2

Follow

502

Followers

Tổng quan

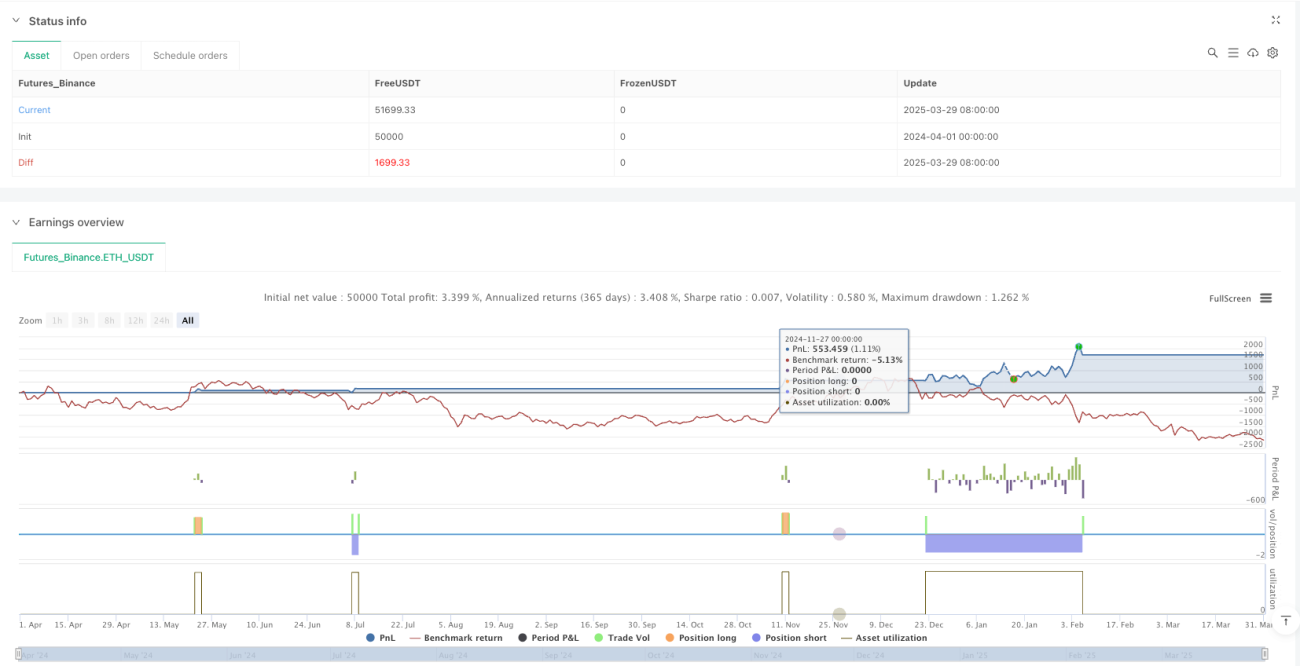

Bài viết này giới thiệu một chiến lược giao dịch kết hợp hai chỉ báo: Bollinger Bands và SuperTrend. Bằng cách tích hợp nhiều công cụ phân tích kỹ thuật, chiến lược này nhằm cung cấp các tín hiệu vào và ra thị trường chính xác hơn, đồng thời giảm thiểu rủi ro giao dịch.

Nguyên lý chiến lược

Chiến lược cốt lõi bao gồm hai phần chính: Bollinger Bands và chỉ báo SuperTrend.

- Phần tính toán Bollinger Bands:

- Sử dụng đường trung bình động (MA) có thể cấu hình để tính đường cơ sở

- Tạo dải trên và dải dưới dựa trên bội số độ lệch chuẩn

- Hỗ trợ nhiều loại đường trung bình động: SMA, EMA, SMMA, WMA và VWMA

- Phần SuperTrend:

- Sử dụng ATR (Khoảng dao động thực trung bình) để tính mức dừng lỗ

- Xác định động thái xu hướng thị trường một cách linh động

- Tạo tín hiệu mua/bán dựa trên sự thay đổi xu hướng

Ưu điểm chiến lược

- Kết hợp đa chỉ báo: Nâng cao độ chính xác tín hiệu nhờ kết hợp Bollinger Bands và SuperTrend

- Cấu hình linh hoạt: Có thể tùy chỉnh loại đường trung bình động, tham số và phương pháp tính toán

- Dừng lỗ động: Cơ chế dừng lỗ dựa trên ATR giúp kiểm soát rủi ro hiệu quả

- Tăng cường trực quan: Cung cấp tô màu trạng thái xu hướng và nhãn tín hiệu

- Quản lý rủi ro: Thiết lập quản lý vị thế theo tỷ lệ phần trăm và giới hạn giao dịch kim tự tháp

Rủi ro chiến lược

- Nhạy cảm với tham số: Trong các môi trường thị trường khác nhau, tham số có thể cần điều chỉnh thường xuyên

- Hạn chế của backtest: Dữ liệu lịch sử không đảm bảo kết quả thị trường tương lai

- Rủi ro chuyển đổi vị thế: Việc thay đổi vị thế thường xuyên có thể làm tăng chi phí giao dịch

- Độ trễ chỉ báo: Các chỉ báo kỹ thuật tồn tại độ trễ tín hiệu nhất định

Hướng tối ưu hóa chiến lược

- Đưa thuật toán học máy vào để tối ưu hóa tham số động

- Thêm bộ lọc bổ sung như xác nhận khối lượng giao dịch

- Phát triển cơ chế xác thực đa khung thời gian

- Tối ưu hóa module quản lý rủi ro, đưa vào chiến lược kiểm soát vị thế tinh vi hơn

Tổng kết

Đây là một chiến lược giao dịch kết hợp nhiều chỉ báo động, thông qua sự kết hợp giữa Bollinger Bands và SuperTrend, cung cấp một hệ thống tín hiệu giao dịch tương đối toàn diện. Cốt lõi của chiến lược nằm ở việc cân bằng giữa độ chính xác tín hiệu và quản lý rủi ro, tuy nhiên vẫn cần liên tục tối ưu hóa và điều chỉnh tùy theo môi trường thị trường khác nhau.

Source

Pine

/*backtest

start: 2024-04-01 00:00:00

end: 2025-03-31 00:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Combined BB & New SuperTrend Strategy", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10, pyramiding=0)

//============================Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1