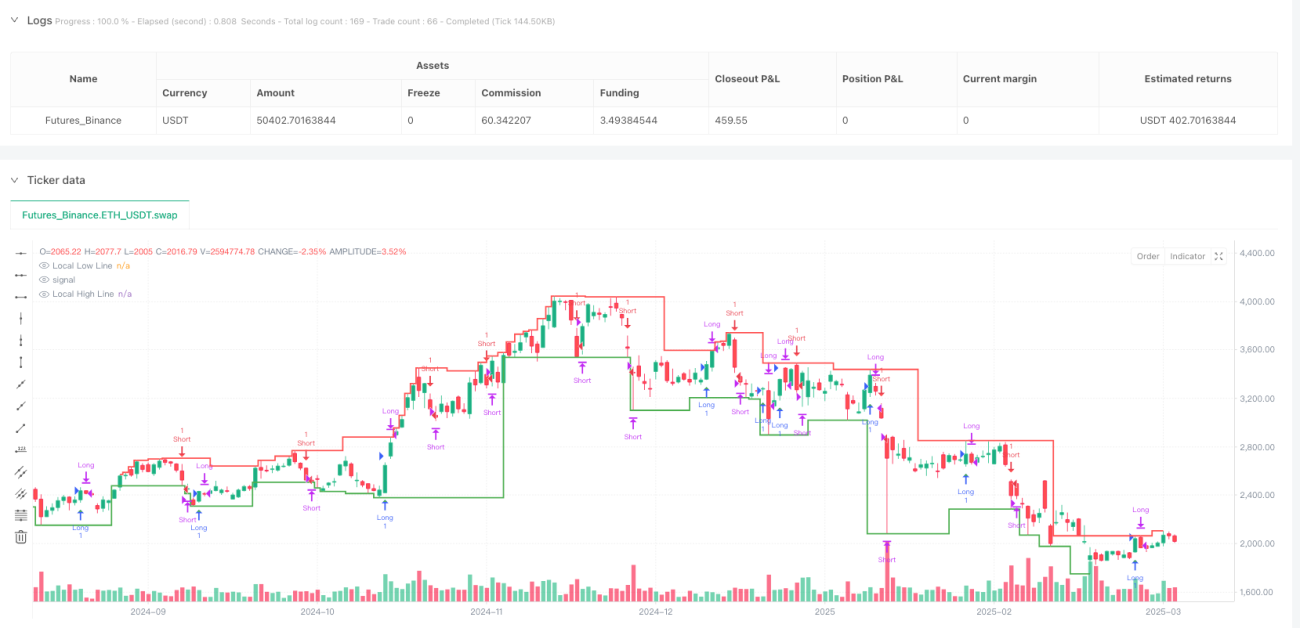

Tổng quan

Đây là một chiến lược giao dịch sáng tạo, kết hợp phân tích vùng thanh khoản và động thái cấu trúc thị trường nội bộ, nhằm xác định điểm vào lệnh xác suất cao. Bằng cách theo dõi tương tác giữa giá và các mức thị trường chính, đồng thời tận dụng sự chuyển đổi thị trường nội bộ để kích hoạt giao dịch, chiến lược này cung cấp cho trader một phương pháp tiếp cận thị trường linh hoạt và chính xác.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược dựa trên hai thành phần chính: nhận diện vùng thanh khoản và chuyển đổi thị trường nội bộ. Vùng thanh khoản được xác định động thông qua phân tích các đỉnh và đáy cục bộ, trong khi chuyển đổi thị trường nội bộ đánh giá sự thay đổi hướng thị trường dựa trên việc giá phá vỡ các mức bullish hoặc bearish trước đó.

Chiến lược có các đặc điểm cốt lõi sau:

- Logic chuyển đổi thị trường nội bộ: Không phụ thuộc vào mô hình nến truyền thống, mà dựa trên việc giá phá vỡ các mức quan trọng.

- Theo dõi vùng thanh khoản: Xác định động các vùng thanh khoản chính, ngăn chặn giao dịch trong điều kiện thị trường yếu.

- Linh hoạt chế độ: Cung cấp ba chế độ giao dịch: "Both" (Cả hai), "Bullish Only" (Chỉ tăng) và "Bearish Only" (Chỉ giảm).

- Quản lý rủi ro: Có thể tùy chỉnh mức cắt lỗ và chốt lời.

- Kiểm soát khung thời gian: Cho phép kiểm soát chính xác khung giờ giao dịch.

Ưu điểm chiến lược

- Thích ứng động: Chiến lược có thể phản ứng nhanh với các thay đổi cấu trúc thị trường.

- Vào lệnh chính xác: Kết hợp vùng thanh khoản và chuyển đổi thị trường nội bộ, giúp tăng độ chính xác khi vào lệnh.

- Rủi ro kiểm soát được: Tích hợp cơ chế cắt lỗ và chốt lời.

- Tính linh hoạt cao: Có thể chọn chế độ giao dịch phù hợp với các điều kiện thị trường khác nhau.

- Phân tích đa chiều: Đồng thời xem xét hành vi giá, thanh khoản và cấu trúc thị trường.

Rủi ro chiến lược

- Biến động thị trường mạnh có thể kích hoạt cắt lỗ.

- Trong thị trường đi ngang, tín hiệu thường xuyên có thể làm tăng chi phí giao dịch.

- Thiết lập tham số không phù hợp có thể ảnh hưởng đến hiệu suất chiến lược.

- Kết quả backtest có thể khác biệt so với giao dịch thực tế.

Hướng tối ưu hóa chiến lược

- Đưa vào thuật toán học máy để tự động tối ưu hóa tham số.

- Thêm nhiều bộ lọc hơn, chẳng hạn như khối lượng giao dịch, chỉ báo biến động.

- Phát triển cơ chế xác nhận đa khung thời gian.

- Tối ưu hóa thuật toán cắt lỗ và chốt lời, xem xét điều chỉnh động theo biến động thị trường.

Tổng kết

Đây là một chiến lược giao dịch sáng tạo kết hợp phân tích thanh khoản và động thái cấu trúc thị trường. Với logic chuyển đổi thị trường nội bộ linh hoạt và khả năng theo dõi vùng thanh khoản chính xác, nó cung cấp cho trader một công cụ giao dịch mạnh mẽ. Chìa khóa của chiến lược nằm ở khả năng thích ứng và phân tích đa chiều, giúp duy trì hiệu suất thực thi cao trong các điều kiện thị trường khác nhau.

- 1