Tổng quan

Chiến lược này là một chiến lược giao dịch cổ phiếu quản lý rủi ro động theo xu hướng đa yếu tố, thông qua việc kết hợp tổng hợp nhiều chỉ báo kỹ thuật nhằm nâng cao độ chính xác của tín hiệu giao dịch và hiệu suất tổng thể của chiến lược. Cốt lõi của chiến lược xoay quanh việc xác định xu hướng, xác nhận động lượng, lọc biến động và kiểm soát rủi ro, cung cấp cho nhà đầu tư một phương pháp giao dịch có hệ thống.

Nguyên lý chiến lược

Nguyên lý chiến lược dựa trên phân tích tổng hợp của sáu chỉ báo chính:

- Chỉ báo G-Channel: Sử dụng đường trung bình động hàm mũ (EMA) 20 ngày và 50 ngày để xác định hướng xu hướng thị trường.

- Xác nhận đường trung bình động biến đổi Fantel (VMA): So sánh đường trung bình động đơn giản (SMA) 14 ngày và 28 ngày để xác thực động lượng xu hướng.

- Xác nhận xu hướng Coral: Sử dụng SMA 10 ngày và 20 ngày để xác định hướng xu hướng ngắn hạn.

- Xác nhận biến động ADX: Đánh giá cường độ xu hướng và mức độ biến động của thị trường.

- Xác nhận khối lượng giao dịch: Kiểm tra xem khối lượng giao dịch có cao hơn đáng kể so với khối lượng trung bình 20 ngày hay không.

- Giá so với SMA 50 ngày: Xác định vị trí của giá trong xu hướng dài hạn.

Ưu điểm của chiến lược

- Xác thực đa yếu tố: Thông qua kiểm chứng chéo sáu chỉ báo từ các chiều hướng khác nhau, giảm đáng kể xác suất tín hiệu giả.

- Quản lý rủi ro động: Sử dụng ATR (Dải biến động trung bình thực) để điều chỉnh linh hoạt mức cắt lỗ và chốt lời.

- Cơ chế vào và thoát linh hoạt: Kết hợp nhiều điều kiện về xu hướng, động lượng, biến động và khối lượng giao dịch.

- Tối ưu tỷ lệ lợi nhuận/rủi ro: Thiết kế tỷ lệ lợi nhuận/rủi ro là 2:1.

- Giao dịch tần suất thấp: Giảm số lần giao dịch, tiết kiệm chi phí giao dịch.

Rủi ro của chiến lược

- Phức tạp trong xác định xu hướng đa chiều: Xác thực đa yếu tố có thể dẫn đến tín hiệu bị trễ.

- Nhạy cảm với tham số: Trong các môi trường thị trường khác nhau, tham số cố định có thể hoạt động kém hiệu quả.

- Hạn chế về khối lượng giao dịch: Khối lượng thấp có thể làm tăng rủi ro đánh giá sai giao dịch.

- Giới hạn cực trị RSI: Có thể bỏ lỡ một số cơ hội giao dịch.

Hướng tối ưu hóa chiến lược

- Thích ứng tham số: Phát triển cơ chế điều chỉnh tham số động.

- Tối ưu hóa bằng học máy: Đưa vào thuật toán học máy để tối ưu thời điểm vào và thoát lệnh.

- Thích ứng đa thị trường: Tùy chỉnh tham số cho các loại sản phẩm và môi trường thị trường khác nhau.

- Kết hợp chỉ báo tâm lý thị trường: Đưa chỉ báo tâm lý thị trường để nâng cao tính ổn định của chiến lược.

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch cổ phiếu tương đối ổn định thông qua việc xác thực tín hiệu giao dịch đa yếu tố, đa chiều. Ưu điểm cốt lõi của nó là giảm rủi ro giao dịch, nhưng vẫn cần liên tục tối ưu hóa và thích ứng với sự thay đổi của thị trường.

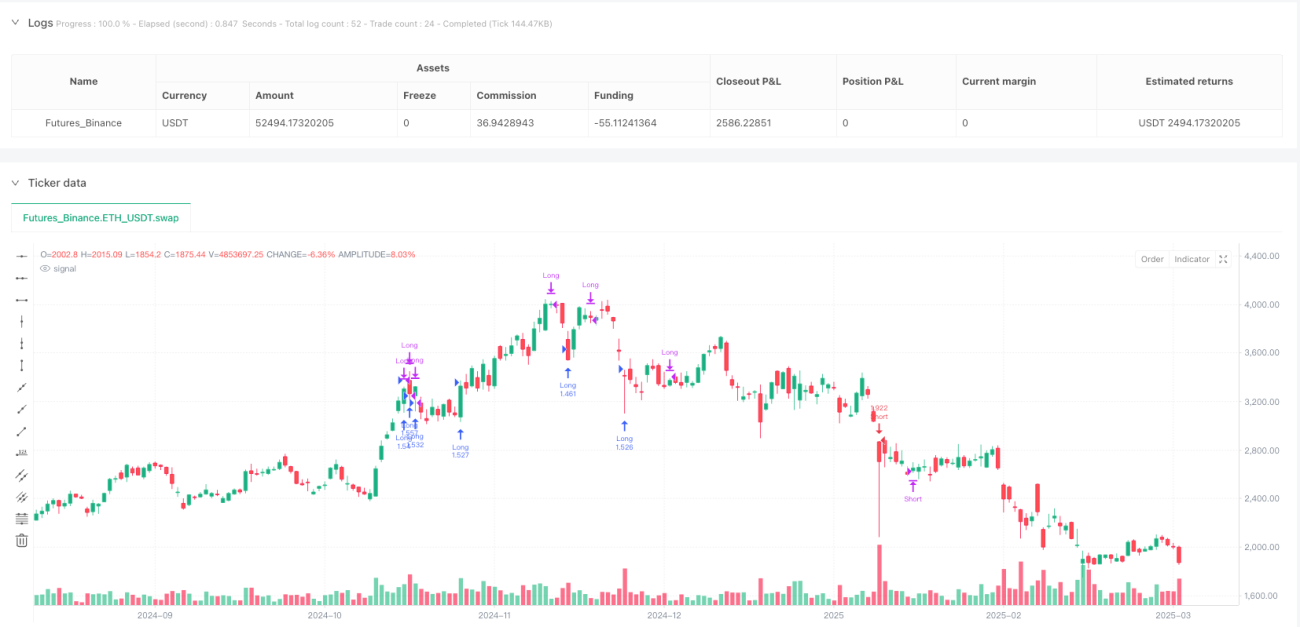

/*backtest

start: 2024-03-31 00:00:00

end: 2025-03-29 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("G-Channel Strategy for Stocks", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// === 1️⃣ G-Channel Indicator ===- 1