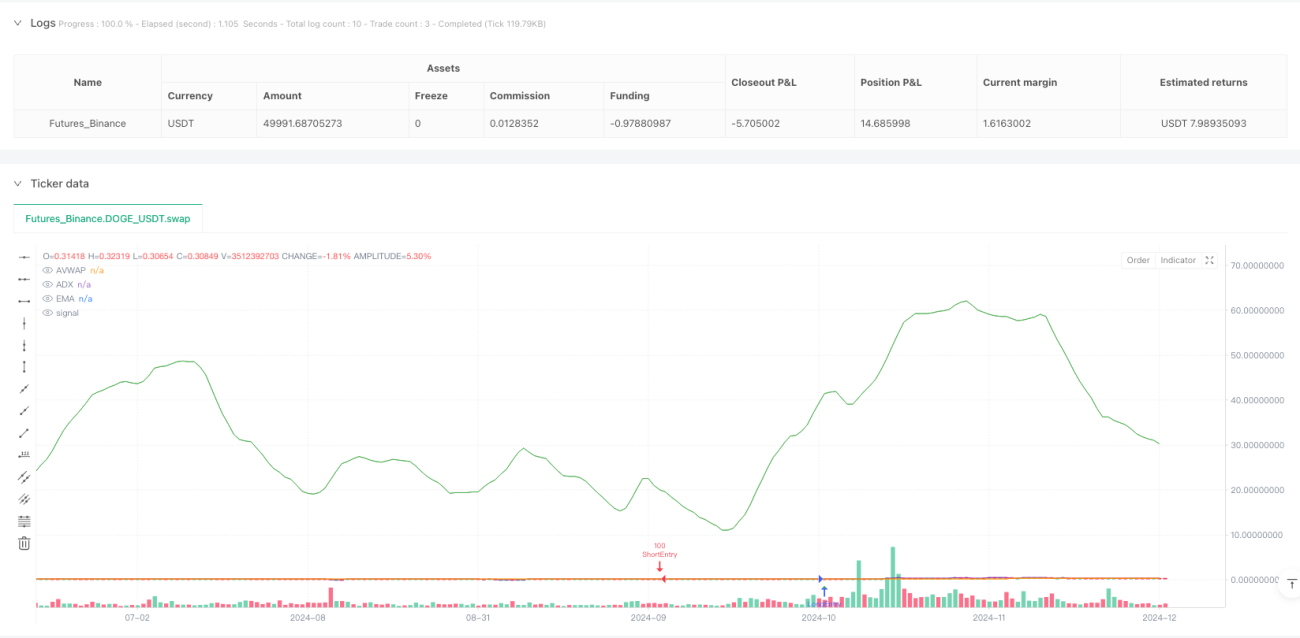

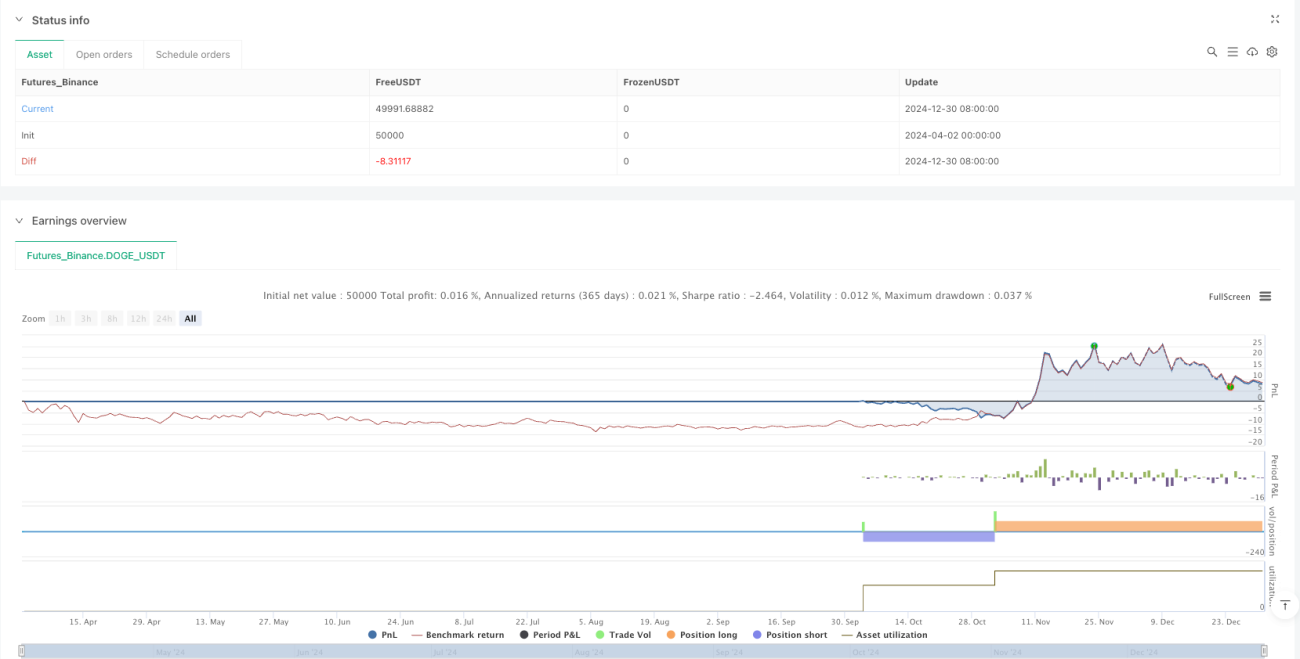

Tổng quan

Đây là một chiến lược giao dịch đa chỉ báo phức tạp, kết hợp nhiều công cụ phân tích kỹ thuật như Giá trung bình theo khối lượng (AVWAP), Phân bố khối lượng theo phạm vi cố định (FRVP), Đường trung bình động hàm mũ (EMA), Chỉ số sức mạnh tương đối (RSI), Chỉ số định hướng trung bình (ADX) và Phân kỳ hội tụ trung bình động (MACD), nhằm xác định các cơ hội giao dịch xác suất cao thông qua tổng hợp các chỉ báo.

Nguyên lý chiến lược

Chiến lược xác định tín hiệu vào lệnh dựa trên nhiều điều kiện:

- Giao cắt giữa giá và AVWAP

- Vị trí của giá so với EMA

- Đánh giá sức mạnh của RSI

- Động lượng xu hướng của MACD

- Xác nhận sức mạnh xu hướng của ADX

- Bộ lọc khối lượng

Chiến lược tập trung vào các phiên giao dịch châu Á, London và New York, nơi thường có tính thanh khoản tốt và tín hiệu giao dịch đáng tin cậy hơn. Logic vào lệnh bao gồm hai chế độ mua và bán, đồng thời thiết lập cơ chế chốt lời và cắt lỗ theo cấp độ.

Ưu điểm chiến lược

- Kết hợp nhiều chỉ báo, nâng cao độ chính xác của tín hiệu

- Bộ lọc khối lượng động, tránh giao dịch khi thanh khoản thấp

- Chiến lược chốt lời/cắt lỗ linh hoạt

- Tối ưu hóa dựa trên các khung giờ giao dịch khác nhau

- Cơ chế quản lý rủi ro động

- Hỗ trợ ra quyết định bằng tín hiệu trực quan

Rủi ro chiến lược

- Kết hợp nhiều chỉ báo có thể làm tăng độ phức tạp của tín hiệu

- Dữ liệu backtest có thể tiềm ẩn rủi ro quá khớp (overfitting)

- Hiệu suất có thể không ổn định trong các điều kiện thị trường khác nhau

- Chi phí giao dịch và trượt giá có thể ảnh hưởng đến lợi nhuận thực tế

Hướng tối ưu hóa chiến lược

- Đưa thuật toán học máy vào để điều chỉnh tham số động

- Tăng cường khả năng thích ứng với nhiều khung giờ giao dịch hơn

- Tối ưu hóa chiến lược chốt lời/cắt lỗ

- Bổ sung thêm các bộ lọc điều kiện

- Phát triển mô hình chiến lược đa năng cho nhiều loại tài sản

Tổng kết

Đây là một chiến lược giao dịch được tùy chỉnh cao và đa chiều, cố gắng nâng cao chất lượng và độ chính xác của tín hiệu giao dịch bằng cách tích hợp nhiều chỉ báo kỹ thuật và đặc điểm khung giờ giao dịch. Chiến lược này thể hiện sự phức tạp của việc tổng hợp chỉ báo và quản lý rủi ro động trong giao dịch định lượng.

/*backtest

start: 2024-04-02 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=6

strategy("FRVP + AVWAP by Grok", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// User Inputs- 1