác định hướng xu hướng, đồng thời dùng bộ lọc khối lượng (yêu cầu khối lượng cao hơn 120% trung bình 20 ngày) để xác thực hiệu lực tín hiệu.

- Hệ thống quản lý rủi ro: Thiết lập chốt lời và cắt lỗ động dựa trên ATR 14 chu kỳ, kiểm soát tỷ lệ lợi nhuận/rủi ro chính xác thông qua hệ số nhân ATR 1,5 lần.

Ưu điểm chiến lược

- Tích hợp tín hiệu đa chiều: Kết hợp thông tin thị trường từ nhiều chiều như mô hình đồ thị, đường trung bình động, biến động và khối lượng, tăng độ tin cậy của tín hiệu.

- Quản lý rủi ro động: Sử dụng ATR để điều chỉnh vị thế chốt lời/cắt lỗ linh hoạt, thích ứng với các môi trường thị trường khác nhau.

- Tự động hóa cao: Hệ thống tự động nhận dạng mô hình, phát tín hiệu giao dịch và thực hiện lệnh, giảm can thiệp thủ công.

- Hiển thị trực quan rõ ràng: Thông qua đánh dấu đồ thị và hệ thống cảnh báo, thể hiện trực quan tín hiệu giao dịch.

Rủi ro chiến lược

- Rủi ro phá vỡ giả: Trong thị trường đi ngang có thể xuất hiện tín hiệu phá vỡ giả, cần xác nhận nghiêm ngặt bằng khối lượng.

- Rủi ro độ trễ: Các chỉ báo như đường trung bình động và ATR có độ trễ nhất định, có thể bỏ lỡ thời điểm vào lệnh tối ưu.

- Nhạy cảm với tham số: Hiệu quả chiến lược chịu ảnh hưởng lớn từ cài đặt tham số, cần tối ưu hóa qua backtest để xác định tham số tốt nhất.

- Phụ thuộc vào môi trường thị trường: Trong thị trường đi ngang không có xu hướng rõ rệt, hiệu suất chiến lược có thể không lý tưởng.

Hướng tối ưu hóa chiến lược

- Đưa vào nhận dạng môi trường thị trường: Thêm các chỉ báo sức mạnh xu hướng (như ADX) để phân biệt thị trường xu hướng và thị trường đi ngang, điều chỉnh tham số chiến lược linh hoạt.

- Tối ưu hóa bộ lọc tín hiệu: Có thể cân nhắc thêm các chỉ báo dao động như RSI để lọc thêm các tín hiệu phá vỡ giả.

- Hoàn thiện kiểm soát rủi ro: Đưa vào hệ thống quản lý khối lượng vị thế, điều chỉnh quy mô nắm giữ dựa trên biến động thị trường.

- Tăng cường khả năng thích ứng: Phát triển hệ thống tham số tự động thích ứng, tự động tối ưu tham số chiến lược theo trạng thái thị trường.

Tổng kết

Chiến lược này đạt được khả năng bắt điểm đảo chiều xu hướng thị trường hiệu quả thông qua việc tích hợp các chỉ báo kỹ thuật đa chiều. Thiết kế hệ thống xem xét toàn diện các yếu tố chính như tạo tín hiệu, xác nhận xu hướng và kiểm soát rủi ro, mang tính thực tiễn cao. Thông qua các hướng tối ưu hóa được đề xuất, độ ổn định và khả năng thích ứng của chiến lược dự kiến sẽ được cải thiện hơn nữa. Trong ứng dụng giao dịch thực tế, khuyến nghị các nhà giao dịch điều chỉnh tham số chiến lược phù hợp dựa trên đặc điểm thị trường cụ thể và khẩu vị rủi ro cá nhân.

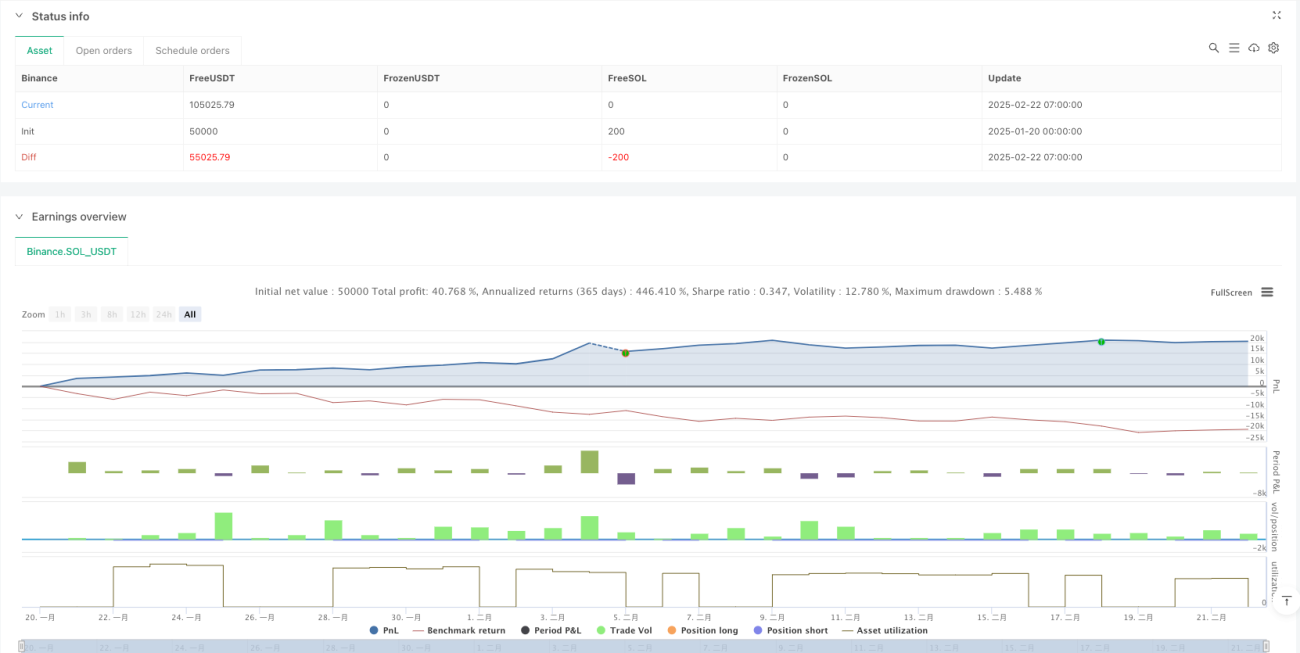

/*backtest

start: 2025-01-20 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Ultimate Pattern Finder", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// 🎯 CONFIGURABLE PARAMETERS- 1